It’s been a turbulent year for the markets, to say the least.

Interest rates have been surging, labor strikes have taken a bite out of the automobile and entertainment industries, a few big banks have failed, and wars are raging on two continents.

The future looks no less uncertain. Inflation has eased a bit, but it’s still too high for the Fed to fully ease up on interest rates. The wars in Europe and the Middle East continue, making food and energy prices more volatile than they have been in years.

And closer to home, next year proves to be one of the most divisive election years in memory.

In short, 2024 promises to be another uncertain year in the markets.

That’s why we’ve had our team of analysts and researchers identify the most promising stocks to keep an eye on in 2024.

Let’s take a look…

Stock #1 for 2024 – GeoPark Ltd. (GPRK)

Analyst: Jay Soloff, StockNews, POWR Income

I’ve spoken before about the price support that is in place for oil globally, and the recent outbreak of violence in the Middle East will only serve to bolster recent price increases.

Due to its small size and location in Colombia, GeoPark Ltd. (GPRK), an upstream oil and gas company, simply flies under the radar of most investors. But after taking a close look under the hood, I believe there’s a compelling story here. Actually, GeoPark is an income stock in value clothing.

Take a peek at what I found…

Business Overview

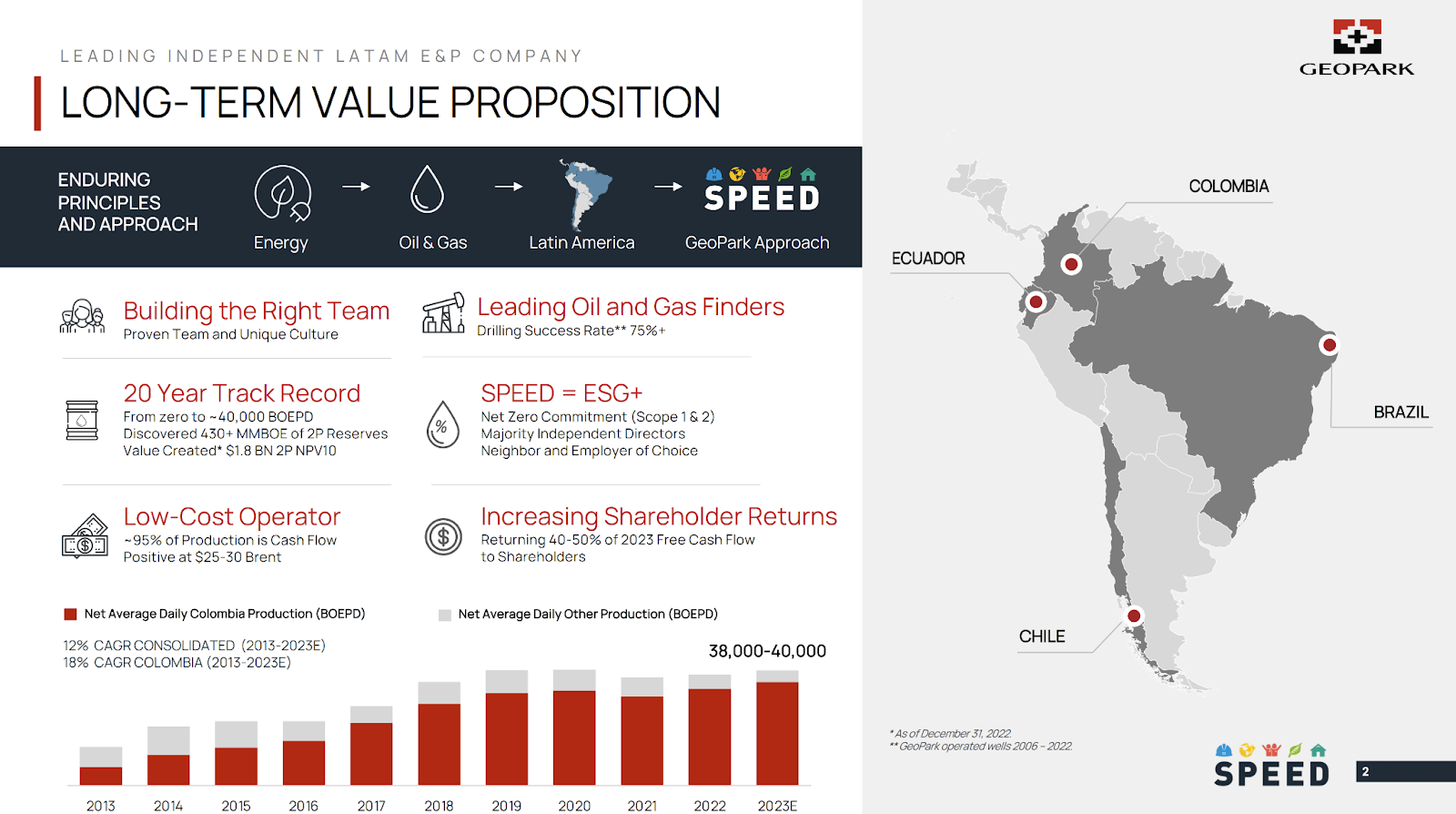

GeoPark is a leading independent exploration, developer and producer of oil and gas reserves in Chile, Colombia, Brazil, Argentina and Ecuador. Fact is, Latin America remains one of the world’s richest and most underexplored hydrocarbon regions.

GeoPark’s value begins in its drilling operations where GPRK has a 75% drilling success rate over the past 16 years.

Its prize asset is the Llanos 34 block—in its own words, “the largest oil discovery in over 20 years in Colombia.” Gross production has rocketed from zero to 75,000 barrels of oil per day in less than a decade.The drilling site was purchased for $30 million in 2012, has produced almost $2 billion since drilling began, and is estimated to contain another $2 billion of production today.

GeoPark also has a strategic partnership with ONGC Videsh – the government oil company of India – to jointly acquire, invest in, and create value from upstream oil and gas projects across Latin America. The company has net proven reserves of 87.8 million barrels of oil equivalent.

Here’s a look at all of GPRK’s operations:

Source: GPRK September 2023 Investor Presentation, p. 2

Financial Results

After weathering a downturn in earnings per share during the pandemic, GPRK bounced back and turned in explosive numbers in 2022.

Earnings Per Share:

● 2019 – $0.97

● 2020 – ($3.84)

● 2021 – $1.00

● 2022 – $3.78

GeoPark closed a record year in 2022, with revenues over $1 billion, adjusted EBITDA over $540 million, and bottom-line net profit of over $224 million.

Full year cash flow from operations was $467 million, which not only funded its capital expenditure program, but also paid down $170 million in debt, canceling entirely any debt owed in 2024.

In 2022, GeoPark paid shareholders more than $60 million, representing a yield of 6.15% or $0.52 per share. The company also has repurchased more than $133 million in its share buyback program since 2017.

Investment Considerations

Let’s talk a moment about the “value” side of GeoPark. The company trades at a lowly P/E of only 3.2, and at a super low 3x earnings. Its price to sales ratio is .88, and yet its operating margins are just under 50%. The company has $129 million of cash and cash equivalents on hand, and a credit facility of $80 million which has yet to be touched.

Its shares are a good value compared to the industry average P/E of 6.3. The company is extremely efficient, with operating margins clocking in at 44.4% and net profit margins of 22%.

Earnings have skyrocketed by 114% over the past year, and have grown by an average of 31.5% over the last five years. Meanwhile, dividends have blasted higher, from $0.02 cents per share in 2020 to $0.52 today—a 531% improvement in just three years, including a 58% jump since 2022.

And the good times should continue – the company plans on returning between 40% and 50% of free cash flow after taxes to shareholders (through dividends and buybacks).

Despite its low profile, the company is being squarely targeted by one group of savvy investors. Insiders currently own 16% of the shares and the top five shareholders own 55% of the company. Private equity firm Compass Group LLC, has almost 75 million shares and 14% of the float, while Cap Trust Financial Advisors holds another 13%.

What’s more, analysts project the share price to blast higher to $16.71 in the next twelve months, a massive 85% bump from current prices.

Not surprisingly GPRK has an outstanding 94.64% rating on the Value component of our POWR Ratings. GeoPark also scores highly in the areas of Quality and Sentiment where it ranks above 80% of the companies we track in both categories.

I like the conservative management of this South American driller, and think its income potential is in the sweet spot of the current oil market.

The shares are extremely undervalued, and for small investors, remain in stealth mode. But if you’re willing to dig down for a bargain in the energy field, I think they are worth a deeper dive and could leave you celebrating an even better New Year!

Stock #2 for 2024 – Immersion Corp. (IMMR)

Analyst: Jay Soloff, StockNews, Stocks Under $10

If you’re looking to ring in the New Year with a “buzz,” look no further than haptic technology maker, Immersion Corp. (IMMR).

The stock trades under $8 but’s in a rapidly growing field and brings strong financials to the table. While it may be best known for its gaming impact, there are a multitude of growth areas the company is attacking with its innovative technology.

Here’s how IMMR is shaking things up…

Business Overview

If you’re a gaming fan, you know the new Call of Duty (COD) just dropped its full release on November 10th. And even if you’re not a COD fan, if you’ve played any video games recently, you probably know there is nothing more important to a gamer than their controller.

Immersion Corp. is in the business of, among other things, making controllers more fun, keeping gamers engaged, and bringing new gamers to the table.

The company makes haptics…that’s the technology that makes the controller buzz in your hand when you hit a target, or your real life steering wheel vibrate when you cross the double yellow line, or even your phone vibrate when you get that important text telling you your takeout is ready.

As we become more and more tied to our video devices, Immersion is finding more and more ways to make the devices interactive, and in the case of automobile haptics, safer.

And with the emerging world of VR/AR (virtual reality/augmented reality) really coming into its own, Immersion has a whole new area of technology to deploy their interactive haptic devices. When most people think of VR/AR they think of video games, but there is a whole other side to the technology.

Training, from military to industrial to educational, is an especially vibrant part of VR/AR and spans a multitude of uses for haptic technology. And IMMR is perfectly positioned to cash in.

They have licensing agreements with industry giants like Samsung, Sony, Microsoft, and Nintendo to name a few. In 2022 and 2021, mobile communications represented 60% of total revenue, gaming and VR accounted for 21%, and automotive contributed 13% and 19%, respectively. These figures demonstrate the company’s successful penetration into key markets.

As a result, Immersion generates revenue across Asia, North America, and Europe. For the three months ended June 30, 2023, 83% of its total revenue came from Asia, while North America and Europe contributed 14% and 3%, respectively. A global presence ensures the company is well-positioned to capitalize on opportunities in diverse markets and regions.

As of December 31, 2022, Immersion and its wholly-owned subsidiaries held over 1,200 currently issued or pending patents worldwide, an extremely deep portfolio of intellectual property (IP).

And Immersion is laser-focused on protecting its IP portfolio. You see, protecting its IP is vital to safeguarding its technology and supporting its licensing model.

That’s why IMMR is currently pursuing patent infringement lawsuits against Meta, Valve, and Xiaomi. That commitment to safeguarding its IP locks in its competitive advantage and also a strategic incentive for potential customers.

Financial Results

● 2019 – $0.64

● 2020 – $0.19

● 2021 – $0.40

● 2022 – $0.92

Clearly, IMMR is headed in the right direction. As you can see, IMMR turned profitable in 2020 and has continued to grow earnings over the last three years. For the latest quarter it reported earnings of $7.0 million, or $0.21 per diluted share, handily beating the consensus estimates of $0.16 per share. The firm posted a net loss of more than $1.8 million a year ago.

The company also declared a dividend for the fourth consecutive quarter. The shares now yield 1.8%.

IMMR is also actively making share repurchases too, retiring 1.3% of all outstanding shares in the second quarter.The stock repurchase program was originally approved on December 29, 2022 and authorized the repurchase of up to $50 million of the company’s common stock.

“During the quarter our stockholders’ equity increased by $4.3 million sequentially and $12.3 million year-to-date while providing $3.9 million and $5.1 million, respectively, in stock repurchases and dividends.”said Eric Singer, Chairman and CEO.

The company’s revenues are almost entirely attributable to licensing. About $6.9 million of its $7 million in revenues came from its licensing stream.

Meanwhile, IMMR’s product mix delivers revenues from a slew of different industries.

In 2022 and 2021, mobile communications represented 60% of total revenue, gaming and VR accounted for 21%, and automotive contributed 19%. These figures demonstrate the company’s successful penetration into key markets.

Investment Considerations

Simply put, IMMR shares are dirt cheap at current valuations.

IMMR has a P/E of just over 5, and pretty incredible gross margins, at almost 98%. What’s more, operating margins are running at almost 64%.

Our POWR Ratings have Immersion at an overall grade of B, with a rating 87.43% better than all the stocks we track. It’s especially strong in Quality, at 96.78%.

Immersion is currently trading at the low end of a range it has been in over the past year, at just under $7, trading as high as $9.25 in late March.

The CEO Eric Singer made the biggest insider purchase in the last 12 months. A single transaction was for $146,000 worth of shares at a price of $7.29 each. Think about it – an insider was happy to buy shares at above the current price of $6.71.

Whether you’re picking up your copy of COD in the next month or not, Immersion should be on your radar as an under $10 stock that is bringing valuable technology to a number of hot technology areas.

Plus, the shares are trading at a price that should deliver a “buzz” to your portfolio and start the New Year off right.

Stocks #3-#6 for 2024 – JELD-WEN Holdings (JELD), PHX Minerals (PHX), MtronPTI (MPTI), and Profile Systems (PFIE)

Analyst: Tim Melvin, Investors Alley, The 20% Letter

It is that time of the year again.

I know what you are thinking.

Thanksgiving is fast upon us. It is time to start thinking about shopping for the big day. We will need turkey and all the fixings, along with some pies. We better stock up on wine and bourbon as well, with all the family headed our way.

We might even want to get some for them to drink.

That’s not it?

Then it must be Christmas.

We need a new tree.

What should we get the granddaughters?

Are we putting up outside lights this year?

That’s not it either.

Oh no-Don’t tell me. Not that.

I hate doing that. It is stupid and pointless.

That’s right, kids.

It is time to determine what stocks we should buy for 2024.

“What will the stock and bond markets do in the New Year?” everyone’s asking. “What will the market do in 2024?”

This is the most pointless exercise in the history of finance.

Nevertheless, publishers, Research Directors, and the marketing heads love it.

If you make a prediction and it’s wrong, that’s no big deal. Pretty much everyone will be wrong.

After all, who had American Coastal Insurance (ACIC) and its 1,757% 2023 gain on their 2023 bingo card?

How many folks suggested shorting market darling Enphase Energy (ENPH) before its 70% collapse this year?

How many suggested we would see another war breaking out in the Middle East involving Israel?

How many of us had Jimmy Buffett passing away in our 2023 checklist? Or that Keith Richards did not pass away?

The point is that people have yet to determine what will happen in the markets or the world in 2023, yet alone 2024.

Some stuff is predictable. With that in mind, here are my core predictions for 2024:

We will have a contentious election in 2024 for all levels of political office.

- Vote chasers will make many stupid statements. Shockingly, people will vote for them anyway.

- Something, somewhere in the world, will happen that no one expected.

- Most days, the stock market will be open from 9:30 a.m. to 4 p.m.

- During those hours, prices will fluctuate. Sometimes prices will fluctuate wildly.

- In 2023, some stocks no one has ever heard of will skyrocket in value.

- Some stocks everyone loves will collapse in value.

- Most people who make predictions will miss the mark.

- Publishers and marketing directors will promote those who get it right, or come close, as geniuses who can make you wealthier beyond your wildest dream by lunchtime a week from Tuesday.

They will not accomplish that.

Nor will they help you when their advice turns sour.

In short, predicting the market is a waste of time. You are far better off reacting to what the market does during the year.

When stocks sell off and everyone hates stocks, you should look for good companies at great prices. It will make you a lot of money over a year or two.

If you find companies with outstanding momentum attracting institutional buying, you should buy them. As long as the fundamentals improve, the stock price should keep climbing higher.

If stocks soar in value and sell for ridiculous multiples of asset values and cash flows, you should sell them.

If you can buy bonds in companies with a high probability of surviving until the principal is due, that yield more than historical stock market returns, you should do that.

I know that is not what you want to hear.

It is not what publishers or market directors want to see either.

It’s the right way to approach investing in 2024, but everyone wants magic stock picks.

I will not give you any of the picks I gave my members. It hardly seems fair to give you something they are paying for, does it?

Since the two anomalies that never go away, which I mentioned above, are value and momentum, I will give you two cheap stocks that could recover and give you huge returns. Both have passed my credit filters and should not experience any severe financial distress in 2023.

Along with that, I will give you stocks with fundamentals and price momentum that have the potential to keep climbing higher.

Our first value pick is JELD-WEN Holdings (JELD). This company makes windows and doors for homebuilders, home improvement, and replacement markets. It will be a bumpy road, but we need new homes, especially at the lower end of the market, to meet demand, which could drive substantial profit gains for JELD-WEN.

The upside could be enormous with the stock trading at an enterprise to earnings before interest and taxes multiple of just 5.

My next pick combines being undervalued and something of a long shot. PHX Minerals (PHX) is a natural gas and oil mineral company with acreage in Oklahoma, Texas, Louisiana, North Dakota, and Arkansas. It is a royalty company that has been working to increase its acreage and grow cash flows. The stock is currently trading at just 94% of tangible book value.

The company just turned down a takeover offer from a larger royalty company as inadequate. A higher offer in 2024 would not be a surprise.

Our first momentum stock is an Orlando-based company, MtronPTI (MPTI). The company makes radio frequency components that it sells to all the major defense companies. Its products are used in space flight, defense, aircraft, and instrumentation for air and spacecraft.

Its products are also used in hypersonic missiles, missile defense, drones, and electronic warfare.

Business is good.

Thanks to geopolitics and the overwhelming stupidity of nations, it will keep getting better.

Sales and earnings are growing. Margins are expanding. Analysts are raising estimates for sales and profits this year and next.

Fundamental momentum is driving strong price momentum.

Profile Systems (PFIE) makes burner management and combustion systems for the oil and gas industry. Its products make using burners that are part of the oil and gas production process safer by acting as a kind of thermostat to prevent accidents.

It’s a low-priced stock with strong sales and earnings momentum that is attracting buying pressure from institutional and retail buyers alike. Profits have exceeded analyst expectations, and Wall Street has been raising its estimates for Profire’s earnings in 2023 and 2024.

Profire’s fundamentals have everything you want to see in an outstanding growth stock. If that continues, this could be one of the biggest winners of 2024.

There you have it.

Flawless predictions for market behavior in 2024 that have been correct every year for all my years in the business.

Two growth stocks and two value stocks that have the characteristics of winning stocks.

Anything more is just guesswork and marketing.

Now, if you will excuse me, I have to go work on the shopping list for Thanksgiving and figure out what to buy the granddaughters for Christmas.

Stock #7 2024 – Main Street Capital (MAIN)

Analyst: Tim Plaehn, Investors Alley, The Dividend Hunter

I regularly review a large number of high yield stocks. I try to dig out the details that separate a high-quality company from one that has the potential to truly whack investor wealth. I often talk about how tremendous value can be found in the dark corners of the stock market, where the investing public doesn’t understand how these undiscovered nuggets of dividend paying companies operate. But sometimes I realize I need to go back and discuss a stock that should be a core holding for almost every stock market investor.

And this one may just be the best income stock that exists.

That’s why Main Street Capital (MAIN) is my conservative pick for 2024. The increase in interest rates dictated by the Fed over the last year has been very good for the profitability of business development companies (BDCs). Main Street Capital is the class of the BDC sector. The company has an unmatched record of dividend growth. MAIN pays monthly dividends. Plus the company historically has paid quarterly supplemental dividends.

MAIN is a stock that will produce consistent low to mid-teens compound annual total returns.

Legally, a BDC is a closed-end investment company, like closed-end mutual funds (CEF). The difference is that a CEF owns stock shares and bonds, while a BDC makes direct investments into its client companies.

A BDC will have up to hundreds of outstanding investments to spread the risk across many small companies. The client companies of a BDC will be corporations that are too small or too new to be able to issue stock or bonds into the publicly traded markets.

As a risk control factor, BDCs are limited to debt of no more than two times its equity.

This means that if a BDC has $500 million of equity raised from selling shares, it can borrow $1 billion. The company can then make $1.5 billion of loans or equity investments.

Main Street Capital Corp. is really quite different from the rest of the BDC crowd. Since its 2007 IPO, MAIN has tripled the total return average of its BDC peers.

Houston-based Main Street Capital has helped over 200 private companies grow or transition by providing flexible private equity and debt capital solutions.

The company provides “one-stop” capital solutions (private debt and private equity capital) to lower middle market companies and debt capital to middle market companies.

Main Street’s lower middle market (LMM) companies generally have annual revenues between $10 million and $150 million. While Main Street’s middle market debt investments are made in businesses that are generally larger in size.

The company’s current investment portfolio consists of 51% LMM, 36% Private Loan and 7% Middle Market companies and 6% other investments.

On December 31, 2021, Main Street Capital had 30 middle market clients with an average loan amount of $13 million. The loans total over $306 million or about 7% of MAIN’s total portfolio.

Middle market loans are floating rate and match with MAIN’s floating rate debt facility. The average 11.8% yield on this group of loans is 4.75% higher than Main Street’s debt used to fund the loans to clients. The 4.5% interest margin is almost pure cash flow that can be used to help pay dividends on MAIN’s stock shares.

The largest portion of the portfolio is lower middle market (LMM), where the company takes equity stakes along with providing debt financing. Equity provides a significant boost to the total returns generated. Lower middle market companies are smaller than the typical BDC client and have annual revenues between $10 and $150 million.

There are over 175,000 companies in this revenue bracket in the U.S., and MAIN has 79 lower middle market clients with loans and equity investments worth $2.1 billion. The loans to the companies in this part of the portfolio have an average yield of 12.6%.

The equity position gives an average 41% ownership of the client companies. The equity stakes are what have allowed MAIN’s net asset value (NAV) to increase from $12.85 in 2007 to $27.23 on March 31, 2023 – 112% growth.

The equity investments are what set MAIN apart from most other BDCs. The rules under which these companies operate prevent them from setting aside loan loss reserves. Because a BDC makes higher risk loans, there will be loan losses. These losses have a direct negative effect on a BDC’s book or net asset value. That is why most BDCs struggle to maintain their book values compared to the growing value built by Main Street Capital.

In recent years, Main Street has been growing what it calls its PrivateLoan Portfolio. These are loans originated through strategic relationships with other investment funds on a collaborative basis and are often referred to in the debt markets as “club deals”.

The private loan portfolio makes up 36% (86 loans for $1.5 billion) of the overall MAIN portfolio and carries an average yield of 12.4%. The loans have floating interest rates and benefit from lower overhead costs.

This three-tier investment portfolio is what sets MAIN apart from the rest of the BDC crowd, and what makes it an income stock for all seasons.

The lower middle market client, middle market client, and private loans mix provides a combination of net interest income to support MAIN’s very excellent history of dividend payments. Plus, MAIN holds an industry leading position in cost efficiency, with an Operating Expense to Assets Ratio of 1.4%.

The result has been a BDC that has generated both regular dividend growth for investors and special dividends to pay out capital gains. As an additional bonus, MAIN pays monthly dividends, smoothing out the cash flow into your brokerage account. MAIN should be a core holding for any income focused investor.

These facts add up to a very high-quality income investment with a 7% yield on the monthly dividends alone. The bonus dividends are just that, an added bonus on top of a great yield. The regular dividend increases will result in a low-teens yield on cost in just a few years. I know of no other stock that can be counted on to pay you 12-plus dividends per year and provide a growing cash income stream. If you do not own any MAIN shares, go buy some.

Stock #8 2024 – New Fortress Energy (NFE)

Analyst: Tim Plaehn, Investors Alley, The Dividend Hunter

Ongoing global events have me convinced that liquified natural gas (LNG) could be the world’s most important energy source for years—possibly decades—to come. The LNG infrastructure system allows the cost-effective transport of clean-burning natural gas from regions of plentiful supply to more populous countries with limited energy sources.

That’s why, for a more aggressive play for 2024, I’ve chosen New Fortress Energy (NFE). It’s a rapidly growing company focused on developing and operating downstream LNG infrastructure assets including LNG regassification and power generation. New Fortress also has employed the first of its Fast Gas upstream liquefaction plants that is installed on an offshore oil and gas rig.

Business Overview

New Fortress Energy operates primarily as a downstream seller of natural gas, delivered to its global network of LNG gasification terminals.

At the end of 2021, New Fortress Energy had 11 regasification terminals, up from five a year earlier. Now the company shows 14 facilities either operating or under development. Gas transport ships totaled 20, up from five. These assets provide LNG midstream and downstream services. New Fortress Energy will soon complete the cycle with its first LNG upstream investment. New Fortress Energy operates on long-term contracts to deliver LNG-based natural gas to customers served by the transport and terminals network. The contracts make New Fortress the exclusive gas supplier to its contracted customers.

Business History

New Fortress Energy launched with a January 30, 2019, IPO. As of the IPO, the company owned three operating large-scale projects and had four more under development.

In January 2021, New Fortress Energy announced the acquisition of HYGO Energy Transition Ltd. and Golar LNG Partners LP. With the acquisitions, the company bought three terminals and power plants in Brazil and 11 LNG ships from Golar.

These additions allow New Fortress to turn the corner to profitability. Here is the swing to profitability since the IPO.

- 2019: EBITDA of negative $115 million

- 2020: EBITDA of $33 million

- 2021: EBITDA of $605 million, including $334 million for the fourth quarter

- 2022: EBITDA of $1,071 million, exceeding the full-year guidance of $1.0 billion

To continue to expand, New Fortress Energy is moving to upstream LNG production with what it calls Fast LNG (FLNG). The first project will be to provide offshore liquefaction at Italian integrated energy company Eni’s offshore development in the Republic of Congo.

On March 31, 2022, the company filed to build its second Fast LNG offshore LNG export plant, off the coast of Louisiana. The company plans to have this plant up and running in 2023. In July, a third FLNG project was added to develop facilities off the coast of Mexico.

The Fast LNG projects will provide low-cost LNG to be resold to the company’s upstream customers.

The next project will be a green hydrogen production facility located in Texas. The plant will produce clean hydrogen close to end-users in the power generation, petrochemical, refining, and steel sectors.

Investment Considerations

During the 2021 fourth-quarter earnings call, New Fortress CEO Wesley Edens noted, “This really does mark the end of the beginning of us as a company.”

By that comment, he means the company has invested a lot of capital over the last few years to get to the point where the company is now very profitable, and additional capital investment will grow those profits.

Long-term LNG supply contracts provide a stable revenue base. The Fast LNG facilities will produce low-cost LNG to supply those contracts. Fast LNG can also ramp up production during price disruption to sell more gas into the markets when prices spike higher.

All in all, New Fortress Energy has strong visibility for the next two years of tremendous earnings growth. The company is also poised to continue to grow as LNG becomes the dominant form of global energy.

Currently, NFE pays a $0.10 quarterly dividend, for a 1% yield. The dividend has been paid since the 2020 fourth quarter.

In December 2022, the company announced a supplemental dividend plan to pay out 40% of adjusted EBITDA in semi-annual installments. A $3.00 per share dividend was declared at that time and paid in January.

New Fortress generated EBITDA of $600 million in 2022, will exceed $1 billion in 2023, and is forecasting $1.6 billion and $2.4 billion for 2024 and 2025, respectively.

This material is provided for informational purposes only and should not be construed as individualized investment advice or an offer or solicitation to buy or sell securities tailored to your needs. Investors should carefully consider the investment objectives and risks as well as charges and expenses of all securities before investing. Read the prospectus carefully before investing.

Nothing contained herein is to be considered a solicitation, research material, an investment recommendation or advice of any kind. The information contained herein may contain information that is subject to change without notice. Any investments or strategies referenced herein do not take into account the investment objectives, financial situation or particular needs of any specific person. Product suitability must be independently determined for each individual investor. [FirmName] explicitly disclaims any responsibility for product suitability or suitability determinations related to individual investors. This information does not constitute an offer to sell or a solicitation of an offer to buy securities, nor shall there be any sale of securities, in any state or jurisdiction in which such an offer, solicitation or sale would be unlawful.

Smaller capitalization securities involve greater issuer risk than larger capitalization securities, and the markets for such securities may be more volatile and less liquid. Specifically, small capitalization companies may be subject to more volatile market movements than securities of larger, more established companies, both because the securities typically are traded in lower volume and because the issuers typically are more subject to changes in earnings and prospects.

Securities of small and medium-sized companies tend to be riskier than those of larger companies. Compared to large companies, small and medium-sized companies may face greater business risks because they lack the management depth or experience, financial resources, product diversification or competitive strengths of larger companies, and they may be more adversely affected by poor economic conditions. There may be less publicly available information about smaller companies than larger companies. In addition, these companies may have been recently organized and may have little or no track record of success.

Investing internationally carries additional risks such as differences in financial reporting, currency exchange risk, as well as economic and political risk unique to the specific country. This may result in greater share price volatility. Shares, when sold, may be worth more or less than their original cost.

Investments in commodities may have greater volatility than investments in traditional securities, particularly if the instruments involve leverage. The value of commodity-linked derivative instruments may be affected by changes in overall market movements, commodity index volatility, changes in interest rates or factors affecting a particular industry or commodity, such as drought, floods, weather, livestock disease, embargoes, tariffs and international economic, political and regulatory developments. Use of leveraged commodity-linked derivatives creates an opportunity for increased return but, at the same time, creates the possibility for greater loss.

Mutual Funds and Exchange Traded Funds (ETFs) are sold by prospectus. Please consider the investment objectives, risks, charges, and expenses carefully before investing. The prospectus, which contains this and other information about the investment company, can be obtained from the Fund Company or your financial professional. Be sure to read the prospectus carefully before deciding whether to invest.

Advisory services are offered through Magnifi LLC, an SEC Registered Investment Advisor. Being registered as an investment adviser does not imply a certain level of skill or training. The information contained herein should in no way be construed or interpreted as a solicitation to sell or offer to sell advisory services to any residents of any State where notice-filed or otherwise legally permitted. All content is for information purposes only. It is not intended to provide any tax or legal advice or provide the basis for any financial decisions. Nor is it intended to be a projection of current or future performance or indication of future results. Moreover, this material has been derived from sources believed to be reliable but is not guaranteed as to accuracy and completeness and does not purport to be a complete analysis of the materials discussed. Purchases are subject to suitability. This requires a review of an investor’s objective, risk tolerance, and time horizons. Investing always involves risk and possible loss of capital.