Below you’ll find the current monthly issue and back issues, conveniently all on one page. The beginning of each month’s issue is noted by the publication date.

May 31, 2024 - 3:30 pm

June 2024 Issue

The last month has been fairly eventful for the interest rate markets. We have seen a Federal Reserve meeting, Fed minutes, and countless Fed officials out speaking in public without handlers. If we distill it all down to its essence, the message is simple: we would love to start cutting rates, but it’s not justified by the data. Therefore, rates will remain higher for longer.

As I write this, the U.S. Treasury is struggling with bond auctions that are not going particularly well. The five- and seven-year auctions did not go well, with yields coming in at the top of the expected range. In addition, the Conference Board released its latest consumer confidence numbers, which showed one of the biggest bounces in some time. Despite facing challenges such as high interest rates, inflation, and economic uncertainty, American consumers have demonstrated remarkable resilience, contributing significantly to economic growth in the previous year.

Thanks in large part to waves of government spending related to various programs and policy agendas, the job markets have been fairly robust. Low layoff rates and a tight job market have contributed to income growth and consumer confidence. It has, of course, helped that the consumer market is in much better shape than most of the clickbait hunters and doom-and-gloom crowd want you to believe. Supported by a healthy labor market and rising wages, personal income continues to grow at a pace consistent with previous economic expansions.

Unlike what the headline writers may want you to believe, there is no consumer debt bomb. Since the great financial crisis, consumers have strengthened their balance sheets and resisted the urge to be stupid. Debt levels have gone up over the past year, but incomes and net worth have gone up even faster.

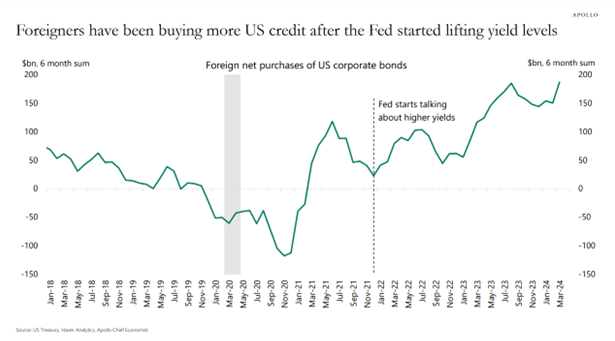

We have seen some signs of developing economic weakness, but it is not enough for the Fed to act. The central bank’s bigger issues are that inflation is sticky, and no one wants to buy our bonds. We have trillions of dollars left to refinance this year, and potential buyers are staying away in droves, due to concerns of political instability and a contentious election. China is out, and Japan has greatly reduced its buying of treasuries. Foreigners looking to buy U.S. credit instruments are increasingly looking to corporate bonds for higher yields and do not feel like they are giving up much in safety when comparing corporate issuers against a dysfunctional government.

Individual and investment fund demand is also lower than hoped so far this year. The almost constant headlines about the size and growth of the United States budget deficit and debt load are also keeping investors on the sidelines. It probably does not help that the inverted yield curve means notoriously short-sighted, instant gratification-addicted investors can get higher yields in money markets than they can in longer-term bonds.

When something is not selling, you have to lower the price. That is basic economics. In the case of treasuries, you have to lower the price until the yield attracts buyers. Rate hikes and tighter credit have not had the expected impact on inflation and the economy for one simple reason: the government, at almost every level, is spending like drunken sailors with wallets full of back pay, out on a bender. This is an election year, so there is little chance we see a slowdown in spending. Eventually, all of this leads to higher taxes to cure the deficit, but that is a subject for another day. Of course, it is also a great reason to buy the tax-free funds on our buy list.

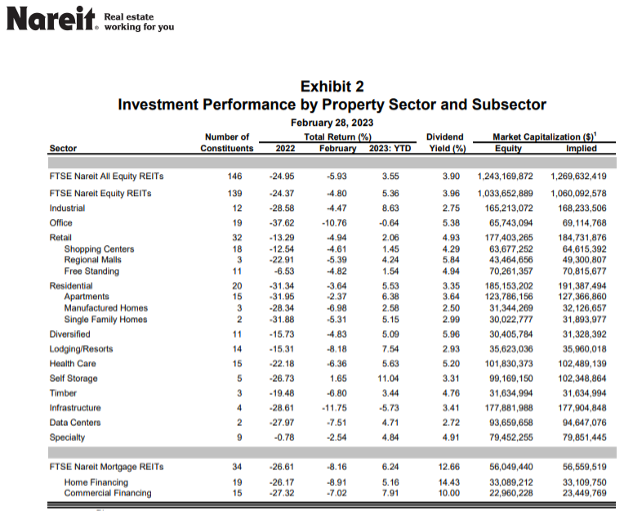

What does higher-for-longer mean for us as income-seeking investors? First, there is no better place to find the income we are seeking than deeply discounted closed-end funds, which allow us to invest in the attractive corners of the fixed-income markets at a discount from the current market prices. There are so many closed-end funds today that we can pick and choose which sectors we own. Right now, real estate-related debt is clearly one of the most attractive segments of the corporate bond market.

Over the course of my career, I have learned that following the moves of successful private equity funds when they make a big move into a sector is a recipe for success. Blackstone has been on a very aggressive buying spree of real estate-related debt in recent months. As a recent article on KKR’s website pointed out: “Across the market, we are finding that it is possible to lend at a significant discount to replacement cost and often at 50% of peak valuations while earning low-to-mid-teens gross returns on mezzanine-like exposure at loan-to-value ratios near 65%. In other words, it is possible to earn equity-like returns at a favorable position in the capital structure, and the scarcity of debt capital in the market means that these conditions should persist, in our view.”

Last month, the real estate team at Ares Management suggested that a real estate reset was getting underway, with improved property values and real estate-related debt markets beginning to thaw. The alternative credit leader has been raising billions of dollars in recent months to invest in real estate equity and debt opportunities. We have several funds that invest in real estate and CRE debt that are bargain opportunities.

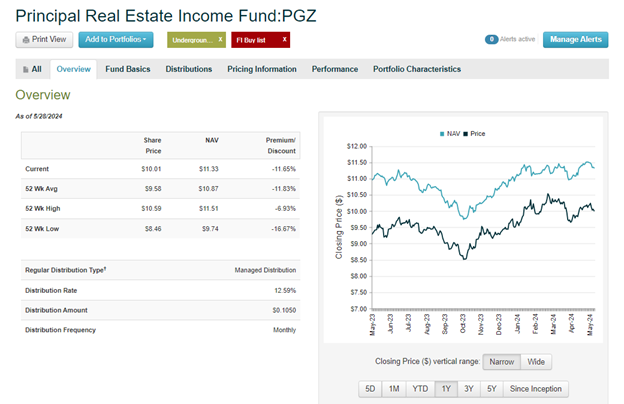

While the activist at the Principal Real Estate Income Fund failed to gain a board seat at the recent annual meeting, we still think the fund is very attractive at current levels. The activists still own a large position and are unlikely to go away anytime soon.

CEFCONNECT.COM

The shares currently trade at a discount of 11.6% with a yield of 12.5%. The fund is invested in real estate-related debt and mortgage-backed securities as well as a handful of REIT equities. You can buy shares of the fund below $ 10.50.

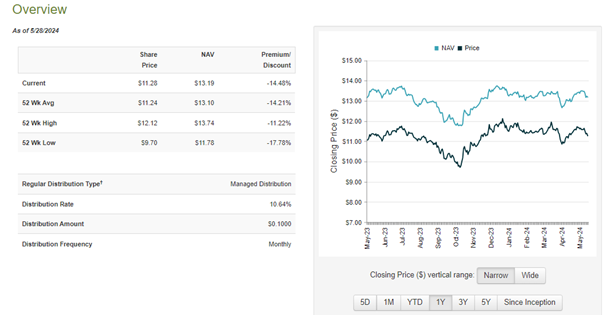

Shares of Nuveen Real Asset Income and Growth Fund (JRI) have recently fallen below the $ 11.55 buy limit.

This fund is trading at a 14.5% discount to NAV and yields 10.6%. The fund has equity positions in companies that own real assets like real estate and energy infrastructure, as well as high-yield debt issued by companies that own real assets. Several activists, including Saba Capital, hold large positions in the shares.

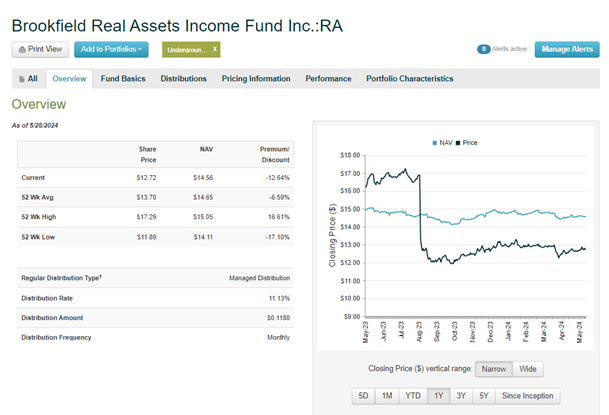

Shares of Brookfield Real Asset Fund are also trading below the buy limit price of $ 13.25.

The fund is trading at a 12.6% discount with an 11.1% yield right now. The fund is invested in real estate and energy-related debt as well as mortgage-backed securities. As is always the case, there are several activist shareholders with sizable positions in the fund.

Higher-for-longer means fixed-income assets are more attractive than ever. Our approach favors buying out-of-favor asset classes with a higher potential for a reversal. That is why we own heavily discounted closed-end funds that own real estate assets. All four conditions are met, and we should see a strong upside from the eventual recovery in the real estate markets.

Remember to tender your shares of ClearBridge MLP and Midstream Fund (CEM). Tender all your shares with the expectation that you will receive 50% redeemed at net asset value. The Fund commenced the offer on May 21, 2024, with an expiration time of 5:00 p.m., New York City time, on June 20, 2024.

February 7, 2024 - 9:45 am

This month, we are going to venture off into the wilds of the world and the markets.

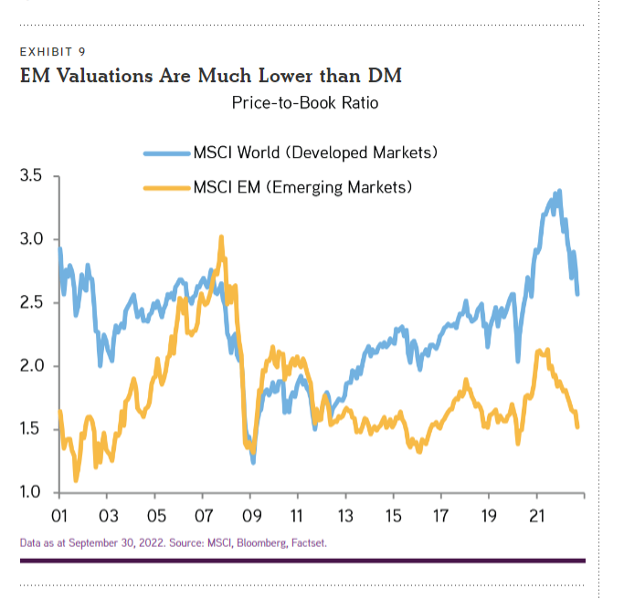

Our first stop is going to be emerging markets. I will reinforce the idea that you need to be sure you own shares of the Morgan Stanley Emerging Market Domestic Debt Fund (EDD). The tailwinds of falling inflation, falling global interest rates, and a weak dollar should combine to deliver fantastic truths. The fund is already up 15% this year, but we are just getting started.

The current conditions for emerging market debt look like they have in previous periods where emerging market local debt has rallied. The currencies are cheap relative to developed markets, and the yields of government and high-quality corporate bonds are higher.

In the past, these conditions have resulted in long-term markets that gave adventurous investors huge returns. The fund returns income only, and the yield is currently 7.84%. The discount to net asset value is 15% right now.

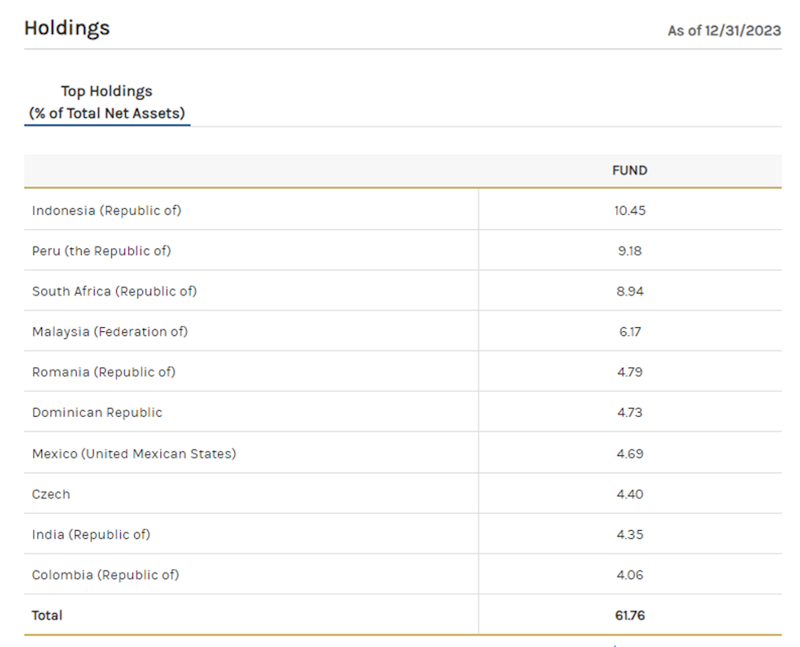

The top ten countries that the Morgan Stanley Emerging Markets Funds is invested in include some places that you might not want to vacation. Still, the economies are growing, interest rates are well above U.S. and European levels, and the fixed-income returns should see strong tailwinds from the three favorable factors.

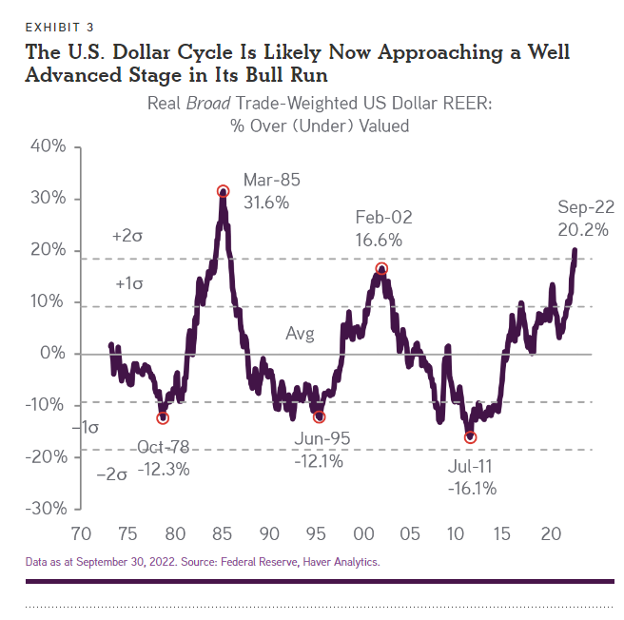

Emerging market fixed-income performance has been flat for a long time. The U.S. dollar has been strong for more than a decade, which has limited gains.

While the emerging market stories of China and India are well known, that’s not the case for the fund’s top holding, Indonesia. Indonesia is now considered an upper-income country and is a member of the G20. It is currently the seventh-largest economy in the world, ranked by gross domestic product.

Indonesia is expected to keep experiencing solid economic and population growth for several decades. The country is resource-rich, with a large agricultural base producing commodities including rice, palm oil, peanuts, rubber, and other items for domestic consumption and export markets. Seafood is also a massive industry for Indonesia: the country is the world’s largest producer of tuna.

Indonesia is also expanding its mining operations in critical metals, including copper, nickel, gold, and coal. Despite all the climate change discussions, coal is still a growing market, and reports to other emerging markets should continue to be strong. Indonesia will also be a significant player in the transition to green energy, as it is the largest producer of nickel and the second largest producer of cobalt.

While Indonesia may be an emerging market, its credit rating is right up there with many of the more developed nations. S&P assigns the nation a BBB rating with a “Stable” outlook. So does Fitch Rating Service.

I could go through all the top ten nations, but that would take too much time and be far too dull for most readers. Suffice it to say that these countries have vibrant economies and will be able to pay their bills, meaning there is nowhere near the level of credit risk that most investors will automatically associate with the phrase “emerging markets.”

If you do not already own this fund, add it to your fixed-income portfolio as soon as possible. You can pay up to .80 for your shares.

I did add a new fund to the portfolio last week—yet another infrastructure fund.

Private infrastructure is one of the best-performing asset classes available to investors; however, most people skip it because it is not exciting.

But, I’m telling you: it should be exciting.

While infrastructure is not going to offer you the promise of turbocharged get-rich-quick schemes, what it does offer is far more realistic and valuable. Private infrastructure, both energy and non-energy, offer steady returns that allow you to compound your wealth at a high rate for long periods of time. When things go south in the economy and markets and turbocharged promises turn into massive real losses, infrastructure prices hold up much better than the price of stocks and keep throwing off steady streams of cash.

While the Ecofin Sustainable and Social Impact Term Fund (TEAF) owns some traditional energy infrastructure, it also has a substantial interest in renewable infrastructure, including private investments in solar farms and wind assets, as well as water-related assets and other valuable, cash-producing infrastructure projects.

The fund has also been involved in financing not-for-profit senior living facilities. Considering that 10,000 Americans a day are turning 65, the need for these facilities will be enormous.

The lack of new projects has helped the nonprofit facilities maintain high occupancy rates. This model has fared much better than for-profit facilities in recent years.

Financing charter schools is another unique infrastructure investment strategy the fund uses to deliver inflation and economic-proof returns for investors. Charter schools currently serve 3.7 million students in 7,996 schools across the United States, and I expect that number to grow substantially.

While most projects are in the United States, TEAF has infrastructure assets worldwide. The Ecofin fund does own a lot of private investments, but most of them are things like schools and solar farms that are relatively easy to value.

The market’s fear of private investment has caused put the shares at a discount to the net asset value of 23%. At the same time, most of the projects owned by the fund are throwing off large amounts of cash, and the shares are yielding 9.5%. Dividends are paid monthly and are reported on IRS Form 1099. Once again, the magic of closed-end fund accounting turns partnership income into ordinary dividends, with no K1s or tax hassles.

Tortoise is the primary advisor of the fund, which has been a target of SABA Capital and other activists in the past year.

Tortoise was once thought to be too big to tackle for activists, but Boaz Weinstein has laid that idea to rest, and all closed-end fund managers and sponsors are now targets if the discounts to NAV of these funds are too wide.

This is apparent when you consider that Saba and Weinstein have scored yet another win against mutual fund behemoth Franklin Templeton (BEN). Franklin is the parent company of Clearbridge, the sponsor of a portfolio holding ClearBridge MLP and Midstream Fund (CEM).

The fund announced last week that it would be merged into ClearBridge Energy Midstream Opportunity Fund Inc. (EMO). The merger value will be based on the NAV of the respective funds at the time of the completion of the deal.

Even with the merger it’s interesting to see what impact adding EMO to your portfolio could have using Magnifi (it’s free for my readers.

Try it now, click here.

Prior to completion of the merger, it will conduct a tender offer for up to 50% of its shares at 100% of net asset value for 50% of the outstanding shares. Make sure you tender 100% to get the maximum 50% acceptance. If you tender 50%, you will only sell 25% of your shares back to the fund.

With the most recent Federal Reserve announcement, Wall Street was shocked that Jerome Powell and his team indicated they were not ready to lower rates yet. The Fed statement proclaimed that: “The Committee does not expect it will be appropriate to reduce the target range until it has gained greater confidence that inflation is moving sustainably toward 2 percent.”

Apparently, traders were surprised by that. But I am not sure how surprised you get to be when government officials tell you something they have been telling you they would say to you for weeks in advance.

While core inflation is down, the Fed wants to see more data, and feel confident that inflation will fall below the target rate of 2%, before signing off on cuts in the fed funds rate.

There is no longer any discussion of possible hikes. Barring some inflation spike caused by energy prices or some other geopolitical disaster, this rate-hiking cycle is over. The question has now shifted to when, not if, on the subject of rate cuts. The timing of the cuts will determine if this is wildly bullish or insanely bullish for our fixed-income funds.

I would like to get some near-term shock to the interest rate markets to add aggressively to our tax-free funds at better yields. We were just getting started with tax-free promotions when rates began their rally last year and have just recently begun to trend sideways or slightly lower. Hopefully, there will be some news flow that will cause the downward drift to continue.

Our two overweights are infrastructure and fixed income, so we are perfectly positioned for whatever happens next.

While we would love to get more money to work in small-cap funds and funds with significant real estate holding, I will not break the rules to do so.

We have scored multiple wins from activist activities in our funds so far. We continue to collect above-average income streams, and the latest addition to the portfolio increases the amount of cash hitting your account every month.

Be sure to join me for our next live monthly webinar later this month. You can get the link and watch the most recent replay here.

January 2, 2024 - 8:00 am

I am writing this on the 27th of December, and we have more than accomplished my major goals for Underground Income in 2023:

1. We have collected a dividend yield greater than the junk bond market, and with far less risk.

Our total return so far this year is more than 15%.

If we can compound in the mid-to-high teens while ignoring the broader stock market, we should be able to help total return-oriented investors compound their wealth at a pace that helps them reach all their goals and financial dreams.

That does not match the gain of the S&P 500, but that was never our goal – as I’ve grown to appreciate in the years when the markets tank.

2. We easily outperformed the bond and oil markets.

This wasn’t exactly a goal, but it is quite an achievement—especially given that we were massively overweight fixed income and energy assets all year—so it’s worth including here.

While I pay attention to what is happening in the markets and am well-versed in macroeconomic and geopolitical affairs, they are not the driving factor in selecting discounted closed-end funds for the Underground Income portfolio.

There are four factors that go into that decision-making process:

First, we must feel like the asset class is due for a reversal.

This is not based on headlines, opinions, or feelings—it is pure math. We want to buy significantly undervalued assets, and I do not care if they are stocks, bonds, real estate, or commodities.

I am also impartial to the distinction between foreign and domestic assets for the most part. The overriding question is whether the assets are undervalued to the point that a reversal in the near future seems imminent.

The math leads us to favor those sections that bombed out, and that everyone hates. More than three decades of being a deep value investor with a huge contrarian streak has taught me that the math is correct most of the time.

People’s opinions and feelings are much less important than math when it comes to markets and investing. Leave your feelings and opinions for the holiday dinner seating arrangements (although if I could use math for this, I would) and team sports franchise attachments.

Second, the fund must trade for less than the value of the stocks, bonds, real property, and cash it holds.

We are looking to buy discounted dollars. The first thing to consider is the level of the discount to net asset value (NAV). I want to buy funds that trade for much less than the value of the stocks and bonds owned by the fund, and the larger the discount to NAV, the more interested I am in adding the fund to the Underground Income portfolio.

Third, there must be an income stream.

This service is for Income and total return-oriented investors; most of our funds pay monthly dividends, but we have a handful of quarterly payers. Either way, a decent dividend yield is a must.

Finally, there must be an activist shareholder who has a long track record of leaning in management to take the steps necessary to narrow the discount to the net asset value.

I make it a point to know the track record of the activists involved in closed-end funds and prefer the small handful with strong track records of success.

This year, we have seen several activist victories leading to dividend increases, buybacks, trade offers, and mergers, including one pending merger into an exchange-traded fund.

Most recently, ClearBridge MLP and Midstream Fund (CEM) announced that they have reached an agreement with Saba Capital, a prominent activist shareholder, and would be considering a tender offer.

The fund will buy back up to 50% of its shares at 100% of net asset value. In Return, Saba will rescind its nominees for board seats and vote to merge several Clearbridge funds.

When you receive notice of the tender from your broker, tender 100% of your shares. You will get a maximum of 50%, but tender all, or you will get half of what you tender.

This will be another major winner for us, with further gains possible when the merger of the funds culminates after the tender offer concludes sometime in 2024.

Following the four rules above gives us three ways to make money with every fund added to the Underground Income portfolio:

- Asset appreciation: The value of the securities and assets in the fund stops going down and increases in value.

- The NAV discount narrows: This can happen on its own, as fund discounts and premiums tend to be mean-reverting over time. Limiting our preference to funds with proven activists accelerates the reversion process.

- Each fund in the portfolio pays a dividend: You can take it in cash or reinvest in more shares; either way, it is cash paid that cannot be taken back.

You will find that I am a stickler for the rules regarding this portfolio.

I did not pull them out of thin air. Some, I learned from successful, experienced investors who share their knowledge of closed-end discount arbitrage investing with me. Others, I learned through my own experience. I have confirmed all the rules the hard way, by contributing my cash to people who did not bend the rules, tempting as it is to break the rules.

I am not in the camp that thinks all commercial real estate will implode and crash the financial markets. In fact, I have my eye on closed-end funds that invest in commercial real estate. I have owned them before and would love to own them now. However, the discounts never got high enough, and there has been no significant activist activity in the funds.

The same holds true for small-cap value closed-end funds run by the managers I respect. Our conditions were never met, so we never bought a share. I suspect we will get our chance in 2024, but suspicions will not be the deciding factor—we will buy them if and when all four conditions are met. My feelings and opinions will not play a role.

Several of our funds have paid special dividends recently, and as we approach the New year, we have seen a rally of just about every asset class. Stocks, bonds, and REITs have all rallied sharply on the expectation not only that the Fed is done raising rates, but also that cuts are coming sooner rather than later. If that turns out to be the case, then stand by for a sharp reversal of the rallies in stocks and REITs. Rate cuts would mean that the economy is weakening rapidly.

There have been signs of some weakening in things like capital expenditure plans and manufacturing reports from Philadelphia, Richmond, New York, Kansas City, and Dallas. Small business optimism was in the toilet all of 2023. The Index of Leading Economic Indicators was also down all year. However, while the data has shown some weakness, none of it has shown signs of accelerating economic decline that would justify lowering interest rates in the first quarter of the year.

Optimism abounds if you look at the various predictions and estimates for 2024. And when it comes to economic and market forecasts, anytime anything abounds, a healthy dose of skepticism is in order.

Nothing in a mathematical observation of equity markets suggests the basis for a rally that further extends valuation is in the cards; however, that does not mean it cannot happen. It just means that probabilities suggest that returns for the next several years will be low and possibly even mildly negative for large-cap stocks.

If we look at geopolitics and economics, there is a lot more potential for negative surprises than positive ones. The wave of optimism is dismissing one of the most unsettled global geopolitical situations in a long time.

The math of closed-end funds is keeping us mostly out of non-energy-related stocks and real estate as we enter 2024. In my over three decades of tracking closed-end fund activity, discount levels and activist activity have done a decent job of forecasting what is about to happen in markets.

That track record as a prognosticator is as good as, or better than, most people collecting six and seven-figure paychecks to make predictions.

2023 was an excellent year for Underground Income, and following discounts and activist activity in unpopular and ignored asset classes should lead to another good year in 2024.

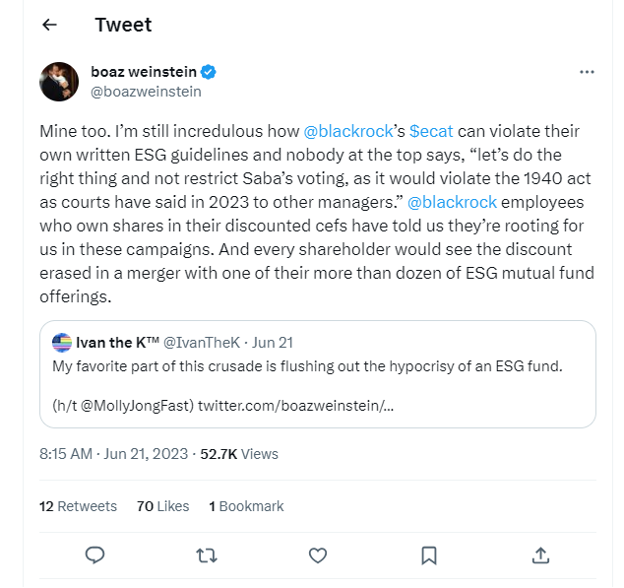

The recent court decision involving Saba, Nuveen, and Blackrock has set the stage for a supercharged level of activist activity in closed-end funds over the next several years. The victory for Saba, especially, makes it clear that no fund sponsor is too big to tackle anymore.

We are in the first inning of what will be a massive transformation for the closed-end funds, and enormous profits will be made.

Underground Income investors should expect to collect their fair shares and then some of these profits.

December 6, 2023 - 4:53 pm

Right before I began pulling together my notes for this month’s newsletter, I saw the news that Charlie Munger had died.

For those who do not know, Munger was the Vice-Chairman of Berkshire Hathaway, and Warren Buffett’s sidekick and intellectual companion for decades.

It is impossible not to acknowledge that Buffett is one of the most successful investors and sharpest business people of the last 70 years. We also must admit that he is a master of the PR game. Although the blood of a pirate of the bounding main flows through his veins, he hides it behind the persona of a capitalist Santa Claus.

But just ask anyone who was ever on the opposite side of the table from him how much of a Santa Claus Buffett is in reality. He ended up owning Berkshire Hathaway (BRK-A) because he had a deal to sell the stock back to the company as part of a negotiated tender offer. Then, the CEO, Seabury Stanton, tried to chisel Warren out of an eighth of a point. Buffett backed out of the deal and bought the whole company so he could fire Seaborn.

Santa Claus indeed!

Munger was also a brilliant investor and a thinker of an entirely different level than most people. A few hours of reading Poor Charlie’s Almanac, and some of the talks and discussions published in that volume will quickly make you aware that Munger understood things most people don’t even think about on any level.

I am not going to rewrite Munger’s obituary. There will be several dozen versions of that spinning around the web by now. There will also be countless “How I knew Charlie” and “How I almost met Charlie one time” stories circulating.

I have nothing to add to those. I never even came close to meeting Charlie Munger. I could have met him at a Berkshire meeting, but he and Buffett were always inconsiderate enough to hold it on my birthday weekend. (The great state of Kentucky throws a horse race for the occasion every year, but the Berkshire Bobbsey Twins never bothered to acknowledge the day!)

I would be remiss if we did not touch on some of the principles that made Munger not just a great investor but a great person.

First and foremost, Munger was a prolific reader. He also said at various points that he never met any wise people who were not prolific readers. His kids referred to him as a book with legs.

I can relate and agree: the biggest favor you can do for your kids is teach them not just to read but to love books. And without my own love of reading, my life would follow an entirely different and much less attractive script.

Munger loved biographies and history. He called reading biographies making friends with the eminent dead. And making friends with the right dead people, Munger pointed out, can make an enormous difference in your life.

He was also a huge fan of being different from everyone else. After all, doing the same thing everyone else does achieves the same results as everyone else. So, given that the average individual investor underperforms the market, why would you shoot for average?

Like me, Munger despised trading. He had a discussion as recently as April of this year with Todd Combs, the CEO of GEICO. He said this about trading:

We have a liquid stock market, which is two things at once—it’s a place for people who are doing long-term investment rationally to go and make their transactions, and it’s a place for another bunch of people to do casino gambling. We mix them up totally. It’s an absolutely insane thing for the country. It’s like we mixed up running the army with child prostitution. It’s ludicrously crazy, but everybody that’s making money out of it loves it this way.

He added that making the casino part of the modern form of capitalism was an insane policy.

By the way, the people making money from trading are NOT the retail traders. The ones making money are the market makers and options statistical arbitrage players. It is often the sophisticated volatility traders who you’re seeing prosper—not Joe Sixpack, trading five contracts because of some super special price pattern.

Working around markets and Wall Street, LaSalle Street, and Wacker Drive, I have met plenty of wealthy people. I have had many drinks with many people in the bars of Rush Street in Chicago who made millions in the options market. They were all floor traders, spread traders, or market makers.

For us mere mortals, the secret to investing success is not short-term, lightning-fast, multi-million-dollar gains—those are the stuff of luck, legend, and leverage. Fortunes, instead, are built by steady compounding of returns without any disastrous losses.

Munger and Buffett emphasized the same principles we use here at Underground Income: price, time, and margin of safety. If we buy the right fund at the right price and avoid taking stupid risks, time (with considerable assistance from closed-end fund activists) will help us compound our money over time.

If income is your primary goal, then Underground Income can allow you to collect high levels of income, most paid monthly, and the combination of asset improvement and narrowing discounts can help offset the ravages of inflation.

As I write this, the news is all favorable for inflation and, allegedly, the economy. The GDP number for the third quarter has been revised up to over 5%, and the inflation readings remain modest. I am writing this before the personal consumption expenditure index, the Fed’s favorite measure, comes out, but I do not expect any massive changes from expectations in that number.

Analysts are falling all over themselves to suggest we will have a magical soft landing.

I really do not expect that to happen.

If you go below the headlines of the Beige Book released by the Federal Reserve last week, consumer spending is slowing—big purchases of stuff like furniture and appliances is down. Employment is flatlining. Retail sales are declining, even as we start the holiday season. Black Friday hit record numbers, but sales were clustered amongst the most heavily discounted items. And the four-week average of continuing unemployment claims hit the highest numbers since December of 2021.

A “soft landing,” in which the economy chirps merrily along while the inflation rate falls below 2% still seems highly unlikely.

That does not put me in the end of America, imminent depression, and riots in the street crowd. Instead, I expect to see a garden-variety recession, with moderate unemployment, sometime next year.

The biggest threat to the suggestion of an economic slowdown is spending by the government. State and local governments are doing their share, but the real culprit is the Federal government. The spending programs in the laughably named Inflation Reduction Act and tax credits for the Green Energy Grift are doing their best to offset the higher interest rates and tighter bank credit conditions that have been slowing the economy.

That does not smooth the path to a soft landing. In fact, it is far more likely to ignite inflation.

As we go into the holiday season, the markets want to believe in a soft landing. As usual, most participants are only reading the headlines, which in most cases are written to appease those participants.

As we go into the holiday season, the markets want to believe in a soft landing. As usual, most participants are only reading the headlines, which in most cases are written to appease those participants.

Even the soft-landing scenarios include a softer, kinder Fed, lowering interest rates at some point next year. Some scenarios show the Fed delivering cuts at the same pace FedEx delivers packages two days before Christmas, with multiple cuts in 2024.

Whether the cuts come from the kindness of “Uncle Jerome’s” heart or in response to an economic slowdown, they will be outstanding for our fixed-income positions.

There are, however, threats to our outlook.

One is geopolitical. At this point, Ukraine, the Middle East, and China are all still in play. How the markets might react to that is hard to know.

The nice part is that it’s a safe bet that energy and fixed income will react differently and offset each other in the event of an event. Energy moving higher on its own due to market forces or shocks is another risk that could reignite inflation. Once again, if that happens, one part of our portfolio will zig while the other zags, with offsetting price movements.

Under either worst-case scenario, the cash keeps pouring into our account month after month.

The Kayne Anderson Energy Infrastructure (KYN) merger with the Kayne Anderson NextGen Energy & Infrastructure closed this month. As expected, we saw a bump in dividend income, and this is now one of the most attractive funds in the portfolio. The NAV is $ 10.32, and the market price is around $ 8.35—a 19% discount to NAV. For new buyers, the yield is over 10%. And as always, all that K1 partnership income is turned into 1099 dividend income, thanks to the magic of closed-end fund accounting.

This combined portfolio is a collection of the most attractive energy infrastructure assets in the United States. Click here to see how much KYN you own – and decide whether it’s time to add more.

The Holiday season is fast upon us, and however you celebrate this time of year, I wish all the best to you and yours.

Best wishes for a happy and very prosperous New Year.

Click here to see the current Underground Income Portfolio.

November 1, 2023 - 9:00 am

The stock market returns 10% a year—everybody knows that.

Owning stocks is much better than owning bonds. When you consider inflation and taxes, bonds are just certificates of confiscation—everybody knows that, too.

Timing the markets is always a mistake. It cannot be done.

You should stay in stocks and take your lumps no matter what happens. It is the only way us regular folks can make money.

Everybody knows all of that, too.

In the past decade or so, fueled by a race between the Federal Reserve and Congress to see who can pump the most money at the fastest pace into the economy, everybody’s action junkie cousin has decided that the surest, quickest path to riches is trading.

The more leverage, the better. And even better than that, let’s use options so we have an expiration date and know exactly how long we have before we must cash in our massive gains.

Most mutual funds do not match the index returns. Moist individual investors do not match the returns earned by mutual funds. And most short-term traders lose money—lots of money.

We overtrade and chase stories.

The concept of staying in for the long run can be compelling. The problem is that if you pick the wrong decades to be long-term buy-and-hold investors, you tend not to do well.

The problem for most of us is that the worst decades usually follow the ones that were awesome and got us all excited about owning stocks after years of strong performance.

The problem is that we are all human, and humans get excited about their money.

Excited people favor emotional thinking over rational thinking. But emotions and the stock market are like bourbon and grapefruit juice: they just do not mix.

Ruthlessly applying common sense to stock markets can make you more money than all the trading schemes promoters ever dreamed up.

There are often huge changes in the markets. The hard part is to recognize them when living in the day-to-day world.

After World War II, you did not need to be a rocket scientist to realize that the war had revived the U.S. economy: the depression was over, once and for all, and the United States was the premier power in the world.

Once the cost of the war began to recede and all those war vets came home and started families and buying things, an economic explosion was inevitable.

U.S. industry learned a lot during the war, and they used that knowledge to turn out cars, washing machines, ovens, bicycles, baby buggies, and just about anything else the new family could wish to purchase. Homebuilders rushed to build neighborhoods with safe streets, good schools, and white picket fences. Jobs were created making all the stuff people did not know they wanted, and the economy boomed.

On the first day of January 1950, stocks yielded about 7%. The P/E ratio of the S&P 500 was just 7, giving stocks an earnings yield of over 14%

By comparison, high-grade corporate bonds yielded just 2.62%. T-Bills were paying out a little over 1%.

It should have been an easy choice, but stocks were still viewed as being too risky for most Americans. So even though, on average, stocks returned 20% annually in the 1950s, most people missed it.

As the 1960s started, stocks had a P/E ratio of 17, and the yield was down to 3.43%. High-grade corporate bonds paid about 4.4%, and the now available 10-year Treasury paid 4%.

Stocks did okay, with a return of about 7.5%, but things were getting ugly as the 1970s neared.

1968 was a brutal year for the United States. Robert Kennedy and Martin Luther King were both assassinated. The Democratic Convention in Chicago turned into a violent affair with riots and so-called “long-haired freaks” being beaten in the street by Richard Daly’s cops. Congress took U.S. currency off the gold standard. The battle of Khe-San, the My Ai massacre, and the Tet Offensive were in the news and all over America’s televisions.

Stocks were soaring as they had been in the go-go years, and corporate mergers were all the rage. The S&P 500 traded at 18 times earnings. Bargains were so hard to find that Warren Buffett wrapped up his wildly successful investment partnership at the end of the year.

Then, for the next 14 years, stocks were a terrible investment.

The 1970s were ugly. We had not one, but two, oil crises involving our friends in the Middle East. We had Watergate and the first resignation of a sitting President. We had to endure what to me was one of our nation’s low points: disco music. Had it not been for the Grateful Dead, the Rolling Stones, and the Baltimore Orioles, the decade would have been even worse than it was.

Nobody who bought into the long-term buy-and-hold concept in the late 1960s earned any returns over this period. Those who recognized that the world was ugly and stocks were expensive could have purchased corporate bonds and earned about 9% on their money while the insanity swirled around them.

In the early 1980s, there was a massive change in the economy and market, and investors who recognized it made fortunes. Bonds had very high yields, and stocks were very cheap—you could buy high-quality bonds with coupons of over 11% and stocks traded at seven times earnings.

The headlines did not reflect it, but America was ready for change. Paul Volcker was at the Fed, and Ronald Reagan was about to become president. In the first year of the Reagan Presidency, Volcker raised the fed funds rate to 20%, and that was the top in yields. (We have never really come close to that level since.)

Investors in the 1980s who recognized the change in the mood of the country and the waning of inflation made fortunes over the next two decades. But it did not take a rocket scientist to see that valuation had gone beyond high, to stupid levels in 1999 and 2000. Analysts were valuing stocks based on clicks and eyeballs. Earnings were irrelevant.

At the turn of the millennium, we had entered a new paradigm. Stocks had a dividend yield of 1.17%. The P/E ratio of the S&P 500 was 33, giving stocks an earnings yield of just 3%. 10-year treasury bonds paid over 6%, and high-grade corporates yielded 8%. The intelligent choice was bonds over stocks. But no one cared.

If you applied a little logic to economic conditions and valuations, it was clear this could not go on forever.

It is not like there weren’t any warnings.

In 1999, Warren Buffett wrote an article for Fortune magazine suggesting there was no way stocks could live up to public expectations. Jeff Bezos, the founder of Amazon (AMZN), agreed with Warren, telling his employees and the public that they should heed Warren’s warning because a lot of people were going to lose a lot of money betting on the internet.

Over the next ten years, index investors made no money. Tech investors got crushed. As Seth Klarman, the legendary investor who manages the Baupost Fund, wrote in a 1999 report:

Students of financial history can point to historic levels of valuation to suggest that we are in a bubble. However, students of psychology may be needed to complete the picture. For one thing, the financial markets have been so strong for so long that fear of market risk has mostly evaporated. People who used to hold bank certificates of deposit now maintain a portfolio of growth stocks. It is not really within human nature to comprehend that you may not know everything you think you know and, further, that what you believe in could change on a dime.

Investors who applied cold, hard logic and relied on math and not stories could have purchased corporate bonds with yields above 8% and more than doubled their money, while index fund holders lost money.

In the aftermath of the Great Financial Crisis, the Federal Reserve under Ben Bernanke began to take more of an activist role in managing the economy and the market. The Fed started responding to moves in the stock market as much as changes in the economy.

Investors who recognized that the Fed was going to keep rates near zero and that it was going to drive asset prices dramatically higher made a fortune over the next 13 years. Stocks went high. Real estate went higher. And bonds went nowhere.

There is probably a book to be written about the Fed’s turn toward economic activism, but it would take far more time than I want to devote to the effort.

We saw more signs of activism intervention under the Greenspan Fed. When Long Term Capital borrowed enough money and stupidly owned enough illiquid securities with that borrowed money to blow up the world, the Fed got involved and brokered a deal that kept financial chaos at bay. We saw more signs of this leading up to the GFC, but the aftermath of that catastrophe brought Fed activism to the forefront.

I can buy the argument that we needed a zero-interest rate policy (ZIRP) in the short term to prevent collapse. ZIRP is a harder sell for seven years.

Harder still is the Fed taking accommodative action every time stocks sell-off. The era of Fed intervention to protect asset prices was a huge change, and those who recognized it made a lot of money in stocks and real estate. But of course, all those changes were difficult to recognize when you were in the moment.

When valuations were low, and we were at the tail-end of hard times, buying stocks paid off a big deal. When valuations were high, and we were at the tail-end of boom times, the smart choice was to buy bonds and ride it out.

Today, the Fed is letting interest rates rise to fight inflation. The market is allowed to set yields for the ten and 30-year bonds without intervention from the central bank. Fed chair Jerome Powell has no intention of saving the stock market and has made that clear.

The S&P 500 has a dividend yield of 1.65%. The P/E is 24, giving stocks a yield of 4.1%—assuming earnings do not decline as the economy slows, which is a huge assumption. The yield curve is inverted, so short-term rates are higher than long-term rates. Interest rates have stopped going down, breaking a 42-year trend.

Meanwhile, the money market yield is over 5.25%. The ten-year Treasury is flirting with 5%. We can buy BB-rated bonds all day with yields of around 9%. High-grade private credit loans are yielding around 12%. New residential mortgage bonds yield over 7%.

Valuations are high. The mood of the country is sour. The political situation at would be a comedy if it were not a tragedy. There are signs the economy is weakening. There is conflict in the Middle East.

If you had recognized key turning points in the economy and market in the decades since World War II, you would have made an enormous amount of money: catching the key turns of the last 25 years has made you rich.

We’ve had a great run.

But today, it is time to step back from the stock market and look at where we are right now: returns from the stock market from current levels are likely to be subpar. Fixed income returns will be much higher than stock returns.

There is yet another massive change going on that will drive returns that no one is talking about that will make our Underground Income voyage even more profitable: activists are remaking the closed-end fund (CEF) industry.

For decades now, the biggest funds have gone unchallenged. They had too much money and too many lawyers to make it worth it fight with them. Funds issued by industry giants had steep discounts, and there was nothing anyone could do about it.

That is changing. The activists have more firepower than ever before, and they are talking on even the industry giants like Blackrock (BLK)—and winning. The activists will not kill closed-end funds, but the industry will change over the next several years, and discounts will be much narrower.

Buying fixed-income CEFs with activist involvement is going to be wildly profitable as bond yields eventually peak and discounts narrow. If yields stay higher for long, as may well happen, we’ll collect huge streams of cash and benefit as discounts narrow.

As any sailor knows, you cannot change the direction or strength of the wind. You can only change how you rig your sails. Failure to adjust sails when the wind changes will keep you from getting where you want to go.

In the financial markets, the winds are changing; it is time to set your sails.

Using the strategy deployed in Underground Income gives you the perfect chart book and tell-tales to line up your sails to reach your chosen financial destination.

October 4, 2023 - 10:12 am

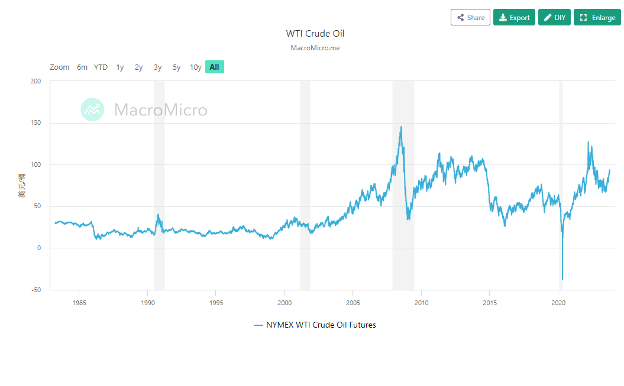

Oil is rising.

So are bond yields.

Once again, Jerome Powell and the Federal Open Market Committee have succeeded in disappointing Wall Street.

It has become a dance that the pair have been doing all year. Powell and the FOMC tell markets that inflation is still higher than they want to see, and they will be data-dependent when it comes to making decisions about raising rates.

They are very insistent that they are open to more rate hikes if it is felt it is needed. Interest rates, they tell Wall Street, will stay higher for much longer than anticipated. And yet somehow, Wall Street interprets that as “happy days are here again.”

Strategists raise the earnings estimate and price target for the S&P 500, but no one talks about the multiple payments for these earnings. And anyone who talks about valuations is old-fashioned and does not understand.

At least one enlightened individual will suggest rather strongly that the Fed will be lowering rates sometime in the next few months. Reading the hard data is nowhere near as important as interpreting the surveys of economists and (apparently) business leaders and traders who are fierce advocates of legalized marijuana.

Markets will rally because everything is fine, and interest rates will drop soon. The economy will boom. Consumers will keep spending money, and job growth will continue without wage growth being a problem.

We will have a most wonderful and magical soft landing for the U.S. economy.

But back to reality: let’s talk about soft landings for a minute, shall we?

The only soft landing that I recall was the end of the recession in the mid-1990s.

Sometimes, tossing facts in the face of stories is fun. Occasionally, it upsets the storyteller, but sometimes, the storyteller needs to be angry.

Over three years, from 1993 to 1996, the Fed raised interest rates from 3% to 6% to tame inflation—300 basis points in three years.

As you can see, inflation was about 3% at the time. The economy kept growing without missing a beat.

So, was it the talent of Alan Greenspan? The genius of Bill Clinton? Or a happy, once-in-a-lifetime accident?

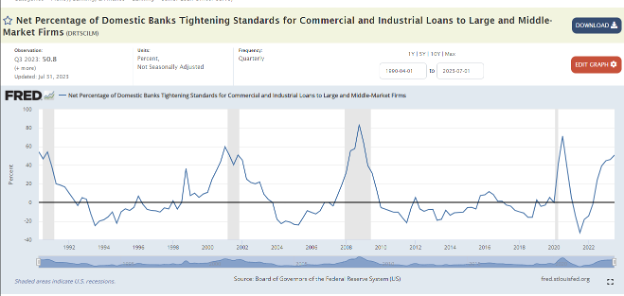

The mid-1990s was a perfect storm of positive events for the United States economy and most of the developed world. NAFTA was passed, and that was good for the U.S. economy. The European Union was formed, which was good for the global economy. The Intel Pentium chip was developed and, in accordance with Moore’s Law, made computing much faster than ever before. The Lithium-ion battery was perfected for commercial purposes, and computing became mobile for the first time. Trade with China was at the beginning of a period of explosive growth. The USSR was gone, and there was only one superpower—us.

The banking industry had recovered from the savings and loan crisis, and bankers were happy to extend credit. Lending standards were not being tightened excessively. In fact, as the Fed began raising rates, most banks were still loose with credit to businesses, and that was good for the economy.

Look at the chart below and compare credit conditions during the “soft landing” to today.

The Fed kept rates stable until Long Term Capital tried to blow up the world in 1998. The central bank had nothing to do with the soft landing.

The explosion of international trade and the rapid advance of technology helped the economy ignore the relatively benign increase in interest rates.

Today, inflation is higher than it was in 1994, even after all the Fed’s efforts to reign in the dragons. Interest rates have gone up 500 basis points in about 18 months. Trade with China is decelerating for more reasons than we have space to discuss. Banks lending standards are very tight. Energy prices are skyrocketing. Oil prices are about five times higher than they were back in the 1990s.

In the 1990s, there were no full-blown wars on European soil to disrupt global supply chains. Europe was not the economic mess it is today. China was not actively working to displace the U.S. on the global stage.

We have seen this movie before.

In 1990, the debate was not about how the country navigated an economic slowdown, the tail end of the S&L crisis, and the junk bond blow-up.

Economists and pundits simply wanted to know how soft the landing would be. For the economy and President George H.W. Bush, it was not a soft landing at all.

In late 2000, a column in the New York Times outlined all the reasons we would have a soft landing. We did not

In 2007, the Dallas Fed suggested we would navigate the subprime crisis with no serious consequences. The consequences surpassed seriousness and danced with catastrophy.

I do not know precisely what the economy will do over the next several months. The data suggests that we will have an economic slowdown that leads to a mild-to-moderate recession. It might be worse than that, but at this point in time, I have no reason to think that will be the case.

There is no data to suggest that we will have a soft landing. Instead, the data suggests that we may see one more rate hike, and then that rates will stay high until we have enough of an economic slowdown for the Fed to feel that rates can be lowered by reigniting inflation.

The forecasts and predictions suggesting rate cuts this year are laughable—the Fed will not lower rates this year. The only way Jerome Powell and company would risk kicking inflation back into a higher gear is if we have a massive economic collapse or a catastrophic geopolitical event—I am talking something of the magnitude of Russia firing on a NATO nation or China invading Taiwan.

Higher-for-longer rates, followed by an eventual cut because of a slowing economy, is a wildly bullish scenario for fixed income. In fact, right now, the numbers suggest that is the most probable outcome.

We gain an edge over fixed-income markets by focusing on heavily discounted closed-end funds. We also collect regular streams of income that make it easier to deal with the current high volatility of the markets.

The presence of activist shareholders gives a potential catalyst for capital gains regardless of market behavior. So does the presence of closed-end fund activist investors who share our conviction that the discount is too wide and should narrow.

The fixed-income funds I have highlighted in recent issues should do well over the next year. We should see the Underground Income Triple Play at work. The asset class will improve as the Fed eventually lowers rates, and we will collect high levels of income on a regular basis, usually monthly.

A combination of activist activity and mean reversion should narrow the discount to net asset value, giving us gains that have nothing to do with market movements.

So far, we have only made one purchase of a high-yield focused fund, and even that one focuses on the higher quality segment of the market. The New America High-Income Fund (HYB) invests in high-yield or junk bonds but has focused on the upper end of the market.

About $ 44 of the binds in the fund are double-B rated.

Those who have been with me for a bit know that double-B, or B.B., is the sweet spot of the bond market and offers the best risk-reward combination in the bond market. 40% is rated B.

Most of the bonds in our fund have maturities of seven years or less. A look at the top holding of the fund shows that they own debt securities issued by companies like Ford (F), American Airlines (AAL), Caesars Entertainment (CZR), Vistra Energy (VST), Carnival (CCL) and Occidental Petroleum (OXY).

This is a relatively small fund with about $ 150 million in total assets. It will need to be merged into a larger fund or ETF to narrow the discount. T. Rowe Price (TROW) is the investment advisor, and it could easily fold HYB into one of its massive high-yield funds.

The current discount to NAV is 16.75%. That is well above the ten-year average of about 10%. There are activists and closed-end fund arbitrage shops on the shareholder list. The abnormal discount could begin to attract attention—and if not, changing conditions in the bond market should eventually cause the discount to return to historic average levels.

The fund pays monthly dividends and yields 7.2%.

I added a new energy fund to the portfolio this month.

I have been vocal about wanting to increase our exposure to energy infrastructure. Tracking activist activity has allowed us to add exposure with a fund that is “in play.” Saba Capital has been actively buying shares of First Trust New Opportunities MLP and Energy Fund (FPL).

First Trust has historically been one of the fund sponsors that most activists consider too big to battle. But Boaz Weinstein has made it clear that they will battle—and beat—anyone, regardless of size.

As you can see, the fund owns all the usual energy infrastructure MLPs.

The current discount to NAV is almost 14%. The fund pays monthly and yields 7.1%.

Thanks to closed-end fund accounting, the K1 payments of the partnerships are converted to 1099 income.

I went into deep detail about why we will use fossil fuels longer than the politicians told you during the most recent member’s meeting. That recording is on the website, so feel free to check it out.

As long as we use oil and gas, it will flow through the energy and processing facilities, pipelines, and terminals we own with energy infrastructure MLPs. Those flows will produce dividends that come to us regularly.

All our energy-related funds trade at steep discounts and all have activists and arbitrageurs as shareholders.

September 27, 2023 - 2:12 pm

I want you to buy shares of First Trust New Opps MLP & Energy Fund (FPL) using a limit order near the current price.

I have been looking for more energy funds to add to the portfolio, and the recent filings by Saba Capital led me to this fund.

The activist has been an aggressive buyer of the shares in recent weeks and now owns 8.38% of the outstanding shares.

The fund is currently trading at a discount to NAV of almost 14%.

The yield is currently 7.11%.

Dividends are paid monthly and are reported on a 1099.

Buy shares of First Trust New Opps MLP & Energy Fund (FPL) using a limit order near the current price.

Do not pay over $ 6.75

September 6, 2023 - 11:03 am

What has changed in the world since the last issue?

According to the headlines, there have been enormous changes.

Jerome Powell gave a speech in Jackson Hole, Wyoming. Depending on your preconceived bias, it was either very hawkish or very dovish. Powell clearly stated that interest rates were going higher, or else that they were not going higher.

Banks and commercial real estate are still an existential threat to humanity and will probably cause mass extinction, global depression, and, even worse, stock prices might go down.

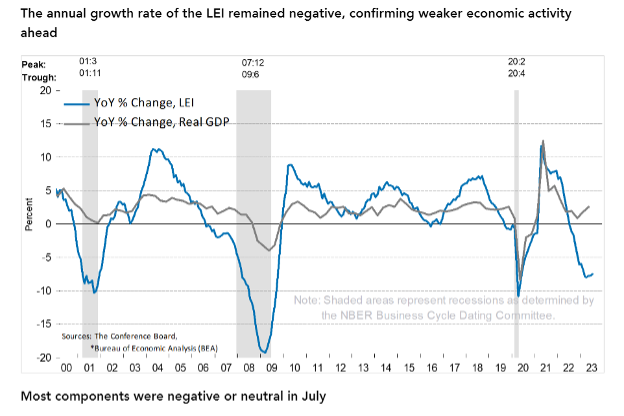

In the meantime, the economy is in fantastic shape except for those pesky weak spots that keep showing up in the reports. There will not be a recession, no matter what the yield curve and leading economic indicators say on the subject.

Inflation is completely tamed. Just ignore what the Fed chair and members of the Federal Open Market Committee (FOMC) are telling us. Do not look at the actual numbers showing that the price of everything but energy and used cars is still moving higher.

The mix of headlines and data is confusing right now. We have an economy that is still experiencing a high inflation rate, and interest rates have risen at a historic pace since last year.

The jobs market has bucked all historical trends and has been much more robust than most analysts expected once rates began to rise.

And consumers have held up much better as well: after an initial rally in 2021, when inflation began to rear its head, commodity prices have become a mixed bag.

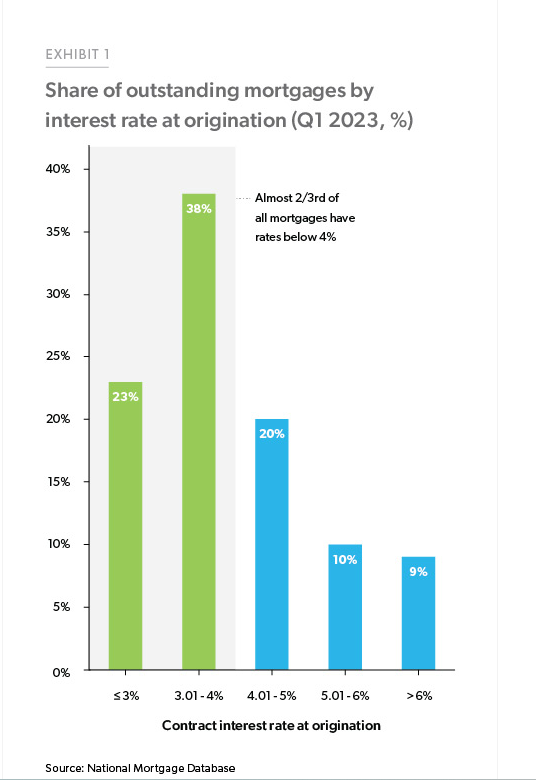

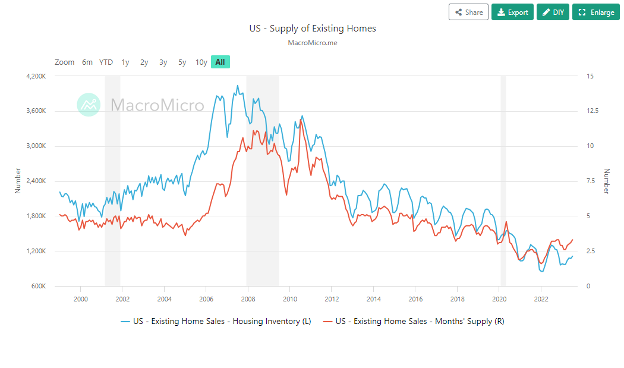

Housing is one of the chief drivers of the economy, so affordability has become a high issue. We have seen some bursts of activity, but the market is struggling to accept the new normal of higher mortgage rates.

It does not help that those of us with sub-4% mortgages (more than 60% of homeowners in the U.S.) have no intention of moving anytime soon.

Existing home supplies are tight, and sales have slowed to a crawl.

https://en.macromicro.me/

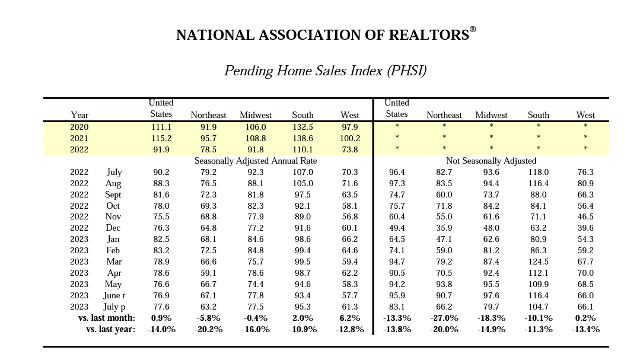

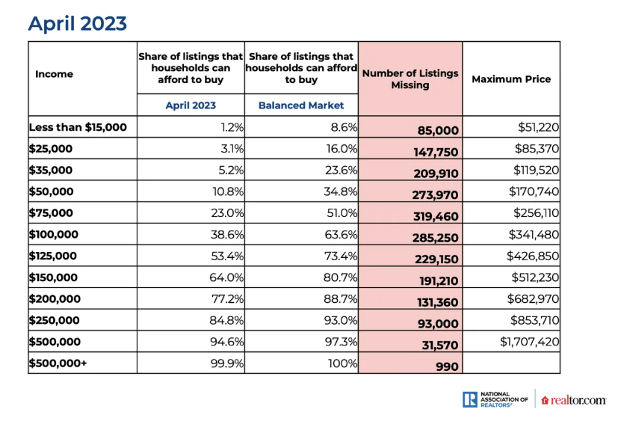

According to the headlines a week ago, the housing market is recovering because of an increase in pending home sales. The leading news outlets and financial media sites report that all is well, and housing will come roaring back. Unfortunately, that is not what the actual data shows, as you can see in the actual numbers from the National Association of Realtors.

Sales picked up from a month ago, but they are still way down from last year.

No one wants to talk about the fact that underneath the headlines, economic activity is clearly slowing.

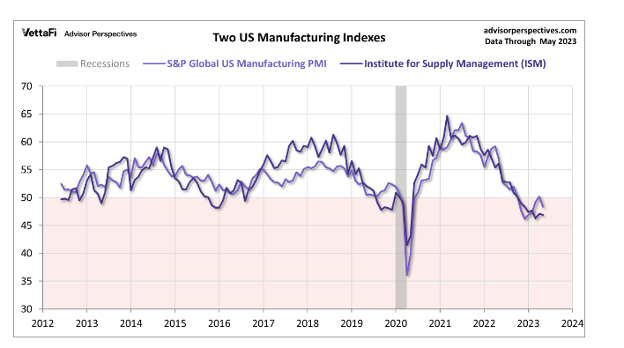

If you look at the recent U.S. Purchasing Manager Index from S&P Global, it becomes clear that the wonderful economy the headlines present are a bit light on actual information.

The opening paragraph of the PMI release pints a much more stark view of the economy:

U.S. firms signaled a slower rise in output during August as activity teetered near stagnation across the private sector. Manufacturers dipped back into contraction as production fell again, while service providers saw growth slow to the weakest since February.

Manufacturing was especially ugly:

At 47.0, down from 49.0 in July, the S&P Global Flash US Manufacturing PMI signaled a solid deterioration in operating conditions midway through the third quarter. The decline was the second-sharpest since January, as a renewed drop in output and a steeper decrease in new orders weighed on the overall performance of the sector.

Let me be clear: do not add my name to the list of those who think the world is going to end.

We will not see widespread bank failures, and most commercial real estate problems will be confined to the central business districts where work-from-home practices have changed the demand picture.

Barring some nasty geopolitical turn of events, we will see a nice normal mild-to-moderate recession. It has been inevitable since the post-pandemic cash injections into the economy caused inflation to rear its ugly head.

There is a lag between rate hikes and economic slowdown. Fed actions have lengthened this lag to offset the carefully manufactured banking crisis and persistent spending by state, local, and federal government agencies. While delayed, it has not disappeared, and we are now starting to see the first signs of a slower economy in some of the data.

There will be fits and starts along the way, but the odds still favor a meaningful economic slowdown.

For us, that is fantastic news.

We have been building a position in heavily discounted fixed-income closed-end funds for months now. We are not the only ones who think it is a bargain opportunity, as the leading activists have also been aggressive buyers of these funds.

This has usually been the case. Most of the economic and market data ends up being reflected in the discount levels of closed-end funds. When an asset class is out of favor, retail investors tend to dump shares.

There are no natural buyers for closed-end funds, so the bids tend to fall to levels that reflect steep discounts.

That attracts activists…who then attract us.

I could look at the chart of discount levels and trends of various closed-end funds by asset class and give you a better reflection of what is happening in markets and the economy than you will get from most newspapers and websites.

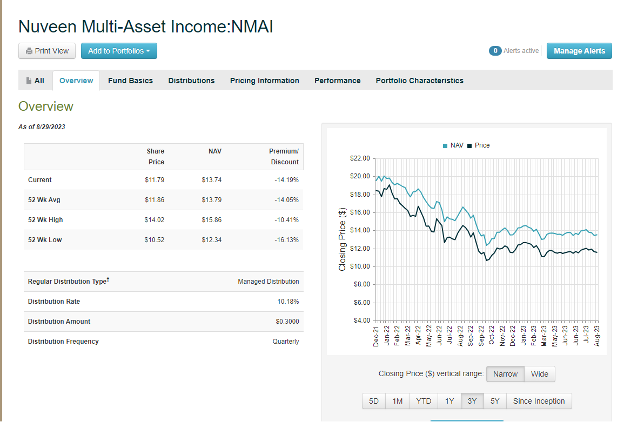

We continued adding to our exposure to fixed income and activities this month by recommending you buy Nuveen Multi-Asset Income Fund (NMAI) shares.

CEFConnect.com

This fund invests in both stocks and bonds from around the globe. About half of the fund’s assets are currently invested in fixed-income and preferred shares; the rest is invested in stocks from around the world. One of the attractions of the fund is that managers apparently share my contrarian bent, and a healthy percentage is invested in out-of-favor sectors like real estate, financials, and utilities. Most of the fixed-income assets are rated BB or better, so it is a higher-quality fixed-income asset. The fund also has large positions in agency-backed residential mortgages and asset-backed high-grade credit securities.

NMAI formed when three funds—Nuveen Diversified Dividend and Income Fund, Nuveen Tax-Advantaged Total Return Strategy Fund, and Nuveen Tax-Advantaged Dividend Growth Fund—merged to create the Multi Asset Income Fund.

The merger created a fund with about $ 650 million in assets that needs to be merged into an open-ended multi-strategy fund.

Nuveen would have been better off merging it into an open-ended fund to eliminate this discount and moving on. Instead, the company just delayed the inevitable.

Saba Capital has been buying shares aggressively and now owns more than 11% of the fund. Saba is tackling the big firms lately and winning, and right now, it appears to have Nuveen (NMAI) and Blackrock (BLK) firmly in its sights.

Other closed-end funds that own shares include arbitrage firms and activists, including Sit Investments, AQR Arbitrage, Wolverine Asset Management, and Millenium Management.

The fund trades at a 14.1% discount to net asset value and yields over 10%.

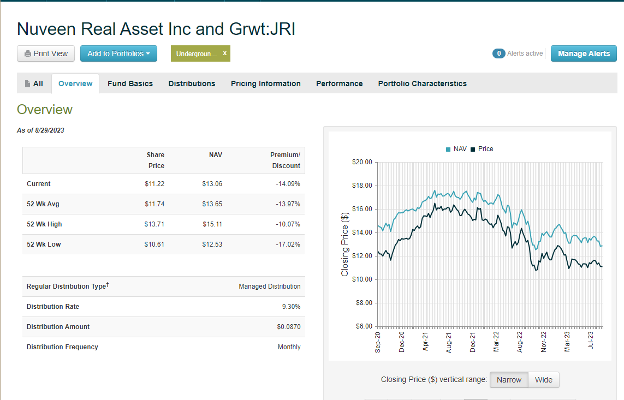

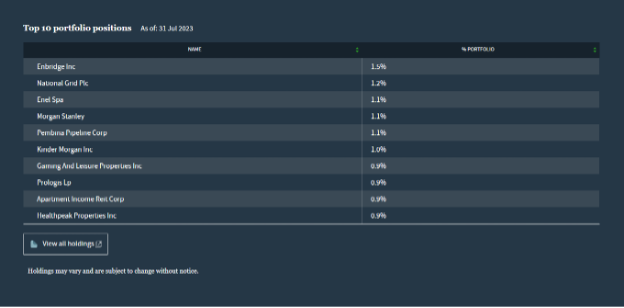

I also added Nuveen Real Asset and Growth (JRI) to the portfolio. This fund owns real assets, including real estate and energy infrastructure, two of my favorite long-term asset classes.

CEFConnect.com

The hard part has been getting real estate at a wide enough discount, and this fund allows us to do precisely that.

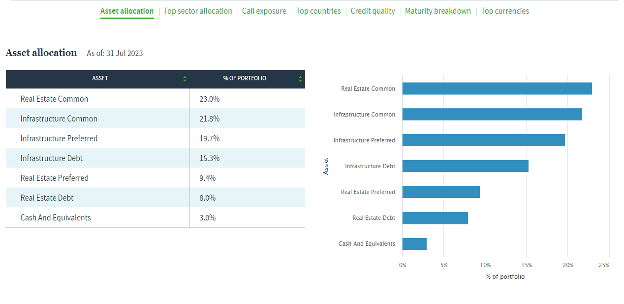

The fund is about 50% stocks and 50% debt and preferred shares issued by real asset companies.

The top ten holdings all fit with major themes we have been embracing and allow us to buy into the major macro trends at a steep discount.

The debt portion of this fund is also mostly BB or better and fits the definition of a high-quality income asset.

Saba Capital is also leading the charge here and recently filed an initial 13d announcing that it owns more than 5% of the fund. Many of the usual suspects are also owners, including AQR Arbitrage, Cohen & Steers, Logan Stone, and Citadel.

The Nuveen Real Asset Fund is currently trading with a 14% discount to net asset value and yields 9.3%

We remain overweight on fixed income and energy infrastructure, and we continue to add to both when we have the opportunity to do so on favorable terms. We are also adding funds with high exposure to real estate when we get the right discount with an activist presence.

We remain almost perfectly positioned for the current environment. It is not my genius as a macroeconomist but the combination of discount and activism that drives the final decision—which, as is often the case, is lining up perfectly with the macro and market conditions ot give us an extraordinary opportunity for robust total returns.

August 29, 2023 - 10:25 am

I want you to buy shares of Nuveen Multi-Asset Income Fund (NMAI) using a limit order near the current price. Do not pay over .92 for shares of the fund.

This is another smaller Nuveen fund that is being targeted by Saba Capital. The fund is trading at a 14% discount to net asset values and needs to be merged with a larger fund to eliminate the discount.

Saba has shown no fear when it comes to taking on the larger fund management companies and Nuveen appears to be in their gunsights along with Blackrock.

Several other activist and arbitrage shops have also been buying shares of the fund.

While the fund does have about half its equity in stocks, a dig through the portfolio shows that it holds a lot of the out-of-favor sectors I favor like REITs, financials, and utilities. The manager also said that they thought US markets were overvalued and had begun selling calls against the fund’s positions.

It also owns corporate bonds and mortgage pools that I think have very attractive total return potential.

The yield is a little over 10% and the dividend is paid monthly.

I will have more details in the upcoming new issue.

Buy shares of Nuveen Multi-Asset Income Fund (NMAI) using a limit order near the current price. Do not pay over .92 for shares of the fund.

August 16, 2023 - 2:37 pm

I want you to buy shares of Nuveen Real Asset Income and Growth Fund (JRI) using a limit order near the current market price.

August 2, 2023 - 6:00 am

You must buy stocks. Everybody knows that. All the books say so.

You must be in it to win it. If you missed the ten best days of the market, you did not make any money. You must own stocks all the time and suffer the drawdowns.

That has been the mantra of academics for decades. 401K purveyors, mutual fund companies, and many brokers also espouse this philosophy. And, it has become accepted gospel for individual investors.

Like all alleged great truths, there is some accuracy to it. Long-term buy-and-hold strategies do work better most of the time than trying to trade in and out of the markets.

However, there are periods during which valuations become so extreme it no longer makes sense to have your portfolio heavily invested in stocks. (If you have firecrackers or small missiles to lob in my direction, now is the time to light them)

Research shows that indicators like the CAPE Ratio and the Average Individual Allocation to Equities identify times of over and undervaluation.

The CAPE Ratio is the 10-year average PE ratio of U.S. companies. When valuations are high, returns over the next decade will probably be very low. And when valuations are low, returns will probably be high over the next ten years.

The CAPE Ratio in the United States is currently 31 and change. It is not quite the most expensive valuation in the world (India and Denmark have higher valuations), but it is close.

The CAPE Ratio currently suggests a long-term return, including dividends, of a little over 3.5% annually. But a long-term 3.5% return will not get us where we want to go.

Do not think it cannot happen. From 2002 to 2010, stocks returned a little less than zero. After hitting a high in 1968, stocks did not break even until 1982. In both periods, devastating declines caused many investors to panic and sell everything, locking in huge losses. But if we sell stocks, we will miss all those big up days that provide all the returns of the market.

If we try to time the market, we will be paupers in retirement. At Christmas time, we will have to knit the grandkids socks using yarn from old sweaters and build them toys from driftwood. Forget the country club—we will be reduced to checking out ancient Wii Golf sets from the library and making sure we never return it late and incur fines.

We must stay in stocks no matter what happens, or we will miss all those big gains everyone talks about. It is time in the market, not timing the market—everyone knows that.

At least, that is what the so-called experts will tell you. Like most self-appointed experts in history, they are full of a certain material that falls from the southern end of a northern-bound horse.

There is some truth to what they say, of course; timing the market in the short term is usually a fool’s errand. I know a few people who can do it, but they have advanced degrees in statistics and physics, as well as extraordinary computing power to assist them in crunching numbers. They could explain how they do it, and it is still unlikely we could replicate their achievements.

And of course, they also eat risk like a tasty snack.

It is a rare combination of brain and computing power combined with emotional and fear control that would make First Officer Spock blush with envy. Even with all of that, all the people I have met who do this have blown up entirely at least once—and most of them, more than that.

However, using the CAPE Ratio and the Average Allocation to Equities like a thermometer, we can measure when the market is so hot that we should stop adding cash and instead take some money off the table.

What about missing those best ten days?

As it turns out, missing those days is not that big of a deal. As Meb Faber of Cambria Investment documented a few years ago, both the biggest up and down days usually occur during bad markets. Missing a big up day when the market hits a new bottom a few weeks later means nothing to your long-term returns. And missing the worst days has added more to your returns than capturing the best days that happen in a downtrend.

It turns out that if you can miss the biggest moves up and down, you beat the market rather soundly.

So, what do we do with all our money when it is not in stocks? After all, everyone knows the best long-term results are made by investing in stocks.

While that is true, it is worth considering that investing in income-producing assets when stocks are too risky has been the source of some of the world’s most enormous fortunes.

Consider John Pierpont Morgan, the financier who helped shaped the modern financial system and financed much of the growth of the United States in the late 1800s and early 1900s. Morgan was a banker. He made loans to new industries and, on several occasions, the Federal Government. He was collecting interest.

When markets made extreme moves, Morgan moved in to acquire companies. When a poor economy caused a borrower to miss payments, Morgan would take over the assets.

Most of the time, he lent money and earned interest. He acquired assets in bad times at bargain prices.

Or you may recall Hetty Green, the Witch of Wall Street—we talked about her in an earlier issue. Most of the time, Hetty was a lender, primarily first mortgages on homes and apartment buildings. When panic selling would set in, as it always does, Hetty Green would eventually become a buyer of stocks and real estate at ridiculously low prices.

In between buying opportunities, Green collected interest. And she was the wealthiest woman in the world when she passed away.

In more recent years, Andy Beal of Beal Bank has had a similar investing story. First and foremost, he is a lender who collects interest. But when markets implode, he becomes an investor.

Beal Bank opened its doors back in 1988 and quickly became one of the most profitable banks in the United States. Thirty-five years later, that is still true.

Following discount levels and activist activity allows us to adopt the same interest-collecting and opportunity-seizing style that has built some of the biggest fortunes in the history of the world.

We will own stocks and real estate. I want to own them—especially real estate.

We have a little real estate via our ownership of Principal Real Estate Income Fund (PGZ). In addition to commercial mortgage-backed bonds, this fund owns several REITs, including favorites like Digital Realty (DLR), VICI Properties (VICI), and Alexandria Real Estate (ARE). Best of all, we own these data centers, casinos, and life sciences properties at a discount to the market price of about 13.5% and collect more than 13% in income payments. And several known closed-end fund activists are large shareholders.

I would love to own more real estate CEFs like this, but the discounts still need to be wider to justify the purchase.

We will get there. We will always do.

As for stocks, they remain the flavor of the day.

I would love to buy into some stock funds, especially small-cap value funds, at a massive discount with a strong activist presence. I just can’t right now. There is no consistent activist buying of equity funds.

That makes sense: closed-end fund activists are arbitrage traders at heart. And at their core, all arbitrage traders are value investors. Value investors do not chase stocks when the CAPE Ratio of over 230 and the trailing PE of the S&P 500 is over 25.

As for the Nasdaq 100 index of tech stocks the market has been in love with this year, the P/E ratio is over 40. The average stock in the index trades at a whopping 16 times the value of the net worth of the individual businesses.

That is not value investor territory.

The time to be an aggressive buyer of stock closed-end funds is when everyone hates stocks. When I see a hedge fund manager on TV whose tie is askew and looks like he has not slept in a week, and I can smell last night’s scotch fumes through the TV, I will start getting excited about adding CEFs that invest in stocks. The discounts will be wider than they are now, and activists will be buying.

Until then, we will collect interest from our closed-end funds.

Our collection of energy infrastructure assets allows us to also function as toll collectors. We collect fees on all the oil, natural gas, and byproducts that pass through our pipelines and gathering systems.

For every drop and whiff of energy processed in a facility owned by one of the companies or partnerships, there is a fee paid, and after expenses, we collect the fee as a dividend. Every time a truck pulls up and takes on a load of fuel in one of our terminals, we collect a fee. When a ship enters one of our terminals, we collect a toll.

The solar and wind farms we own in some of our funds charge the energy companies a fee for producing and transmitting the energy.

Every time a car rolls onto the Dulles toll road, a small percentage ends up in our pockets. The same happens on the Chicago Skyway connecting Chicago and Northwest Indiana. We also own a piece of several toll roads in Europe.

Stocks are too expensive. The discounts need to be higher to get aggressive.

Until then, we will clip coupons and collect tolls.

The beauty of that is that the current valuations in fixed income and the slowing in much of the economic data combine to give us returns over the next years that will make be the envy of most other asset classes, including stocks.

Oil and gas prices may fluctuate, but we will turn on the lights every day and move from one place to another. That requires energy. So does turning on the air conditioner, which has become a very popular activity across most of the United States this summer.

Most of the energy produced in the United States comes from oil and gas. Almost all that oil and gas passes through the assets we own via MLPs and energy CEFs, and we collect a toll.

Of course, some of the energy is produced using renewable sources. We collect a fee on some of that as well.

Coupon clipping and toll collecting. This is what the wealthy do until the markets give an opportunity for extraordinary returns from stocks and real estate.

It is also what we are doing here at Underground Income.

July 10, 2023 - 10:26 am

Please sell NXG Cushing Midstream Energy Fund (SRV) using a limit order near the current price.

July 5, 2023 - 8:00 am

“Still the same.”