STOP

Buying Stocks & Bonds

Dear Investor,

Tim Plaehn here…

Speaking to you today because every retirement “expert” has got it all wrong.

And I’m not just talking about your financial advisor…

I’m talking about the entire financial industry.

Just flip on the television to CNBC and you’ll see what I mean…

It’s all a distraction.

Because all these ‘analysts’, talking heads, and advisors want you focused on which stocks and bonds to buy so you pay attention to them.

Well I’m here to tell you that’s not what retirements about.

I don’t know about you, but this is NOT how I imagine enjoying my golden years:

To me, retirement is about one thing and one thing only: Enjoying life.

And you can’t live your best retirement if you’re always wondering if you own the right investments…

Because stocks and bonds won’t pay for your retirement.

But you know what will?

Cash.

Cold hard cash income into your account like clockwork.

So instead of wondering which stocks to buy to get “rich and retire early” or whatever else is out there, you need to do one thing and one thing only: Have a plan.

A plan to NOT buy stocks and bonds in retirement and instead to buy income.

Because to me, a retirement plan must achieve three things:

- Ensure you never run out of money.

- Provides you income even during market crashes.

- Requires little time and is low-stress.

Unfortunately, almost all of the ‘retirement plans’ out there fail to deliver on these three simple rules.

That’s because almost all of them fail to take into account the three biggest hurdles standing between you and the retirement you deserve.

Here’s what I mean…

First, there’s the cost of living.

Thanks to the Federal Reserve’s printing, a dollar today doesn’t go anywhere near as far as it did 20 years ago.

According to the U.S. Bureau of Labor Statistics, what cost $50 back in 1999 now costs $77.50 today… A 55% increase!

Inflation eats away at hard-earned savings… making retirement all the more difficult.

To keep up, your income and investments need to rise an average of 3% per year!

And while the government reports that inflation is low, we all know the truth.

While products like electronics continue to fall in price, the things that matter to retirees continue to jump:

- Over the past 20 years the cost of medical care has more than doubled.

- Food and beverages have surged 64%.

- Even housing hasn’t become cheaper – increasing by 61%.

Things like Social Security and pensions have failed to keep up with these kinds of increases.

This past year, Social Security beneficiaries received a cost-of-living increase of just 2.8%.

Yet the cost of healthcare is expected to rise 6% over the next 12 months, according to Consulting and Research Firm Price Waterhouse Coopers.

There’s only one solution.

By becoming a Dividend Hunter you ensure you’ll never run out of money by making more more every year.

- One of my Dividend Hunter picks now yields over 9% per year after it increased its payout by a whopping 29%.

- Another pick just raised its dividend by more than 7%.

- And one of my favorites just upped the ante by 7.9%.

Just imagine sitting at the beach, knowing that your retirement plan…

- Ensures you never run out of money.

- Provides you income even during market crashes.

- Requires little time and causes little stress.

You’d be well on your way to the retirement of your dreams.

But rising costs aren’t the only threat standing between you and a secure retirement.

Retirement Hurdle #2: You’ve Been Sold This One Big Fat Lie

Next there’s what might be the biggest lie in the investment world today: Capital Gains.

Remember, what I said earlier…

A true retirement plan will work even during the worst stock market crashes.

While the last ten years have been great for anyone counting on capital gains to increase their wealth and fund their retirement…

We all know the stock market doesn’t always rise.

Years can go by, known as “Lost Decades”, where the stock market goes nowhere…devastating the savings of anyone counting on capital gains to fund their retirement.

From 1969 to 1982, again, the market failed to deliver any capital gains:

Imagine retiring at the start of one of these “Lost Decades.”

Yet, Wall Street and the rest of the financial services industry would have retirees sell off their nest egg to pay for living expenses.

Despite the fact that this would be devastating during anything but the best market environments…

I liken it to owning an apple orchard.

You clear the orchard, plant seeds, make sure your trees have water and fertilizer to grow…

After years of hard work your trees finally begin to grow fruit.

You’re now ready to reap the benefits of all that time and effort.

So you take out your axe and begin chopping down your trees!

The local hardware store said they would buy all of the firewood you could bring them.

Wait, that’s not what’s supposed to happen!?

You spent all this time growing these apple trees only to cut them down a sell them as firewood?

Instead of maintaining your orchard, harvesting apples every year, and using the seeds to grow more trees…

You’re now cutting down the trees to sell as firewood??

You would never agree that is a good idea.

Yet that’s exactly what retirees are told to do!

Even if you were desperate for firewood to heat your home, cutting down apple trees is an absolute last resort!

The trees are your valuable cash producing assets.

It’s like that with retirement.

We spend decades working and saving to grow our nest egg.

Then, just as it grows big enough to produce enough fruit to live off of, we start cutting off branches until there’s nothing left.

Wall Street would have us believe this insanity is acceptable.

Despite the fact that it flies in the face of everything I mentioned earlier…that a retirement plan should

- Ensure you never run out of money.

- Provides you income even during market crashes.

- Requires little time and is low-stress.

To anyone that believes relying on capital gains and selling off their nest egg is a retirement plan I ask three simple questions:

- What if you outlive your savings?

- What happens when you’re selling your investments when the stock market is crashing?

- How can you rest easy and enjoy your retirement given your uncertainty to the two questions I just asked?

It doesn’t make sense.

So I set out to do something different.

An investing service that everyone can use to generate a lifetime’s worth of income.

Here’s what a few subscribers have to say:

“…My wife and I are living off of the dividend payments and have seen a total portfolio return of 23% over the past year.” -Tom and Gayle H.

“My portfolio is up $75K since Jan 2016 after instituting your investment philosophy.” –Thomas B.

“Thank you for the valuable service you provide… I’ve become convinced that the best investment approach for me is dividend income.” -Stan P.

It’s like John D. Rockefeller said when asked about his career…

“Do you know the only thing that gives me pleasure? It’s to see my dividends coming in.” -John D. Rockefeller

Rockefeller was the richest man in history.

Were he alive today, economists and historians estimate that he’d have a net worth of $400 billion.

Three times as much as the current richest man in the world, Amazon founder Jeff Bezos!

Rockefeller knew a little something about making and keeping wealth…And that dividends are the best way to make his family rich for generations to come.

Unfortunately, many haven’t taken the hint…

Nothing could be worse for anyone in search of a secure retirement.

The third problem almost every retirement plan out there struggles with is complexity.

You see, to me retirement is meant to be just that: Retirement!

I don’t know about you, but I didn’t work my entire life just to stress about what the market will do tomorrow, the next day, and the day after that.

That’s just another kind of work.

Whenever a talking head on CNBC mentions trading some complex strategy or the latest hot stock, I shake my head.

They miss the whole point.

Any retirement plan that works is doable in thirty minutes a month — that way you have the time to do what you enjoy.

Instead of this:

You get this:

Many of my readers have realized that fighting inflation and counting on capital gains won’t get the job done.

So they conclude that the only way to generate the income they need is with a complex strategy.

Things like:

- Asset blending.

- Options trading.

- Technical analysis.

- Short term trading.

There are numerous investment newsletters, gurus, and media talking heads telling Americans that complex strategies like these are the way to retire.

But with The Dividend Hunter, you’d be a part of a different kind of investment research service.

One that…

- Never uses leverage.

- Avoids complex short-term strategies.

- Buys only the highest-quality, high-yielding dividend stocks on the market.

I believe that if you don’t understand something, it’s best not to do it.

And I want every one of my readers to understand what’s happening with their retirement.

Which is the exact opposite of what the financial industry would prefer.

That’s because…

Despite what you may have heard, financial advisors aren’t paid to help you retire…

To appreciate the power of retiring The Dividend Hunter Way let’s look at the other side of the coin… farming out your retirement to a typical financial professional.

Everywhere you look you’re told that listening to Financial Advisors is the smart thing to do.

That’s certainly what I thought when I became a licensed financial advisor myself back in the late 1990s.

I firmly believed that doing my job meant helping clients reach their financial goals for retirement.

But as I soon realized, nothing could have been further from the truth.

As one of the Financial Advisors at a local bank, my job was less about helping clients meet their financial goals and more about hitting the phones…I was just another salesman.

In reality, my job was simple: Sell government bonds and mutual funds to people who had Certificates of Deposit (CD’s) maturing at the bank.

And as you may have guessed, different investment products had different commission structures…

The broker I worked with who was the most successful (who made the most money in commissions) happened to be pushing the most expensive, high-commission products.

Whether or not they were right for the client.

The conflicts of interest were everywhere… and were enough to make my head spin.

Which is why I eventually walked away.

I had realized…

- A financial advisor’s primary goal is to accumulate assets.

- They would rather not lose money rather than make you a dime.

- Industry-wide conflicts of interests are overwhelming.

With The Dividend Hunter, I’ve created the solution to all these inherent contradictions…

A service that was about research and results and NOT asset accumulation and commissioned products…

The Dividend Hunter Way

When it comes to something as important as retirement, it’s crucial to have a plan that works.

It’s a philosophy I’ve had ever since I was a pilot in the U.S. Air Force.

Back in those days, if you didn’t have a plan you could wind up dead in a matter of seconds.

How did we deal with the risk while flying F-16 fighter jets at 1,500 mph?

We planned for the worst.

And it’s a good thing, too…

Especially on one day in particular.

The day my engine quit on me during a routine maneuver.

Now the first thing you should know about the situation is that the F-16 Falcon is a one-engine plane. So losing that engine is a serious problem.

The next time you fly commercial just ask yourself: What would the pilot do if all the engines went out?

All pilots are trained for moments exactly like this…

And that training is what I put to the test that day.

I was 15,000 ft. — 3 miles — above the landing strip.

As I was going through routine maneuvers I got the warning light…

Then, before I knew it, what the alert had told me was confirmed: My engine was dead.

I immediately called the radio tower alerting them that my engine had quit.

And believe it or not, I was put on hold while they scrambled with what to do.

I realized that if I was going to make it out of this situation, I was going to have to do it myself…

But I wasn’t completely alone…I had trained for this dozens of times.

So I did what any other well-trained pilot would do and put my plan into action… everything I did was automatic.

First, I dipped my nose down by 25 degrees to maintain airspeed while I continued to communicate with the radio tower.

Next, I went through the 10-step engine restart process while simultaneously maintaining airspeed…

Unfortunately, it failed to restart.

I informed the tower that I was definitely coming down…

But there was another problem: I was headed the wrong way.

Which meant that I had to pull off a 180 degree turn with no engine.

The ground was coming to meet me fast…

As I came out of the turn I could see the runway coming at me quickly.

I dropped my landing gear and gripped the stick… carefully maneuvering the plane for a landing.

One mistake and I was a goner.

Then, in the blink of an eye, I was on the ground and skidding to a stop.

I had passed the “ultimate test” of my engine giving out mid-flight, 15,000 feet in the air with flying colors.

To cap it all off, that night at the bar I learned that I had an audience as I put my training to good use: 80 aircraft had been delayed to clear the runway for my landing.

All were impressed… and I’m proud to say I was bought more than a few rounds that night…

It was fun to hear what my landing looked like from the ground.

Best of all, I heard the words “Man, you sure sounded calm and cool without an engine…” more than once.

It had been quite the day, but landing an F-16 Fighter without an engine wasn’t at all lucky…

I had trained for this. My action plan was automatic.

Were it not for that training and action plan, I would have been in big trouble…

It’s the same with investing.

When it comes to the markets, anything can happen.

What you need is a plan…

An action plan that accomplishes all three of the goals I mentioned at the beginning of this presentation.

It needs to:

- Make sure you never run out of money.

- Generate income even during market crashes.

- Be low-stress and hassle free.

And now, I’m going to show you exactly how all three of these ‘retirement plan requirements’ are possible with my brand of dividend investing.

Dividends Are the Path to Financial Freedom

Believe it or not, you’re already on your way to generating all the retirement income you need.

It all starts with knowing where you’re at.

And you figure it out by answering a few simple questions…

- How many years do you have until you retire?

- How much investment savings do you have?

- What do you need to earn each year in retirement to meet your needs and live the life you desire?

If you only have $100,000, $150,000 or $250,000 saved and just a few short years left to retire don’t worry.

If there’s anything my time in the Air Force taught me, it’s that it’s possible to make a plan to accomplish any goal.

That’s why you’re reading this presentation.

You’ve concluded, like so many others, that the way millions of Americans invest and fund their retirement doesn’t get the job done.

And you’re right.

We know that Social Security and Medicare won’t be enough to meet your needs.

Especially since, according to the Social Security Administration’s own annual report, Social Security will run a deficit for the first time since the 1980s this year.

In fact, by 2034 Social Security’s Reserves (currently at $2.9 TRILLION) will be completely depleted by 2034!

But that’s not all.

We also know that counting on the stock market to deliver capital gains to fund your retirement is a dead-end as well.

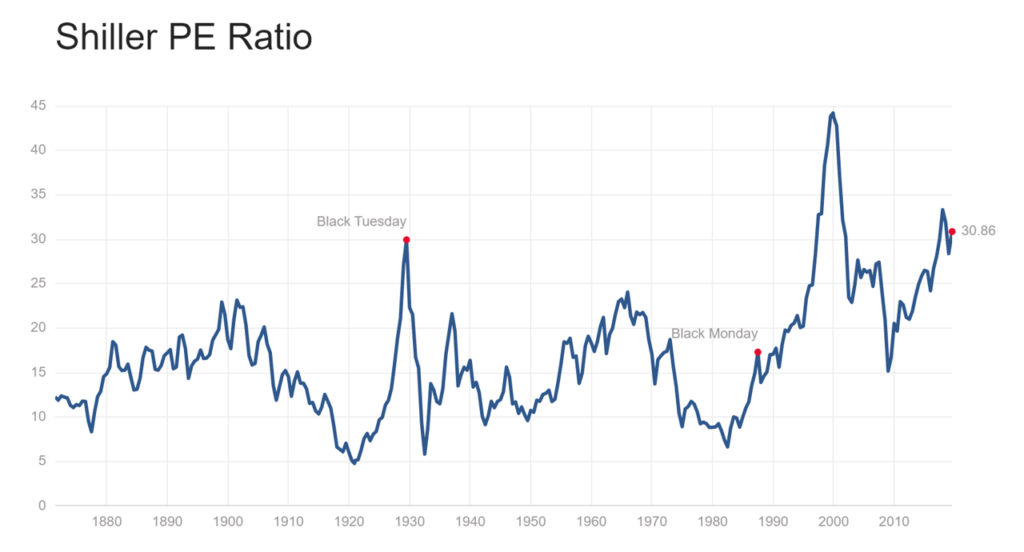

Ten years into a bull market, the stock market now sits at record highs and is now at one of the highest valuations it’s ever been:

At this moment the price-to-earning multiple of the S&P 500 — a measure of how much you’re paying for stock market earnings — is the second highest it’s ever.

In fact, at its current P/E Ratio of 30, the market is at the same valuation it was heading into the 1929 stock market crash.

The only time it’s been higher was during the .com bubble of the 1990s!

And we all know what happened next…

Now don’t get me wrong… I’m not saying we’re on the verge of a crash like the one that happened in 1929, 1987, 2000 or 2008.

What I am saying is that to retire comfortably you can’t count on the stock market’s winning streak to continue.

Yet, as we both now know, that’s exactly what millions of retirees and their financial advisors have elected to do.

Sooner or later, they’re going to get a rude awakening.

A crash isn’t even needed to expose just how dangerous that sort of “plan” is.

If stocks simply stay flat for the next decade, and you withdraw 4% of a $1 million nest egg every year, you’d be down to $664,832.60 by the end of the 10th year.

Not only that, but you’d be living off less and less money as time goes on… with your year 1 withdrawal income at $40,000 but your income in the 10th year amounting to just $27,702!

Repeat that process again and you will have blown through almost $1,000,000 in just 20 years!

Managing your retirement finances like that ensures that the day you retire also marks your “Peak Net Worth.”

It’s the richest you’ll ever be.

I reject all of this… and decided to build a rock-solid system of picking high-yielding dividend stocks that provide the income needed to retire.

You can do it too, starting today.

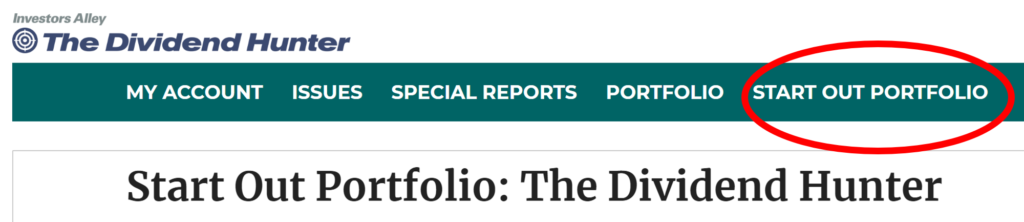

Your journey begins with the Dividend Hunter “Start Out Portfolio”

You see, one of the most common questions I receive from new subscribers is “Which of your recommended dividend stocks should I buy first?”

It’s a valid question.

The stocks you buy first quickly become the bedrock of your retirement income portfolio.

Which is why I created the “Start Out Portfolio.”

They’re so important, these stocks received their own menu drop-down on the Dividend Hunter’s site:

Now as I tell my readers, they’re going to eventually want a high-yield dividend income portfolio of 15 to 20 stocks.

This provides consistent income of thousands per month that can be relied on no matter what happens.

Now obviously, when forming the bedrock of any income portfolio, you know the first picks are going to be good.

The Start Out Portfolio features my best ideas.

Dividend stocks that…

- Pay a high current yield.

- Features payouts that are safe.

- Offer the potential for meaningful dividend growth in the years ahead.

Right now the average yield of the Start Out Portfolio is a juicy 8.8%.

As icing on the cake, because these are my best ideas, these stocks also offer the chance for capital gains.

Here’s just a taste of what’s inside:

- The first two Starter Portfolio picks are my top two REIT plays — one of which currently yields a whopping 12.7%.

- Next I advise new Dividend Hunters to pick one of two commercial mortgage lenders, with the highest yielding paying investors a juicy 9% per year.

- No retirement income portfolio would be complete without an energy infrastructure play, with my top pick in the sector paying out an incredible 17.5% per year.

Right out of the gate… you could be making 8% or more.

Which is incredible, if you consider the market’s average return for the past 100 years has been exactly 8%.

That’s no coincidence.

Becoming a Dividend Hunter means more than just investing in the stock market…

It means you’re going to be generating income no matter what the market does… year after year… quarter after quarter… month in and month out.

The Dividend Hunter gives you…

Everything You Need to Build Your Own “3 Rule Retirement Plan”

Now you know that generating income from your retirement portfolio is the only path to prosperity…

And by focusing on high-yielding, sound investments you’re instantly on the path that checks off all the boxes…

- You won’t run out of money because you don’t sell assets to pay your bills.

- Dividend checks continue to roll in even during market crashes.

- A well-chosen portfolio can even be stress free and require only a little initial effort.

There’s no denying the fact that for anyone that wants a true retirement, becoming a Dividend Hunter is the way to go.

When you become a member, you’ll have every tool to master income investing and achieve your financial dreams.

Your membership includes:

- The Dividend Hunter’s Monthly Newsletter — Every month you get a review of the portfolio’s results, economic and market analysis.

- Special Reports You Won’t Find Anywhere Else — I don’t only manage one of the top high-yield portfolios around, we also add extra value by giving members in-depth reports that will help supercharge their portfolios. Examples include: “How To Triple Your Income In Under 10 Minutes,” “The Small Business Boom Paying 14 Venture Royalty Checks a Year” and “The #1 Strategy That Turns $25K Into Income For Life.”

- The Monthly Dividend Paycheck Calendar – This innovative product helps you track all your dividends and makes creating your own ‘Private Pension’ a breeze.

- Buy of the Week — Every Tuesday (except the first week of the month) I flag one stock from the dividend portfolio that represents a great buy right now.

- The Dividend Hunter Portfolio — With an average yield of 8%, this is the meat of my income-generating service. Recommendations are broken down into three categories: Conservative Dividend Stocks, Aggressive High-Yield Stocks, and Fixed Income Investments.

- The Start Out Portfolio for new subscribers.

In addition, there’s loads of bonus material.

Including a video my team and I put together titled “How to Get the Most from Your Dividend Hunter Subscription.”

We’ve also just released another video this summer, titled “Five Year Anniversary Portfolio Review” where we look back on the incredible results we’ve produced in our first half-decade.

Everything you need and more to achieve your financial goals.

Now all of this begs the question: What’s all this information and investment research worth?

After all, Wall Street investment firms and high-ticket Financial Advisors can charge thousands per year…

Write down on a piece of paper the answer to this simple question:

Would you become a Dividend Hunter today if a subscription was less than $500 per year?

Great.

Now set that aside for now.

Because there’s one more thing I’d like to share with you today…

Get the Endless Income Blueprint Absolutely FREE With Your Membership

I have something very special to offer you today.

Call it a gift for taking the time to listen to all I’ve had to say.

If you take the leap and take advantage of the Risk-Free Dividend Hunter trial I’ll be detailing in just a few moments I’m going to immediately send you my Endless Income Blueprint.

It’s a compilation of everything anyone with $100,000, $150,000, $200,000 or more needs to create a never ending stream of income.

Endless Income Blueprint Component #1

To do anything well, you first need to understand it.

And if you want to claim the financial future of your dreams, you’ll need the Becoming a Dividend Hunter dossier.

It serves as a primer for what it means to be a Dividend Hunter.

After all, change doesn’t happen overnight.

I’ve already shown why you need to become a high-yield investor to enjoy a real retirement.

This dossier is the “how.”

I’ve seen it time and time again. Someone takes charge of their retirement only to stumble right out of the gate.

It doesn’t have to be that way.

What they forget is that you have to walk before you can run.

Which is why I created Component #1.

Inside you’ll discover…

- An in-depth overview of The Dividend Hunter Philosophy so you’ll know how to succeed.

- A review of who can benefit the most from my approach to income investing.

- Why The Dividend Hunter is unlike any other investment advisory publication and what it means for your wealth.

- What you can expect once you’ve made the decision to invest for dividends instead of playing the “Capital Gain Game.”

- The reasons why investing for income is the best way to set yourself up for a lifetime of wealth and security.

And best of all…

- A step-by-step plan for building your own Endless Income Portfolio.

Even better, you’ll know how to create your own high-paying portfolio.

Endless Income Blueprint Component #2

Once you’ve read Component #1, this is where you go next…

I call it the “Building an Income Portfolio That Lasts a Lifetime”.

It contains all the practical how-to’s of actually setting up a portfolio to receive all the endless income I’ve described here today.

Every piece of this kit is a response to a REAL need that readers have expressed.

Retirement A means having income coming in every single month – and this guide shows you how.

As a bonus, it will show you how to…

- Use the Dividend Hunter’s Payout Calendar to build a monthly income stream.

- Dividend reinvestment strategies.

- Buy and sell rules for long-term success.

- How to put the Dividend Hunter to work for you.

For anyone starting out as a Dividend Hunter, this is a must-have.

One subscriber, Stan P., said it best…

“Thank you for the valuable service you provide… I’ve become convinced that the best investment approach for me is dividend income.”

It details the “nuts and bolts” of an Endless Income Portfolio.

While the next component helps you protect it…

Endless Income Blueprint Component #3

Something big is coming.

As I’ve already discussed, the market moves in waves.

And every so often, capital gains-focused investors can go years without seeing returns.

It’s why one of the biggest fears investors have is a bear market… a market swoon that wipes out their savings.

And if history is any guide, we could be coming up on one of these periods once again.

Which is precisely why this next blueprint component is so valuable.

I call it…

“Sustaining Your Income During the Next Bear Market.”

What you do today very well could determine your financial fate for the rest of your life.

Just imagine, retiring at the start of the most recent “lost decade” – right at the peak of the dotcom bubble in 2000.

Each year you do just as your financial planner advised – selling 4% of your principal to pay living expenses.

And every year, you see your portfolio value shrink.

Down… And down… And down.

This is why I compiled this report.

As we enter our retirement years what we do with our savings becomes all the more critical.

Don’t be one of those investors chasing capital gains… hoping the stocks you own will go up…

That’s how you wind up worrying about your finances….Continuing to work just to make ends meet.

Inside this component you’ll find everything you need to tailor the Dividend Hunter philosophy to achieve the retirement of your dreams – no matter what the market does.

Every day I get an email from someone worried about what the future holds.

How will they retire if the market falls?

These individuals aren’t crazy.

They’re expressing fear about a very real possibility.

They don’t want to leave their retirement to chance …and neither should you.

“I am very glad I subscribed to The Dividend Hunter”

-Johann R.

Dividend Hunters leave nothing to chance.

True “Hunters” focus on how much cash they’re receiving from their investments.

“You have completely changed the way I think about my investments, and I am much more focused on watching my average monthly income go up than I am what the share prices are…” -Jerry M.

Once you become a Dividend Hunter you’ll find there’s nothing holding you back.

In fact, you’ll discover new ways of making money most investors have no idea exist.

Strategies like…

Endless Income Blueprint Component #4

This is my secret weapon.

Lots of “gurus” have secret weapons.

But believe me when I say, this one is in full alignment with the Dividend Hunter philosophy.

I call it…

The “Income Investor’s Secret Weapon”.

You see, Wall Street has lots of ways to make money off Main Street.

My secret weapon takes the fight to Wall Street…

And puts the power in your hands to make outsized profits.

Imagine… turning a dividend stock that yields 5%…6%… even 8% and then doubling that income?

Whenever I mention this secret weapon, and it’s potential to make anyone 10%, 12%, as much as 16% in a single year, peoples’ ears perk up.

That’s because this ‘Secret Weapon’ is the best way to live life to the fullest

And make sure Retirement A…

…is a reality for you and your loved ones this strategy is indispensable.

This strategy is how you go from guaranteeing endless income to becoming wealthy.

“I just want to say what a great system you have introduced me to…”

-Mark C.

“…I made 66% in 45 days’’ -Peg B.

With The Income Investor’s Secret Weapon you’ll be able to turn Wall Street on it’s head.

And start making real income in retirement.

Endless Income Blueprint Component #5

One should always know where they stand.

That’s particularly true when it comes to investing.

Every day I get an email from a subscriber asking me what they should do given their situation.

More often than not, they fall into one of three categories of investor.

What you do at each stage is crucial to your long term success.

Which is why I created…

“Your 3 Phases of Being An Investor and How to Profit” report.

The end goal of this report is to show you what to do at each stage.

That way you’re on the path to enjoying the retirement of your dreams.

All these reports are worth more than $900.

But you get them FREE today.

In fact, I’m about to tell you how I’m going to sweeten the pot.

We’ve talked a lot about having a ‘stress-free’ retirement today.

For most Americans, that means having the confidence you’ll never run out of money.

And part of being stress-free is having someone in your corner helping you at all times.

An expert who can guide you through this transition.

That’s why I’m inviting you to enjoy these three FREE bonuses and much more inside my most popular flagship investment newsletter, The Dividend Hunter.

Start Earning Endless Income With The Dividend Hunter Today!

The Dividend Hunter is my private members-only community where I reveal how to both profit from top-paying dividend companies and see consistent “paychecks” monthly.

You gain access to my personal Dividend Hunter Portfolio.

It’s comprised of stocks I’ve purchased for my own account —

And today, I have a very special offer for you.

A “Thank You” for listening to this presentation.

I’m sure by now you’ll agree that investing for income is the only way to guarantee the kind of retirement we all desire.

Which is exactly why I put together my Endless Income Blueprint.

You have the desire to take your financial future into your own hands to have everything necessary to start earning endless investment income.

To do that, you’ll need each component of the Blueprint:

- Blueprint Component #1 – Becoming a Dividend Hunter. which will be your describes the philosophy behind my style of investing and the Dividend Hunter Worksheet that allows you to fully understand your finances. Value: $49.

- Blueprint Component #2 – Building an Income Portfolio that Lasts a Lifetime that dives into the nuts of bolts of building a wealth-generating portfolio that lasts. Value: $99.

- Blueprint Component #3 – Sustaining Your Income During the Next Bear Marketcontains everything you need to thrive no matter what the future holds. Value: $199.

- Blueprint Component #4 – The Income Investors Secret Weapon is perhaps my most coveted profit-generating secret. Value: $499

- Blueprint Component #5 – The 3 Investor Phases and How to Profit in Them teaches you what to do and when throughout your investing life. Value: $99.

The value of this Dividend Hunter Endless Income Blueprint Kit exceeds $900!

How can you put a price on knowledge and taking control of your financial fate?

And it can be yours FREE with this special offer.

As we’ve learned, anyone can become a Dividend Hunter with the right tools.

But it takes time, discipline, and dedication to truly maximize your gains.

That’s why I started my investment service.

To allow anyone to benefit from the Dividend Hunter philosophy in just a few minutes a day.

The Dividend Hunter’s Endless Income Blueprint is

yours to keep with your Risk-Free Subscription.

Once inside you’ll find everything you need to start earning thousands of dollars per month – a real income that lasts a lifetime.

Get started right now by clicking the button below. You’ll be taken to a secure page to put in your information.

You’ll join thousands of others already benefiting:

Steve L. wrote me saying:

“I have invested just under $100k and my return percentage is higher than my financial agent can manage. Go figure.”

-Steve L.

And this message from Vic B. in Colorado…

I just wanted to take a moment to thank you for your wonderful newsletter and dividend tips. I have subscribed to a lot of stock newsletters in the past and found them to be very hard to understand.

I have tried several newsletters and yours is the only one I have stayed with.

-Vic B.

I am glad to have found The Dividend Hunter and all your weekly updates. The dividend calendar is excellent and I have been using it regularly.

I eagerly await all your updates and thank you for improving my income stream with all your great ideas.

– Jack G.

The Dividend Hunter will be your go-to resource for building Endless Income.

Thousands have already joined.

If you’re serious about creating a long-lasting income, The Dividend Hunter is worth every penny.

The going rate for The Dividend Hunter is $99 a year.

And I know it’s worth far more.

Believe me this is not some “money grab” situation like a lot of other financial publications engage in.

It’s my attempt to open a whole new world of investing success to you.

That’s because I know that when you begin experiencing the kind of success I’ve described here today, you’ll be back for advanced investment training.

Ways of making money that few know of and allow practically anyone to enjoy a stress-free retirement.

Plus, the wealth of knowledge in the Endless Income Blueprint is worth $945.

But all of it can be yours for just $49.

You read that right.

Today, you can get a one-year membership to The Dividend Hunter for a mere $49 investment.

More than 90% off!

$49 in the grand scheme of things isn’t much. You’ll pay more for a nice dinner out — and that’s without the wine.

And that’s to say nothing of the thousands you’ll start earnings per month like clockwork!

I’ve been told $49 is far too low for all the monthly issues, the updates, and the sheer amount of income you could make.

Here’s what some of my current members had to say:

I cannot remember just how I became acquainted with your Dividend Hunter newsletter, but I am truly thankful. The dividend payouts are like clockwork. Set and forget… have already made back my subscription fees plus. Consider me hooked!

— Alan F

“Thanks to your advice, we are now getting money that we were missing out on before. Our first month’s dividend checks will surpass $1,250!

-Pedro T

What a privilege to have access to your sage advice-I’m shaking my head in disbelief at how my dividend portfolio is performing. Thanks again.

— John O., New York

To join, all you have to do is click the button below.

For the amount of value you’re getting, I’d be tempted to offer zero refunds. I can’t afford to waste time with investors who aren’t serious.

However, I want to make it a no-brainer decision for you, so I’m offering you a full year money back guarantee.

At any point, if you don’t find The Dividend Hunter to be worth every penny…shoot me an email and you’ll get a full refund.

In fact, you can even keep the Endless Income Blueprint Components as a free gift.

To join, click the button below.