During the week of March 15th to 20th, the high-yield sectors in the stock market crashed to unbelievably low stock price levels. The financial media gave their usual reasons for the share price drops including their “go-to” being that investors were afraid and selling their shares across the high-yield universe.

They were wrong: the financial media completely missed the underlying cause of the high-yield sell-off.

Over that single week, market values for real estate investment trusts (REITs), finance and mortgage REITs, master limited partnerships (MLPs), business development companies (BDCs), and preferred stock shares all crashed.

For example, from the market close on Friday, March 13th, to the bottom of the high-yield crash on March 18th, the Virtus InfraCap US Preferred Stock ETF (PFFA) dropped by 55%. PFFA is a diversified preferred stock ETF, an investment category viewed as safe. Over the same period, best in class BDC Main Street Capital (MAIN) experienced a 52% drop. Blue-chip pipeline MLP Plains All American Pipelines (PAA) lost 59% over the three trading days.

Here’s How Dividend Investors Are Setting Up Plans to Boost Their Income In A Short Time

Interestingly, after the bottom on Wednesday, March 18th, these high-yield investments came up strongly to close out the week. For example, at the close on the following Friday, PAA was up 52% compared to the Wednesday low.

The real cause of the high-yield sector’s meltdown was a massive forced unwinding of leveraged high-yield. The primary culprit was UBS Group AG (UBS), which announced mandatory redemptions for a dozen of its ETRACs 2xLeveraged ETNs.

These funds provided leveraged investments in mortgage REITs, MLPs, BDCs, preferred shares, and other high-yield stocks. The result was the dumping of millions of shares in these investment categories into the stock markets.

At the same time, leveraged closed-end funds (CEFs) in those categories saw their leverage levels skyrocket, pushing these funds also to dump shares into the stock market. I labeled this as a liquidity-driven crash that did not correlate with the fundamentals of the individual companies operating in the high-yield market sectors.

My contacts in the financial world clued me into what was really happening with the leveraged funds and high-yield share prices. There was one other clue that told me the crash in high-yield prices was not a sign of doom for those business sectors. Insiders jumped in and bought large numbers of shares.

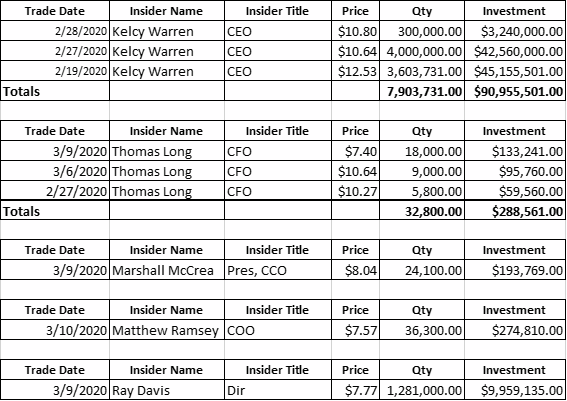

Through the sector crash for MLPs, Alerian reported that insiders in 19 energy midstream companies invested $109 million in the businesses with which they were intimately familiar. Here is the insider buying data for Energy Transfer (ET), one of the largest MLPs.

New Residential Investment Corp. (NRZ) a high-yield mortgage finance REIT reported these insider purchases on March 18:

- CFO Nicola Santoro purchased 50,000 shares at $5.84 each, bringing his stake in the company to 50,000 shares.

- Board member Alan Tyson purchased 10,000 shares at $5.01, bringing his stake to 125,700 shares.

- Board member Robert McGinnis purchased 10,000 shares at $5.18, bringing his stake to 77,500 shares.

- Board member Andrew Sloves purchased 10,000 shares at $5.83, bringing his stake to about 78,000 shares.

And again for NRZ on March 20:

- Board member Pamela Lenehan yesterday purchased 10K shares at $5.53 each.

- Board member Andrew Sloves made his second buy in two days, purchasing 10,000 shares at $6.03. He also picked up 1,000 shares of Series A Preferred shares for $11.00 each.

The large number of insider purchases were a firm indicator that the crash in stock prices was viewed as a great buying opportunity by those who best knew about the business prospects of these companies. I chose to follow the investment choices of these insiders rather than what happens when exchange-traded investment funds blow up due to over-aggressive strategies.