Could a beat up bank like this really have made you millions over the last 22 years?

Guys, I’m not kidding…

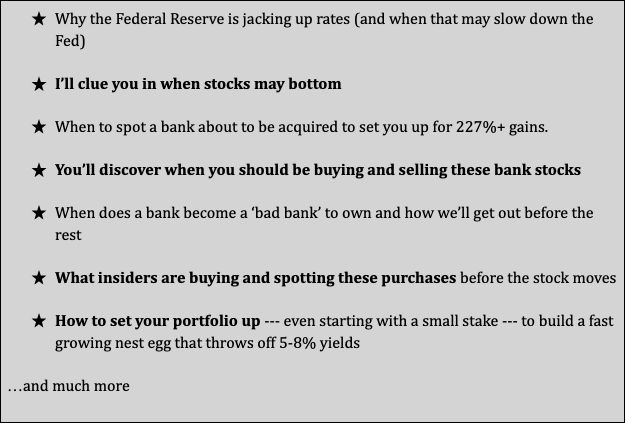

These eyesores are cash cows. There are 174 of them throwing off big money as the Federal Reserve raises interest rates.

I’ll show you the best bank to buy in this bear market for just $16

- Average returns buying these tiny banks would’ve turned $25,000 into $4.1 million despite 3 recessions, real estate crashes, once-a-generation pandemic, and now rapid inflation. Can’t beat that.

- These little banks beat the market 82% of the time. Learned this from the laziest successful man I ever worked with (3-martini Matt)

174 banks want to give you money!

They’re practically begging, “Hey, you! Take our cash! Here’s more!”

While most stocks got wrecked in this rough market…

There are millions of dollars and profits on the line right now from these 174 gold mines.

All you have to do is pick it up.

Imagine a bank depositing over $4.1 million dollars into your 401k tomorrow.

How much income could you generate with that size portfolio?

Just a 5% yield would create you a $205,000 income stream dropped right into your pocket to spend.

You’d have the option to work or not to work.

Spoil the grandkids (like I do).

You would have a nest egg that is safe from any and every external pressure.

No worries about real estate crashes, poor markets, interest rates, who’s President, war, inflation, your grocery bill.

Guys — Banks are handing out this type of massive cash right now to you... no matter your portfolio size.

Now, I’m not talking about the BIG kahuna institutions.

Not Wells Fargo

Not Bank of America

Not JPMorgan Chase

Not JPMorgan Chase

I’m talking about a bank like that one ———————>

And I mean exactly like that.

The small banks you may find hiding behind a Burger King or that suspect taco joint.

Out of 3,711 financial companies… only about 174 fit the bill.

Many are banks you’ve never heard of unless you live in the area.

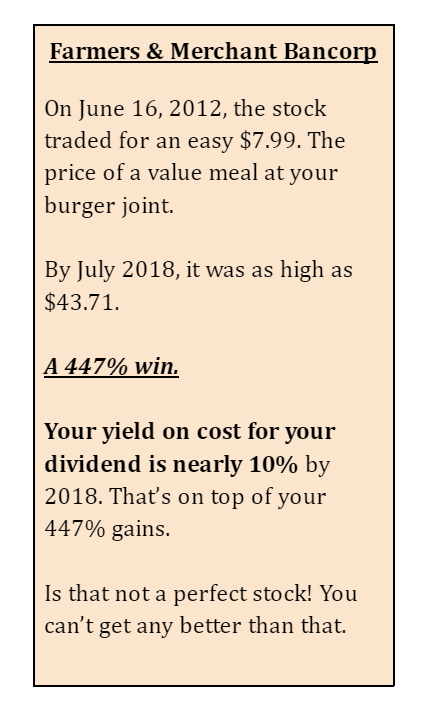

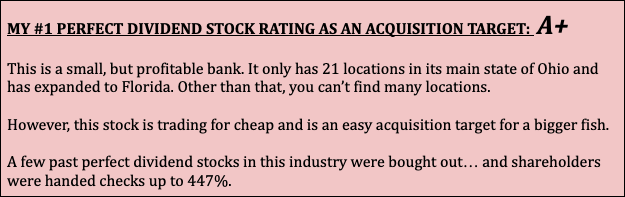

This beat up building here is owned by a small bank that only operates 39 locations in only Ohio and Florida.

Yet, they’re set to raise their dividends by 37.5% this year. And I recommend buying it right now. Today.

I don’t mean drive up to your teller window with a bucket marked “put $$$ here.”

I mean jumping into one of the most lucrative stock market opportunities you’ll find right now.

There’s no physical real estate to buy.

And no board meetings to attend.

Many of these banks are so small… institutions can’t buy them! They aren’t big enough to invest in.

Yet, these little banks are trading publicly.

You just may not know the ticker!

One bank, I also recommend buying, started in a small burrow in Queens, New York…

Their locations go by 13 different names! It’s a crazy story.

I’ll show you where to find these bank money machines right now.

And especially now.

As the Federal Reserve raises rates, you’re making more money than ever with banks.

Banks LOVE rising interest rates, and you’ll see why. Your portfolio will love it too.

My name is Tim Melvin.

Over 34 years…

I’ve tested more than 2,917 stock strategies for the biggest financial companies in the world.

I’m astounded that I’m finally revealing this…

Buying these smaller banks is proven to be the #1 best way to build wealth and income. In any market. Anywhere.

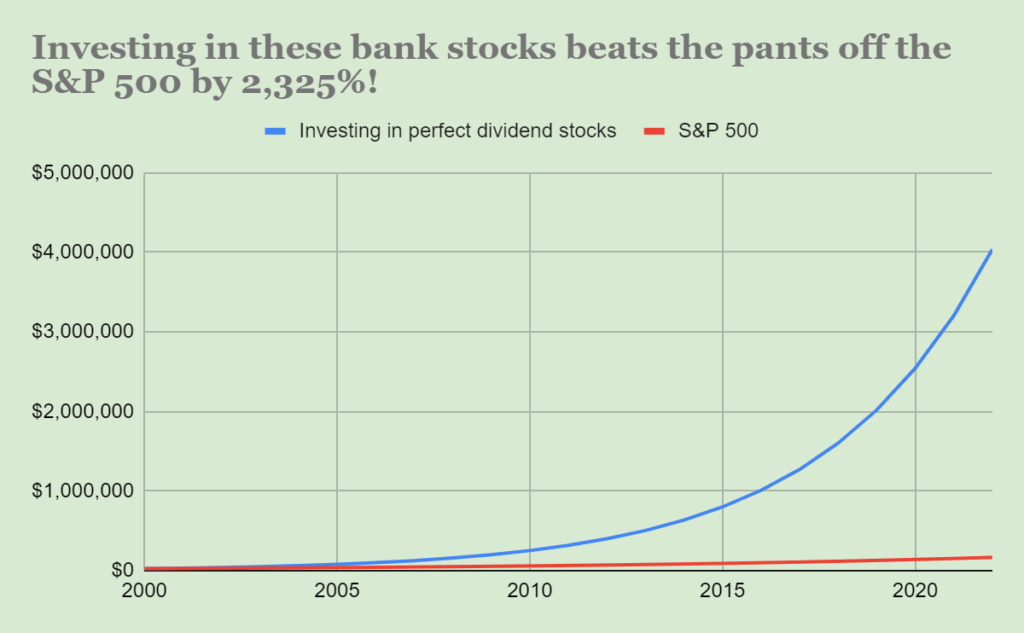

You would’ve beat the S&P 500 by a whopping 2,325% over the last 22 years

This isn’t cherry-picked data either, folks.

This is the average returns if you had bought the exact bank stocks that follow a simple 2-step framework.

This includes buying the winners and losers.

Here’s door #2 everyone else takes.

From January 1, 2000 through 2022…

They “buy and hold” the S&P 500… the gold standard for financial advisors everywhere.

Starting with $25,000… with an average 9% return over that 22 years… you’d end up with around $166,465.

Meanwhile, you’re at club level…

Buying these small banks I’ll show you today…

And could’ve taken that same $25,000…

Through 3 recessions, a pandemic, 40-year high inflation, and war…

You could’ve ended up with around $4,037,309!

That’s a 2,325% difference!

Imagine a multi-million dollar nest egg at your disposal to retire on especially during the hard-pressed times we’re in now.

That’s an annual compounded return of around 26% per year!

Meaning…

These banks have averaged doubling your money every 32 months

Compare that to investing in the “safe” index funds where you expect to double your money in 8-10 years.

How I’ll show you today — you could be doubling your money up to 5X faster.

Now, I’m not promising you that. Nothing is guaranteed.

All I’m showing you is the potential.

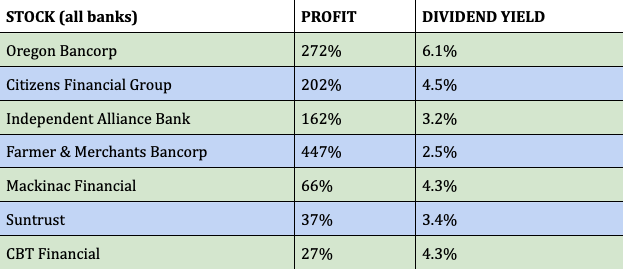

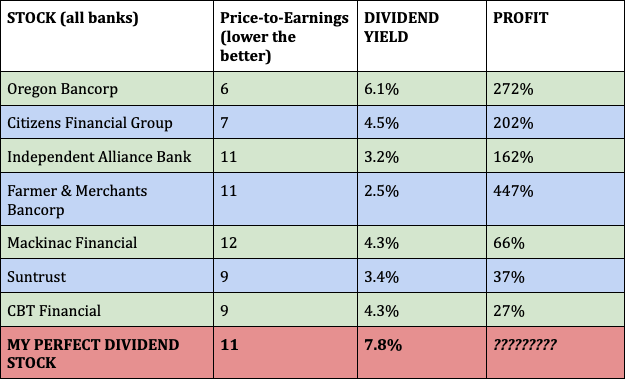

One bank, Oregon Bancorp.

This bank isn’t big.

They only generate around $48 million in revenue per year.

That’s a small company. Amazon generates more revenue than that in 1 hour.

But that doesn’t mean it’s ‘risky.’

It’s just a small bank.

It was May 26, 2018.

Stock traded at $11.28.

By 2021… it had popped as high as $42!

That’s a 272% winner on just owning the shares!

It gets better…

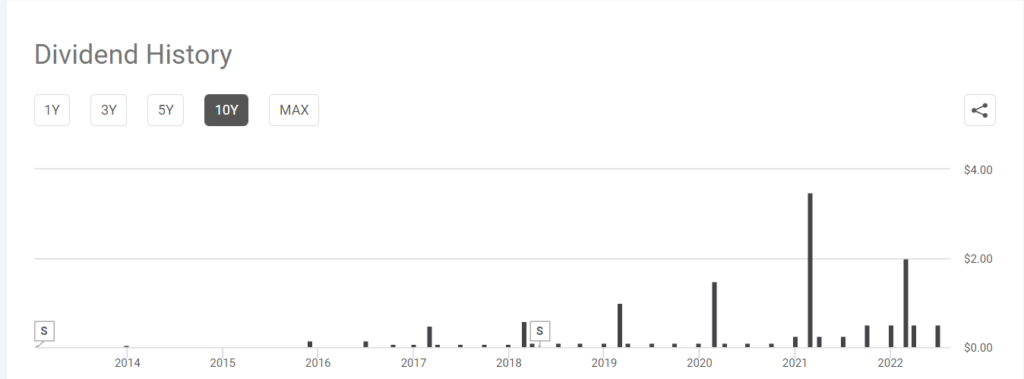

They paid around $1/share in dividends. Now, they pay $2.08… and even have a $2 special dividend to boot!

Their dividends have gone straight up

Yet, here’s the kicker.

There is no building with “Oregon Bancorp” on it!

There are only 18 locations in the entire US. All located in Oregon, Idaho, and Washington State.

No one in Florida (where I am) would ever hear about this bank ever.

Here’s one of their spots in Oregon. Right next to a Firehouse Subs.

You would never notice a bank like this unless you’re dumping your half-eaten sammie outside their door.

Yet, this bank is a #1 ranked small community bank in the entire country specializing in helping local business owners.

That’s special.

Who knew they’re cash cows!

Shares up 272%… dividends going from $0.10… to nearly $3.00 in 9 years. That’s a 2,900% increase in your dividends!

Imagine if you made $5,000 per year in dividends from them.

A 2,900% increase would spike that to a crazy $145,000 per year!

I’m NOT recommending Oregon Bancorp right now due to their price run-up.

However, I’ll show you my #1 bank to buy in a moment which has even more potential (as it’s growing faster).

But, in this environment, you can’t sit on your hands waiting for the ‘old’ days of investing to come back.

Buy and hold is dead.

(even dividend stocks)

Do nothing now and your money may only grow “3-5%” per year,

according to Vanguard.

Yes, Vanguard… guys incentivized to keep you invested in their investment products, believe the forward returns of the market are around “3-5% returns per year”. Kiplinger believes it’ll be around 4.7%.

If inflation stays around 5-8%… you’re losing money every year.

That’s your lifetime savings getting destroyed!

Vanguard, I found, was the nicest of projections going forward. Another analysis projected returns of -3.85% for the S&P 500.

No other projection I found was in the positive going forward.

The Wall Street Journal believes, “This Could Be a Lost Decade for Stocks…”

And CNBC says this is “…. a rare (and worrisome) combination for new retirees.”

As inflation roars, you’re spending more and more of your nest egg just to keep the lights on.

That’s crippling to a portfolio, which is why it’s no surprise:

Running out of money is America’s #1 retirement fear…

And some even fear it more than death!

If you can build a solid nest egg… and invest in the right stocks… you can generate enough income to not only live and pay your bills…

But retire comfortably.

$4.1 million through 3 recessions, inflation, wars, real

estate crashes, pandemics…

Imagine if you had that nest

egg secured already.

It’s not too late.

A nest egg you can rely on creates unlimited opportunity.

An opportunity not only for you to finally pursue traveling, hobbies, whatever you want…

But to create wealth for your next generation.

Have you ever planted a seed for a new tree?

Trees are frustrating because you can go entire years without seeing much progress.

Then… one day… the tree shoots upwards with cool, towering shade, beauty, plus it helps clean the air. Your grandchild swings from a tire on it creating lasting memories.

Wherever you are on your investing journey:

- Near retirement

- Already retired

- Or still far off from retiring

You can still continue to build wealth year after year.

I’m showing you how you can do it with bank stocks.

I already showed you they can pay pretty solid dividends. Maybe not 12+% yields… but you can earn more dividends quickly.

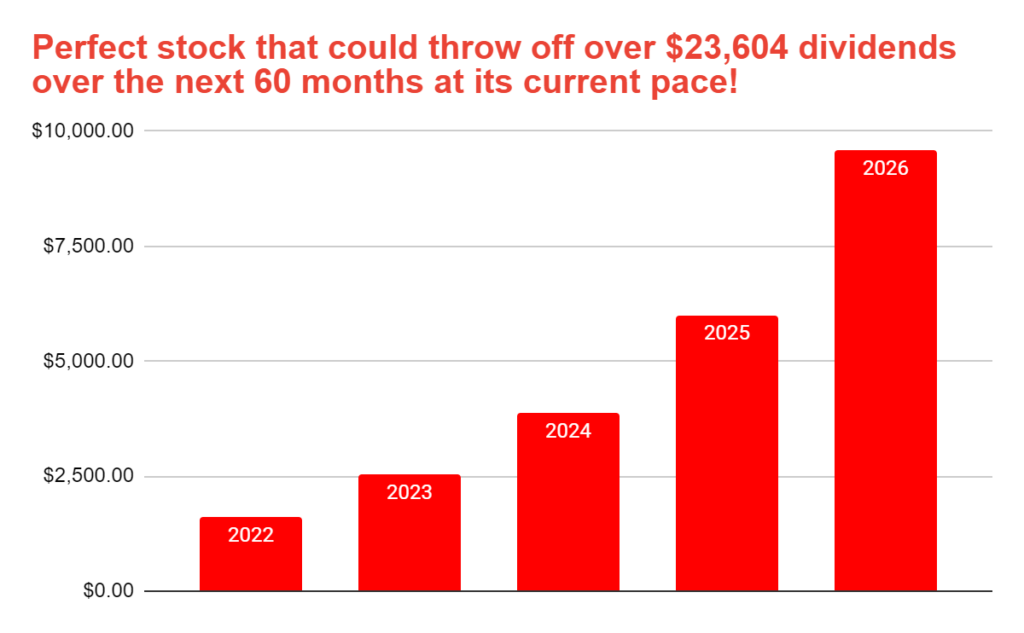

In fact, my #1 bank dividend stock has averaged 37.5% dividend increases over the last decade.

At that rate, you could collect over $23,604 dividends over the next 60 months starting with $25,000.

That’s not guaranteed. Only if they continue at their furious pace.

But that amount of dividends is 94% of your cost basis for shares right there!

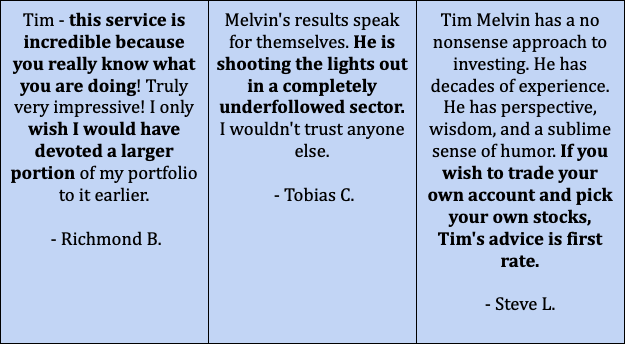

Others who have followed me are very happy.

I’ve heard enough wild promises from other financial media companies that I had to say something

I’m not promising quick riches here.

You won’t make millions overnight.

You’re not trading or running some ‘high risk’ operation here investing in banks.

Let’s be real here. This is not the most exciting investment, and that’s okay.

All I can tell you is I’ve been doing this for more than 30 years.

You can go one of two ways:

- Follow the talking heads for the ‘hot stock’

Or

- Invest in something that is proven to work even if it’s not ‘fun.’

There’s no ground-breaking innovation taking place here. Banks have been around for centuries doing the same darn thing they do now.

That’s why I’m not promising you “get rich quick” anything.

I’ve seen enough editors talk out of their behind about the “new cryptocurrency” and they wash out when everything goes downhill.

You can follow those who chase a quick buck from you.

Or, you can listen to someone who’s been all over the financial industry and has seen it all.

I call my #1 bank stock the “perfect dividend stock” because you can collect returns from 7 different catalysts.

You can’t find that anywhere else.

I’ll share with you the best

dividend bank opportunities

I’ve ever seen in the 3 decades I’ve been

at this stock market thing.

Including managing money for

some of the world’s wealthiest.

Again, my name is Tim Melvin.

I’ve been in the financial services industry for over 34 years serving as a portfolio manager, broker, and advisor.

Now, I’m not like many of the stock guys out there.

I’m old school.

I’m not trying to find the next landmark medical breakthrough, or deciding if Tesla is going to be the biggest company in the world.

I don’t leave my investing to chances.

I have one goal —> Look for inefficiencies in the market.

Where is an asset trading for less than what it’s worth?

We’re talking some real good, old school Benjamin Graham, Peter Lynch, Warren Buffett stuff.

Find the diamond among the rubble and buy it.

My #1 “perfect dividend bank stock” is trading at an incredible price right now.

This is what I find.

That doesn’t mean I’m necessarily buying stocks left for dead.

It’s instead looking for arbitrage opportunities..

Good, sound businesses with great cash flow and a bright future…

But they’re unpopular because they don’t fit in with the current “fad” in investing.

I’m also looking for them to pay a nice, fat, juicy dividend.

If I can buy an asset trading for less than it’s worth… and turn it around and make money… plus, collect dividends… I’m as happy as a guy at the bar on payday.

Finding these perfect dividend stocks takes work.

The work starts before I buy anything.

I’m up late reading financial statements, studying SEC filings, on top of learning about the overall market.

I’m doing this literally every single day.

After taking my granddaughter to the zoo, I drop her back home and I’m off to read SEC filings on a Sunday afternoon.

Studying financials and SEC filings isn’t unique in itself…

It’s knowing how to dig up a value opportunity in the market.

That’s my specialty.

But, that’s not what I always did.

Wasn’t born into money…

I grew up in the Baltimore projects

raised by a single mom.

In high school, we needed money so

I pounded pavement as a door-to-door

salesman to make ends meet.

Sweating my socks off,

getting dogs turned on me for

‘intruding’ on people’s property.

That job prepared me for life.

I owe everything I’ve got to those summers of doors getting slammed in my face.

I didn’t even graduate high school. Got my GED.

Never went to college either.

Yeah, this resume isn’t looking stellar so far.

But what I lacked in formal education I made up with grit and an attitude to never give up.

I got my first job as a broker from cold-calling.

In the early 90s, I saw a column by famed money manager, Victor Neederhoff. He had made an egregious miscalculation about the markets.

I wrote to him and called him out, “Your math is wrong.”

Well, that worked. We met up and I talked regularly with Victor. Eventually being a regular at prestigious parties for Wall Street and the wealthy.

There, I met George Soros and other fund managers you’ve heard of.

What I realized after chatting with many of them was, “These guys aren’t that much smarter than me. If they can make a living from the market, so can I.”

That sounds pompous, but it’s very true.

It was here at the brokerages, this wet-behind-the-ears young buck learned everything I’m telling you now.

I learned important lessons like:

- You can’t generate life-changing returns doing what the average person does

- Don’t fight the tape, meaning, if stocks are really bad, you must be picky about where to value invest

- Illiquidity is where the opportunities are

Many of these small banks are too tiny for the big billion dollar funds.

That’s where you and me with deep knowledge of the space can swoop in and win.

In fact, that’s how I learned this lesson and all about banks.

How did I find these perfect

dividend bank stocks?

I discovered them from one of the most successful stock brokers I’ve ever met — ‘3 Martini Matt’

Matt was a character.

If you looked up ‘work smarter, not harder’ in the dictionary, this guy’s mug would be plastered all over that dang page.

Matt worked alongside me in the brokerage I was employed at.

If Matt got to his desk by 9:30, it was an early day.

And if he left after 4:01, he must’ve lost track of time for a minute.

Meanwhile, he’d duck out at noon… 3 martini lunch with clients… stumble back in for the afternoon lap.

You’d think, “Who the heck is this guy? And how did he get this job?”

Here’s how he got it:

Matt was the best darn stock broker in the entire firm.

Clients lined up to give him their money. I was jealous as heck.

He was one of the richest brokers in the firm.

Matt had houses in Annapolis and a vacation home in Gibson Island (the most expensive zip code in Maryland). Houses go for $1.5 million at the low end here.

Matt had it all.

Like I said, clients begged to give him their money. He was that good. It almost made you think he was doing something illegal.

I mean Matt worked less hours but made more money than those burning the midnight oil.

How is 3-martini Matt beating the pants out of all these other tight wad brokers who worked even longer shifts?

He was doing something different…

So I did what any curious, young buck would do. I walked up and asked him: “What are you doing so well?”

You know what he told me…?

Matt told me, “Melvin…

If you’re not invested in banks,

you’re an idiot.

Banks run everything.”

Banks?

Are you kidding?

That was the secret to it all?

Now, this is a bit dramatized… and Matt’s not his real name.

However, what he told me stuck for years in my brain.

It only hit me a while later…

Everyone overlooks the banks.

They’re boring. It can be as boring as watching golf on television or trying to read a James Joyce novel for the second time.

Boring stuff doesn’t attract money 24/7 like a Tesla or Netflix stock.

Banks like Wells Fargo have been beaten down -13.7% in 5 years and hasn’t recovered to pre-Covid prices…

Goldman Sachs stock only pays pitiful 2.9% dividends…

Banks were decimated during the 2008 Great Recession…

This broker must be pulling the wool over your eyes.

Not so fast, Matt said.

Banks are the heart and soul of America. Of everything, really.

Why buy these types of small banks? Some of them are rundown.

They don’t look like much!

It’s not about what they look like.

It’s about the massive value they provide.

What does this look like?

A rundown warehouse.

Do you know that industrial warehouse space is one of the hottest asset classes in the US!

Amazon, Walmart, all utilize these spaces and they’ve doubled and tripled in price.

And with that stuff comes more self-storage.

These don’t look like much either.

Yet self-storage is also a highly desired space too.

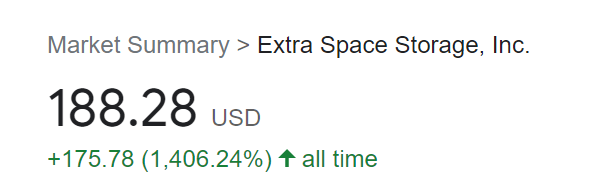

Extra Space Storage (EXR) is up 1,406% in under 20 years. Yes, from boring real estate.

Banks don’t need a fancy get-up.

They control the money flow into the economy. Businesses rarely open without banks being involved. No stock hits the market without a bank. 70% of folks aren’t buying houses without a bank.

If a country was a human body, the bank would be the brain. As they direct all the movements of everything else.

You turn off money. You turn off a country.

Banks have been in existence since 1,800BC in Babylon. They aren’t going away.

Yet, banks consistently are ranked as one of the most boring investments to be involved in.

It’s no wonder banks were Warren Buffett’s favorite investment for decades.

I’m about to show you how banks could be the sexiest investment to have in your portfolio…

My top bank pick produces a nice nearly 8% dividend and trading at one of the deepest discounts in the banking industry.

Ever since then, I’ve watched and studied the banking sector looking for these big winners.

Here’s my tracked return over 8 years

in the banking sector:

I recorded these winners on banks:

- A 165% winner on MFNC over 8 years

- A 100% winner on EVBN in 19 months

- A 150% winner on BOCH in 5 years

- A 163% winner on SVBI in 8 years

- A 192% winner on SLCT in 7 years

Those are just recent trades closed in 2021 and 2022.

Not all my trades were winners… but the last 10 trades closed were all 50%+ winners. Even in this bear market!

How is this possible?

Most investors fail to beat the market.

Period.

There’s two reasons why.

(and why millions will lose their

nest egg in the next few years)

#1.

Peter Lynch had one of the most famous runs ever for a fund manager from 1977-1989.

His fund, the Magellan Fund, returned an incredible 29% return per year on average. That’s unheard of as most hedge funds don’t beat the market. Only 3 beat the market in 2021 out of 3,841. Think about that.

29% is an incredible feat.

Even my bank strategy only returned 26% on average over 22 years.

Yet, here’s the most interesting part…

The average investors inside the Magellan Fund… they lost money.

In 12 years, most lost money despite 29% returns per year.

Was there fraud? Fake reporting? No!

Simple bad habits thanks to human psychology.

When markets are good, we buy. When markets are bad we sell.

You actually need to do the opposite!

I buy good stuff on sale.

If money managers aren’t puking under their desk, I’m NOT buying.

I’m kidding, partly.

I used to be a money manager… and I had many sickly moments during the rough markets of the tech bubble and the 2008 meltdown.

But it was also during those times I finally stumbled on bank stocks.

#2 reason many lose money:

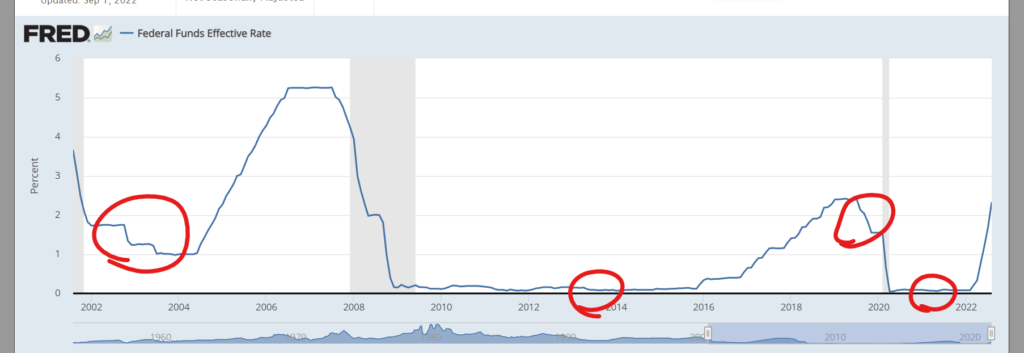

You fight the Federal Reserve.

Do Not Fight the Fed!

So, in the 80s, for us old Wall Street dinosaurs, Marty Zweig was the Michael Jordan of Wall Street.

At one point, he owned the most expensive house in America in Manhattan.

Well, he’d be on Wall Street Week every Friday at 8pm. So we’d all rush home to see it or get our handy VCR set to record it.

It was actually on this show that Zweig predicted the Black Monday crash the Friday before. That’s a wild tale.

But Zweig shared the most important piece of investing I’ll never forget.

He said, “You can’t fight the Federal Reserve.” When interest rates are going up, it is a terrible time to own many stocks.

When interest rates are going down, well, you can pop some champagne and all is well.

This mantra has held up well for most of my career.

And we’re seeing it right now.

Today, being a growth stock or index investor is about as painful as the colonoscopy I just had.

As the Federal Reserve fights 40-year high inflation, they have ramped up rates at a pace not seen since Zweig’s days in the 80s.

Since then, we’ve seen many growth stocks like Peloton get beaten down 91%+.

On the flipside, when Covid hit the markets in March 2020, the Fed dropped interest rates to 0% and stocks recovered in a month.

When the Fed lowers rates, they’re opening the floodgates for banks to lend more money into the economy. Banks make less here as interest is lower. Less interest on credit cards, mortgages, lines of credit etc.

When the Fed raises rates — as they’re doing aggressively right now — banks charge more for credit cards, mortgages, lines of credit… and there’s less money being pumped into the economy.

Less money pumped out means less going into stocks.

That’s why stocks don’t like the Fed tightening.

The problem for many investors, they try and fight the Fed.

They see stocks bottom in June 2022 (as I called) and go aggressive. Stocks bounce back 17% as they do in a bear market rally, but they can then go sideways or drop from there.

As the Fed raised rates to fight the tech bubble in 2000…

Growth stocks took a beating.

And didn’t recover for over 10 years.

The Federal Reserve is battling the worst inflation since the 80s.

They’re raising rates rapidly.

And aren’t cutting anytime soon!

You can’t be in the wrong stocks as this is going on.

Remember, buy and hold is not an option anymore.

You’re risking 3-5% returns… or even negative returns.

Fortunately, these little banks do extremely well when the Fed is raising rates or keeping them steady.

82% of the time buying little banks,

you stomp the market’s returns.

You only get ‘beat’ when Fed lowers

interest rates quickly

*that’s NOT happening for a few years*

Again, this bank investing strategy has returned an average of 26% per year since 2000.

It’s beaten the market single-handedly each year…

Unless the Fed is lowering rates fast.

I circled the only 4 years out of 22 this banking strategy did NOT beat the market.

As you can see, when the Fed is aggressively lowering or keeping rates at 0%… normal growth and blue chip stocks will outpace the banks.

But, the rest of the time, we’re winning.

We even would win, on average, when bank stocks get hammered during the 2008 crisis.

I’ve taken these lessons to amass one of the best track records on Wall Street.

I called the top in 2007

I called the bottom in 2009

I told you to buy more

real estate in 2019

(before prices jumped 50%

in 24 months)

![]()

I warned to get out of

tech stocks in 2021

All of these calls would’ve saved you a ton selling at the top…

And then you would’ve bought at the bottom.

But I’m no ‘blind squirrel who finds a nut’ guy.

I called a short-term bottom on the

exact day in June 2022

On June 20, 2022… after the S&P had fallen 23.4% from November 2021 highs…

I called that we would have a “rip-your-face-off” rally.

Sure enough, the very next day, stocks gapped up and took off the next 30 days. The S&P 500 gained 17% in one month. Some stocks, like Apple, shot up 32%.

But, I didn’t stop there…

Called the market to

drop in September 2022

(dropped 1,000 points one week later)

I told folks, “Things will get a lot worse” despite the bear market rally I just called.

That was early September.

Just a week later…

Called this big drop the week before

Worst day since 2020.

I’ve been helping thousands and thousands more since with my research including writing for Jim Cramer and James Altucher.

What I’m about to show you

with my perfect dividend

stock is what I saw lacking

on Wall Street

Do you know what blows up a portfolio faster than Bernie Madoff?

Pure, stinkin’ greed.

And, working on Wall Street, that’s all I saw.

Brokers taking client money, dumping into risky asset after risky asset. How do you think I was able to call the top of 2007 before the Great Recession?

I saw all this first hand.

Now, I’m seeing the exact same scenarios play out.

So much greed.

With inflated housing prices, stocks like Gamestop going berserk last year…

Even unprofitable tech stocks, like Peloton, trading for insane 20-30x their revenue despite losing 9-10 figures each year.

The only thing that keeps a portfolio going up through thick and thin is dividend stocks.

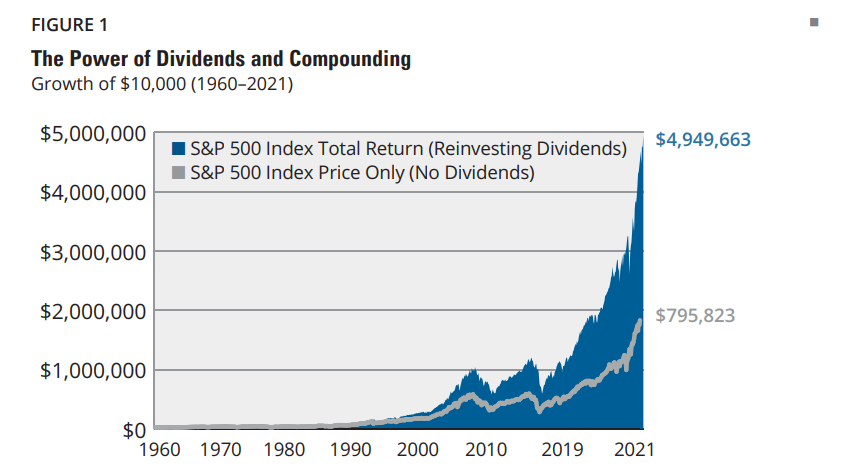

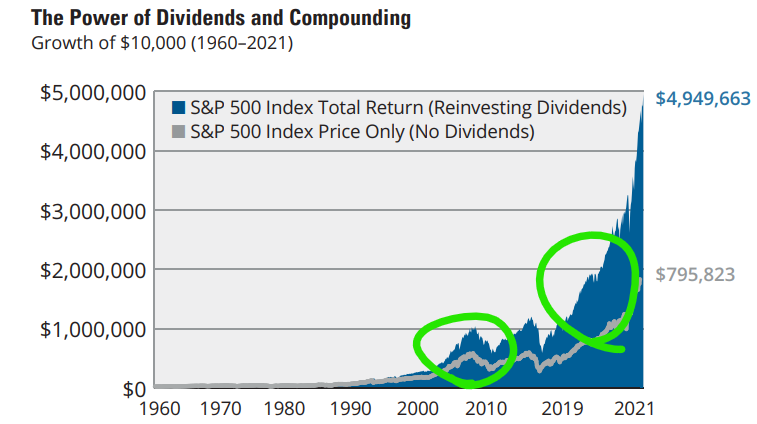

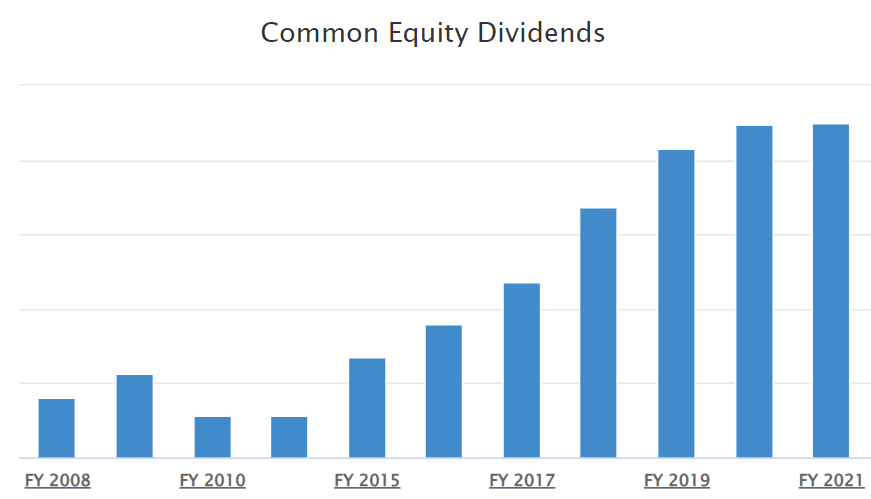

In fact, according to Hartford Funds, check out the power of investing in dividend stocks.

Just buying the S&P 500 without dividends, you’d end up with a portfolio of $795,823 from 1960-2021 starting with $10,000.

With dividends?

Your portfolio is a whopping $4.9 million!

That’s 521% more in your portfolio than if you had no dividends.

But, look closer.

Notice where the big separations take place…

When markets are in turmoil.

That’s because dividends shine like a beacon in a hurricane. It deposits cash when you need it most.

My perfect dividend stock does exactly this… paying 3X more than most ‘great’ dividend stocks.

Why banks right now?

Here’s why banks are an incredible investment right now:

Banks are ‘stronger than ever’ (hold up in the next recession)

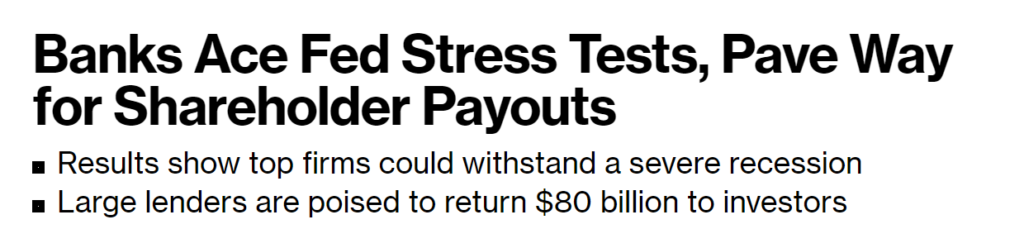

In June 2022, the Federal Reserve claimed “All banks” passed the stress tests.

These stress tests determine if a bank can handle less customer deposits, less lending, and more defaults.

And “All banks” passed with flying colors.

During Covid, the Federal Reserve placed heavy restrictions on banks on buybacks, repo markets, and more.

Now, “no further restrictions” are planned for banks.

Compare this scenario to 2008: Banks were heavily leveraged and once the domino of foreclosures started… it wiped out leveraged banks like Lehman Brothers.

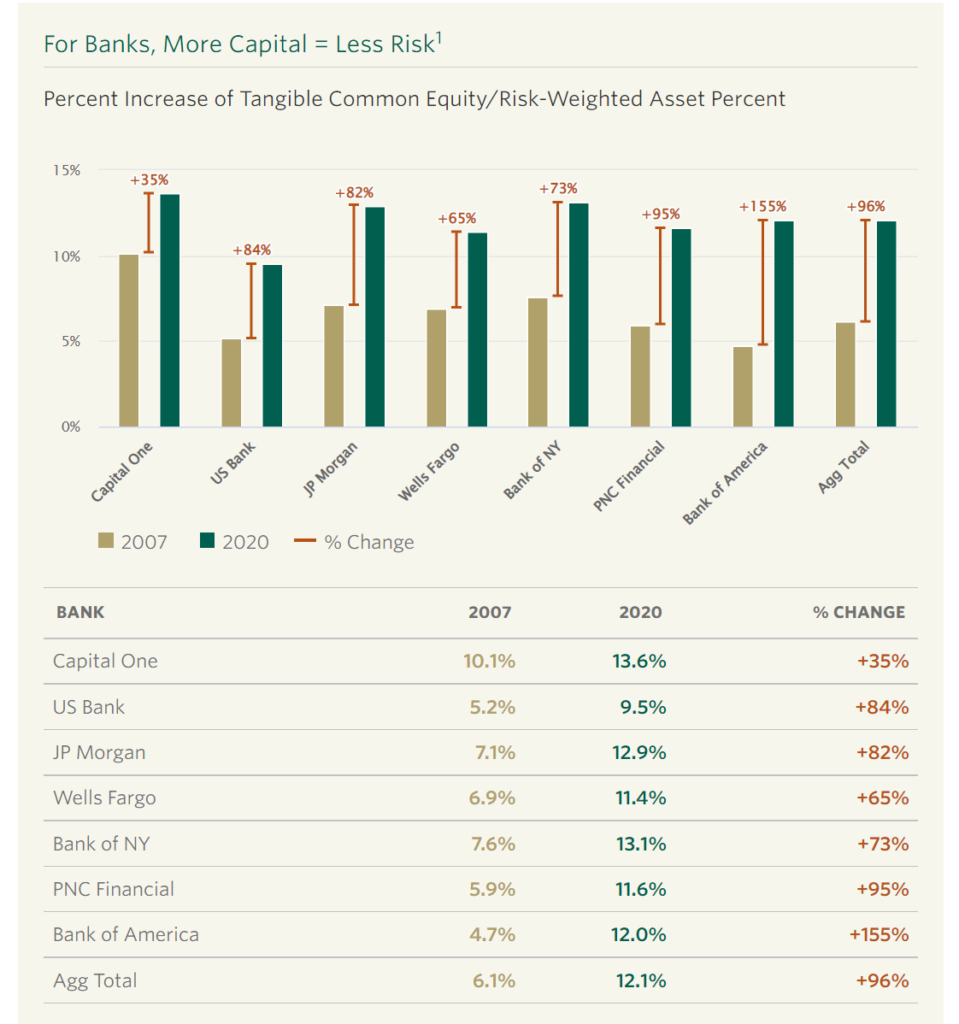

According to the Davis Funds, “Our largest U.S. banks today hold 96% more capital relative to their risk-weighted assets than before the crisis. In addition to more capital, banks have also reduced risk through tighter underwriting standards and a greater focus on compliance.“

This chart compares 2007 to 2020.

Banks are far more capitalized, aka able to weather storms.

If you’re worried a recession will see a 2008 bank massacre… it’s likely not happening.

Banks are heavily undervalued (discounts everywhere)

With the bear market of 2022… many tech stocks aren’t coming back. Ever.

That’s not the same in the banking industry. Remember, we need banks to have civilization. You don’t need an iPad glued to a bike for exercising.

Barron’s claims:

“U.S. Banks are dramatically undervalued.”

Marketwatch reports:

“Bank stocks are super cheap.”

They go on to say, “Bank stock valuations are very low.”

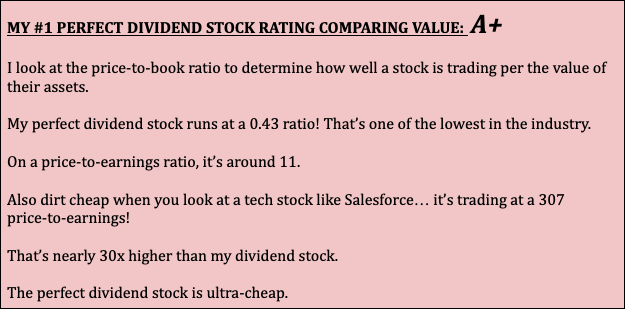

I mentioned my perfect dividend stock trading at one of the lowest valuations comparing price-to-book value. That means it’s trading low right now.

Global firm, Oppenheimer, believes banks will outstrip the S&P 500 going forward.

You’re getting in at the right time.

The banking industry is consolidating (big gains in share prices)

Smaller banks are being gobbled up at a fast clip.

7 of the last 10 biggest bank acquisitions in the last decade have happened since October 2020.

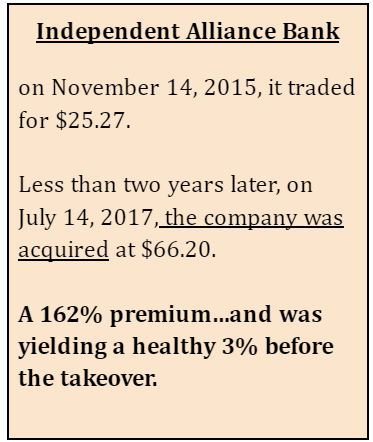

I already shared with you a few stocks that produced up to 162% gains thanks to mergers…

I’ll reveal even more about these stocks and how they’re related to banking.

Banks are buying back stocks in droves (boosts share prices)

Stock buybacks are gifts to shareholders.

The stock count shrinks making your lucky shares a bit more valuable.

My perfect dividend stock is on a buying spree… buying down their own shares annually. Yet, the stock still trades at a mass discount.

That’s the opportunity.

In 2021, banks bought up $75.01 billion back of their own stock.

- Bank of America bought back $25.1 billion

- Citigroup bought back $7.9 billion

- JP Morgan bought back $18.4 billion

Deutsche Bank bought back 300 million pounds.

HSBC took back $2 billion.

But it’s not just big banks…

The smaller, community banks… the ones likely to be acquired… also jumped into the buyback circus.

That’s instant equity in your portfolio when banks are buying back your stock.

You buy the perfect dividend stock…

Shares become more valuable virtually overnight without you lifting a finger.

That alone should perk your interest.

But it gets better.

The very best reason to put my perfect dividend stock at the center of your portfolio is:

Interest rate hikes = massive profits for the banks

I just shared banks are stronger than ever.

Heck, they’re getting stronger as steel.

See, banks are thriving right now in a low interest environment.

Which doesn’t make sense as low interest means loans are cheaper, bonds cheaper, savings accounts are less attractive.

However, we’ve seen interest rates begin the climb up.

Rising interest rates means:

- Boosted bank profits as interest income on loans goes up

Banks earn more in their spreads.

If you think interest rate hikes are going away tomorrow… it’s not happening.

In fact, CBC News reports;

Jerome Powell plans to keep jacking up rates.

Higher rates could attract more big money into bank stocks.

If you follow along with me today, you’ll be first in line before them.

I discovered my perfect dividend stock by following a simple 2-part approach in banking stocks

7 past perfect bank stocks:

I already shared why banks could be setting up for some of their biggest moves in 15 years…

But being a bank isn’t all that puts these perfect stocks in their own, elite class.

PART #1: They must be trading at a remarkable discount compared to their price-to-earnings ratio.

PART #2: They must pay an above average dividend.

Take a look at the past 7 perfect dividend stocks.

But also take a look at my current pick…

It’s trading at a similar price-to-earnings than all the rest did before popping as high as 447%.

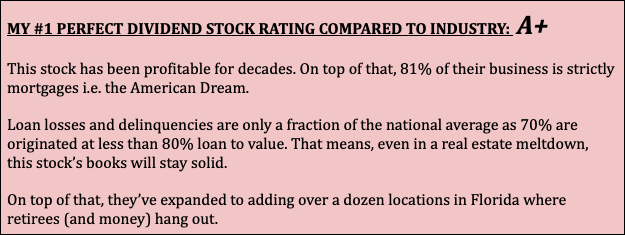

The first bank you’ll buy today started in this rundown building in 1938 during the end of the Great Depression

From this building, a husband and wife team built a small bank to help immigrants of their European heritage.

The business is almost entirely focused on mortgages.

For years, mortgage companies have endured record-low interest rates… meaning, less cashflow in the door.

Now, interest rates are likely to stick around 5%+ for years to come thanks to the Federal Reserve shutting down purchasing mortgage backed securities.

This bank isn’t a monster.

Only 39 branches total across just Ohio and Florida.

They’re underwriting for mortgages is cream of the crop. Their delinquencies are a fraction of the national average rate of 8.22%.

I told you these banks want to give you money.

This bank, in particular, loves their shareholders.

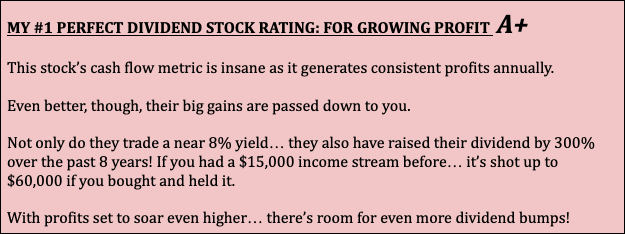

They’re paying a 8.2% dividend yield… and that’s going to keep skyrocketing.

The perfect dividend bank stock

is trading for less than $16

And its dividend could keep increasing

up to 37.5% each year

Meaning, if you start investing today, making $15,000 per year in dividend income…

By next year, you could see your income jump to $20,550 all without lifting a finger.

It’s a stock you can rely on because:

…It pays a yield 3x larger than your average stock.

…It’s grown its dividend 37.5% annually over the past 8 years. That’s 300% growth if you’re doing the math.

…It’s buying back shares annually into the millions.

…It’s in an industry that experts, including the Federal Reserve, have called “stronger than ever.”

…Plus, there are acquisitions quietly happening which can boost share price gains as much as 272%.

… and all in a sector that’s been around for generations and will never go away.

This Perfect Dividend Stock

is trading at one of the deepest

discounts ever seen in the industry

(or even in my 34 year lifetime in stocks!)

If you compare their share price to the book value of the company…

This perfect dividend stock has a freakishly low price-to-book ratio of 0.43 accounting for publicly held stock.

That means the stock trades for below what the company actually owns in assets! If they liquidated everything they owned tomorrow, you’d make money.

To put 0.43 in perspective…

Apple Computers — now a dividend payer — has a price to book ratio of 45! That’s 44X higher… or should I say, 44X more expensive!

A company trading for less than the value of its assets is as dirt cheap as it comes.

In its industry, it’s one of the absolute lowest.

Meaning, this perfect dividend stock is on absolute fire sale.

You can’t buy it at any better of a price.

And once the big money finds out, this stock should rocket higher.

That would make their near 8% dividend yield drop quickly.

You can get in before the smart money and buy this perfect dividend stock starting today.

7 ways to make money from this dividend stock

- Pays a high dividend

- Increasing their dividend double-digits

- Does stock buybacks

- Trading at dirt cheap levels

- Industry is stronger ‘than ever’ as Fed raises rates

- Potential to be acquired

- Industry seeing huge consolidation

My perfect dividend stock is included in

my special report, This Tiny Bank is the Perfect Dividend Stock

Inside, I’ll share:

Inside, I’ll share:

- The ticker symbol of this incredible company

- All the details, facts and more about why this is the perfect dividend stock out there right now

- My strategy on how to dig up these perfect dividend stocks

You’ll now have the perfect bank stock to put at the corner of your portfolio.

Most importantly…

Even if a recession hits…

Inflation runs hot…

The markets go sideways…

I’ve proven that bank stocks like my perfect dividend stock have consistently returned 26% every single year since 1999.

That’s through the tech bubble crash of 2000, the 2008 recession, the bull market after, the Covid crash, and the bear market of 2022.

In fact, if you had started with $25,000…

Investing in bank stocks, like my perfect dividend stock, you could’ve turned it into a cool $4.1 million dollar war chest.

My system for finding these perfect dividend stocks is back tested with incredible results

All you need to do is get your hands on this report right now.

Again, I’ll show you the ticker… but also:

I shared my 2 criteria for finding this perfect stock:

- It’s trading at a big discount

- It’s paying a high yield

These seem simple.

But there’s a lot of behind-the-scenes work that goes into this.

You can’t just buy a bank stock that ‘looks on sale’ with a high yield.

…you need to know how strong their cashflow and balance sheet is.

…you need to know how strong are the loans in their portfolio

…you need to know if the board of directors are on the side of the shareholder (and not themselves)

These are things you can only find in SEC reports, interviews, earnings calls and more.

I’ve been doing this for 34 years.

I’ve worked with the biggest financial publisher in the world.

I called the top of the market in 2007… and the bottom in 2009.

This is my life’s work.

But this is just the beginning…

Out of 3,711 financial companies…

Only 174 banks qualify…

I only want the 10 best ones.

So you must grab this

report now with my

in-depth, private research for my #1 pick

Because if it is bought or goes

up in price too much…

you need to know the next perfect dividend stock

Remember, buy and hold is dead.

You must be ready to invest in the next best bank stocks as prices and valuations change, plus acquisitions close.

I want the 10 best ones to invest in.

…if you’re ready to invest in proven assets that stand strong no matter the market…

…if you’re pumped up to finally invest in opportunities others don’t know about, and your friends will beg you info for…

…if you’re excited about the opportunity to collect dividends, capital gains, boosted yields each year, maybe even a big buyout opportunity…

I’m about to make your portfolio a lot funner place to hang out in.

Get access to my perfect

dividend stock and

the other 9 bank stocks I’m buying

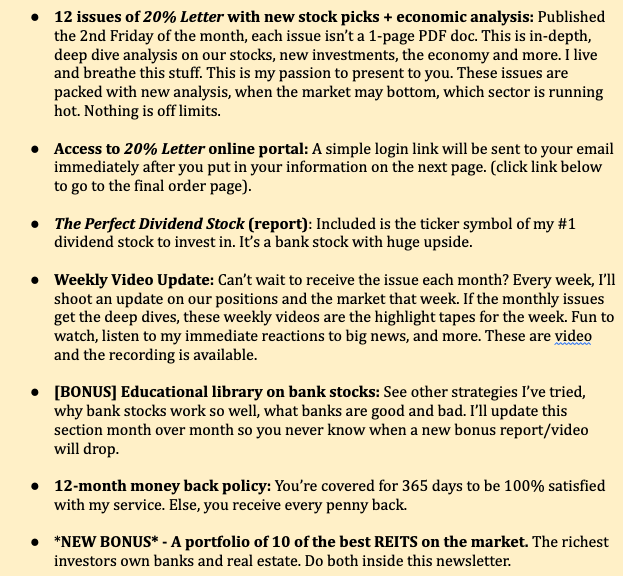

inside my brand-new service, The 20% Letter.

We have one goal with the 20% Letter…

We have one goal with the 20% Letter…

Generate 20% total returns every single year.

That’s share price gains plus dividend yield.

That could be over 12 months or 36+ months. We’re looking to hit an average.

My perfect dividend stock may get bought out, raise its dividend, pay a special dividend… you never know.

It could happen in two months or two years.

Our mission is to consistently hit 20% returns year-over-year.

It doesn’t matter who is President, who’s at war with who, or if we’re in a recession in America.

Remember, over 22 years, this strategy has returned 26% per year based on my back tested system analysis.

But this isn’t about 1 perfect

dividend bank stock.

The 20% Letter is a must-read as a plan for growing your income & wealth

during this tough market

I’ll go into:

Here’s what you get as a new member of The 20% Letter:

This service is easily worth $500 per year.

Especially as I’m giving you the most perfect dividend stock as a subscriber to The 20% Letter.

However, you won’t pay anything near that.

In the future, I expect this newsletter to be at $149 per year.

Why am I starting this letter

now after 34 years?

…Tired of investors like yourself getting rug pulled by algorithms and board of directors who put themselves first.

…Are you sick of being at the mercy of surprise dividend cuts?

…Do you look forward to retiring but are unsure if self-managing your money is ‘for you’ and need that confidence boost?

…Have you been yanked around by plenty of self-professed gurus promising you the moon? (That’s not me)

Have you tried and tried every ‘stock-picking’ service out there and are ready to leave the market altogether?

Don’t back down.

Others are already seeing success following:

The key to success in the market is buying high-quality stocks when they’re discounted.

I’m a value investor.

One of my core rules is to buy stocks trading at low valuations.

You’ll have the #1 perfect dividend stock in your inbox.

But, don’t invest everything into it.

Instead, save some room for these bonus stocks:

90% of banks could be acquired soon.

I’ll show you my #1 bank to be acquired.

Plus, a bonus pick since this is a new product.

Here’s 2 more banks

that could be acquired in the next 24 months

You may have noticed driving around town signs of banks are changing. Suntrust became Truist. First Bank suddenly becomes Fidelity Bank. Wachovia becoming Wells Fargo was big news. Merrill Lynch was famously swallowed up by Bank of America during the Great Recession.

You may have noticed driving around town signs of banks are changing. Suntrust became Truist. First Bank suddenly becomes Fidelity Bank. Wachovia becoming Wells Fargo was big news. Merrill Lynch was famously swallowed up by Bank of America during the Great Recession.

In most cases, it’s not banks are going out of business. Moreso, they’re being acquired. And fast.

At the peak in the 1980s, we had around 18,000 banks and thrifts.

Today?

4,700.

Which is still WAY too much.

Canada only has 35 banks. France has 337. The UK has 334.

We need a 90% consolidation.

Banks are slow growth machines. Bigger banks realized they could accelerate growth (to, of course, boost stock profits) by simply acquiring vs. investing in new locations. This consolidation spree set off in the 1990s as the finance rules laxed.

I have two banks I could see being acquired in the next 24 months:

ACQUISITION TARGET #1: This small bank in Wisconsin only has around $330 million in assets. (JP Morgan has $48 billion to compare). For 95 years, this bank chugged along… until 2017. That year, they dumped 44% of their private stock ownership to the public. That’s a signal they’re prepared to be acquired. In 1Q 2020, they sold the rest. They have until JANUARY 2023 to be protected from a takeover. After that, it’s open season for a big bank to scoop them up.

The largest stakeholders are the employees. They’d all be licking their chops for a big payday.

70% of their assets is in commercial residential real estate. That’s an asset that’s taken off in the past few years and will continue on. A large bank will love this.

This is a tiny bank. A market cap under $100M. No institutions can pump a lot of money into it. That gives you a unique opportunity to scoop up shares for cheap.

Here’s a second bonus bank that could be acquired.

*BONUS PICK* ACQUISITION TARGET #2: This Hawaiian bank is flashing *green light* ready for acquisition. They are 100% residential loan banking… which should be a prime target as prices decline.

Not to mention, they’ve repurchased 32.5% of their IPO shares! Buybacks are incredible for you. To boot, they pay a 4.5% dividend.

They’re trading at a 0.71% tangible book value valuation, which is half what bank buyers are looking for. Meaning, you could see a double up when a bigger bank comes knocking.

I’ll share both of these picks as a free bonus inside The 20% Letter.

Find the picks inside my bonus report, “The #1 Bank About to be Acquired.” I included a 2nd one as a fun surprise.

Get it now… valued at $99… free with your subscription to The 20% Letter now.

The price to join The 20% Letter

is the lowest it’ll ever be.

Just $0.13 per day to add

the perfect dividend stock

To your portfolio today

Remember, I said I plan to raise the price to $149 and stick it there.

However, because the market is in such turmoil right now…

I’m open to cutting the price just this one time.

Rather than $500…

Or $149…

Will you join me for one, low, low price of $0.13 per day? That’s $49 per year.

Click the link below and you’ll have a chance to see this stock moments from now.

$49 is less than a steak dinner for two.

It’s a very good price especially for the stocks I’m sharing that could return 20% per year.

I’m a student of some of the greatest investors — Buffett, Marty Zweig, Peter Lynch.

If you went ahead and purchased all their top books:

Spend more money and time trying to invest like the greats alone.

Or, join me for less and get more.

You’d spend $70.62 before tax. Why spend 44% more and have work to do to read!

Not to mention countless hours having to read these books.

The Intelligent Investor alone is 640 pages.

You’ll be following a similar mindset and approach to the market alongside me…

Not to mention get the actual stock picks to make (you’ll never find that in a book).

Because we’re going to be buying valuable banks at great prices inside The 20% Letter.

Join The 20% Letter by clicking the button below.

It’ll take you to a secure, private page to finish filling out your information.

Click the button now.

12-Month Money Back

Policy

You’ll love what I’ll share else

you can blame me

Investors Alley has been in business 24 years. That’s longer than Motley Fool and Marketwatch.

We plan to be here for decades to come. That’s why we are happy to offer a 12-month money back policy.

Through 365 days, if at any point, you aren’t happy, call and get a 100% refund on your subscription fee.

No questions asked. No hassles.

This is risk-free to join The 20% Letter.

In moments, you too could be on your way to compounding returns year after year.

Returns that absolutely smash the returns of the S&P 500.

Join now for a mere $49.

When you do, I’ll add a special $500 bonus!

SURPRISE BONUS:

I’ll be releasing my first ever

“Perfect Real Estate Stock”

Inside The 20% Letter

I’ll be sharing my top 10

REITS to invest in

Most millionaires I know…

Not the slick, suit-wearing ones…

I’m talking about the blue collar plumbers, electricians, small business owners… they have hefty stakes in 2 things.

1. A cut of your local bank

Not the big Wells Fargo near you.

I mean, the big time business owner in your town is likely on the board or owns shares of the local financial institution.

That’s because banks make bank. Pun intended.

And

2. Physical real estate

Much like bank stocks…

Real estate is something that’s not going away. It’s imperative for society as everywhere you look… someone owns it.

Millennials are late to the buying-a-house party… but, I believe, no matter the interest rates…

That millennial couple walking that baby cart around, they got good jobs, they aren’t going to forego a house. They’ll hoard those pennies.

They want good schools, shopping, entertainment and more.

We shouldn’t see a slow down in the housing market. It’s not going to go straight up like we’ve seen recently, but it’ll stay steady.

Billions have been invested trying to ‘innovate’ in real estate… remember Zillows $800 million blow up trying to flip houses…

Real estate will always be a store of value, cashflow and wealth.

That’s why REITS are the cash cows I’m always happy to invest in.

And I have the “Perfect Real Estate Dividend Stock” to share with you right now.

This is a REIT in the healthcare space and yielding a nice 7.75%.

Even better, shares are trading at just 11x funds from operation which is far below other healthcare REITs.

The REIT leases buildings to medical practices and healthcare systems. It currently has 171 buildings with a 97% occupancy rate. That’s incredible for cashflow.

All the executives have 7-figures of their net worth tied to the stock…

Plus Goldman Sachs and renowned investor, Paul Tudor Jones’ firm, Tudor Investments, just bought up big positions.

As more of the population gets older, having a stake in healthcare is a smart move.

That REIT is waiting for you right now.

I’ll even do one better…

I’ll be releasing a new

REIT investment until we

have the 10 best ones by

this time next year.

To kick off The 20% Letter service…

I’ll be releasing a new REIT investment until we have about 10 REITs total in the portfolio.

My goal is to have 10 bank stocks and 10 REITs for you to invest in.

You don’t need to invest in all of them, but I recommend picking a few to diversify.

To start, click the button below, add The 20% Letter to your cart and you can finish checking out on the next page.

Your first check could already be in the mail in the coming weeks.

My perfect dividend stock is one you likely have never heard of.

It’s trading at a steep discount in the banking sector, raised its dividend 300% and climbing… plus, pays a fat 8% right now.

Other perfect dividend stocks have popped 272% to 447% after ticking all 3 of my indicators.

The banking sector is as strong as ever.

No matter what the market or the economy does, you can be covered and collect cash. Our goal is to try and hit 20% total returns each year.

Join The 20% Letter now before prices go up to $149.

This will become your

little investing secret

Build a potentially

massive retirement nest

egg in just 32 months from bank stocks

that’ve beaten the market by 2,325%

And it’s only going to get better as the Fed raises rates.

Remember, this bank strategy has doubled investors’ money every 32 months.

Imagine the income you could be producing in such a short time.

I’ll show you how to do it.

Click the button below and start now.

That’s all folks,

Tim Melvin

Editor and Founder of The 20% Letter

FAQ:

How much do I need to invest to get the most out of The 20% Letter?

You can start with a few thousand bucks. An account of $25,000 allows you to diversify your holdings a bit.

What returns are we expecting?

Historically, this strategy has generated 26% average annual returns based on my tests. We will shoot for 20%.

Is there a money-back policy?

Yes! A 12-month money-back policy on your subscription fee.

Is this going to work during a recession/bear market?

The backtested track record went through 22 years. That’s 3 recessions, a real estate crash, an oil crash, wars, a global meltdown, a once-in-a-lifetime pandemic, the list goes on. This isn’t like the 2008 bank collapse. Banks are “stronger than ever” and the Fed stress tested all of them with flying colors.

When will I get the perfect dividend stock info?

Click the link below and you’ll be taken to the checkout page. Once you become a subscriber, I’ll email you within 10 minutes.

If there are 174 banks that are generating so much cash… I can find them on my own, I don’t need help!

Wrong. Yes, there are 174 banks that fit my 2-part criteria… but to get to the massive outperformance over the last 22 years… you need to be invested in the 10 BEST ones. That goes far beyond what I can write here. You need to study cashflow statements, the management, debt schedules and more. I’ve done this (and love doing it) for 34 years. For $0.13/day, I’ll do the work.

Aren’t I too late? If this bank strategy worked for 22 years… no way these stocks are successful again.

Remember what I shared at the end here. There is mass consolidation happening in banks. 90% need to be pared down. That means tiny banks are going to do even better… because as interest rates go up… profits go up. As profits go up, these banks become more attractive to big banks. Big banks like higher interest rates for income, but it slows the economy meaning it slows their own growth. Acquisition allows them to grow faster to boost shareholder profits. This tiny bank windfall is only beginning.