Forget Pensions, Social Security, and 401K Withdrawals…

You Need…

The Endless

Income

Blueprint

What Would You Say to $8,100 of Monthly Income?

READ ON FOR A STEP-BY-STEP GUIDE ON HOW TO…

**Generate Lifelong Income**

America is in crisis.

Not from the National Debt…

Foreign Wars…

Or even our current political climate…

No, this is a crisis that hits far closer to home.

I’m referring to the Retirement Crisis.

You see, today Americans have a choice.

To retire in one of two ways.

Call them Retirement A and Retirement B.

Retirement A is the kind of retirement we all dream of…

Quality time with family…

Trips to the beach…

Or simply kicking back and enjoying life…

And then there’s the other kind of retirement…Retirement B.

If you can even call it a retirement at all.

Because it typically means retiring from a job held for decades and starting another one…

Cashier…

Retail…

Even Uber driver.

It’s a reality for MILLIONS of Americans.

And, if you’re reading this I bet you’re unsure of what to do.

The wrong choice could ruin your Golden Years.

But if you had to make the choice today, which would you choose…?

Retirement A on a beach, relaxing and enjoying life with family?

-OR-

Retirement B – Continuing to work day after day just to make ends meet?

The answer is clear.

But as we all know, it’s easier said than done.

Today you’re going to see exactly how to make Retirement A a reality for you and your family.

And once I’m done, you’ll have a blueprint for building endless income to fund your life.

I just ask one thing…

Of course, I can’t stop you.

But believe me when I say skipping ahead will mean missing out on crucial information…

Information that could make all the difference between enjoying Retirement A – the kind of retirement we all desire …

And Retirement B – working for the rest of your life to make ends meet.

To receive the full benefit of what I’m about to share today, you must read every word.

Now, with that out of the way, allow me to ask a simple question:

What are you willing to do TODAY to guarantee ‘Retirement A’ — a leisurely retirement where you savor all that you’ve accomplished in life?

We’ll get to the steps you need to take in just a few moments.

But to fully appreciate it you need to know why the Retirement Crisis is happening and, more importantly, what it means for your financial future.

The facts could not be more stunning…

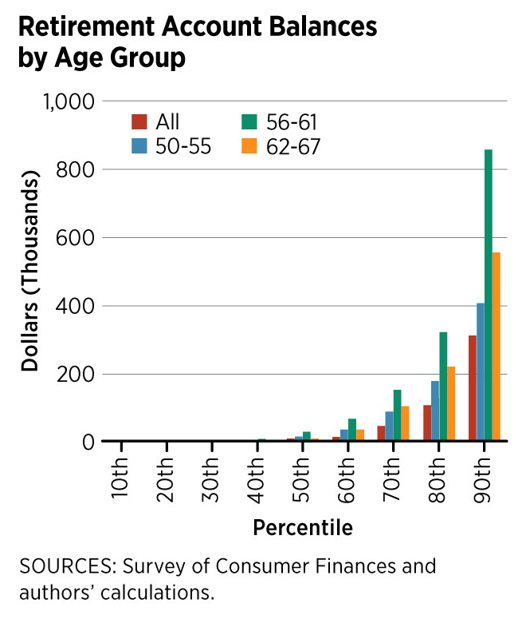

One-in-three working-age Americans have less than $5,000 saved for retirement.

Three-fourths of Americans say they won’t be able to achieve financial security in their lifetimes.

Worse, the U.S. Census Bureau reports that 57% of working-age adults have no 401K assets at all.

And those that do have savings aren’t much better off.

Right now, the average 401K balance for Americans ages 50-59 is $152,700 – not enough to live off of in retirement.

Even when you include Social Security.

And let’s face it, for most of us, employers aren’t much help either.

According to the Social Security Administration, 20% of American workers have access to a pension. That’s down almost 50% from 1980!

Simply put…

Because even if you do everything right…

And make the tough decisions to reach the ‘Promised Land’…

It’s still not enough.

AARP recently made the situation crystal clear, saying…

“…for a retiree to generate $40,000 a year after stopping work, he or she will need savings of about $1.18 million to support a 30-year retirement…”

Even if you plan on living simply one thing is for sure: It’s getting harder and harder to retire in America.

What you need is a blueprint…a roadmap to achieving the kind of retirement they deserve… Retirement A.

A step-by-step “Do It Yourself Kit” for retiring on a stream of endless income.

The solution to all the headlines we’re seeing more and more these days…

My blueprint gives anyone the power to take control of their financial future.

My blueprint gives anyone the power to take control of their financial future.

Because let’s face it: No one is going to do it for you.

In fact, there’s something big standing in between you and the retirement of your dreams…

For decades, financial planners have been preaching “The 4% Rule.”

It’s based on an economic study conducted in 1994 by Financial Planning Guru Bill Bengen.

He wanted to answer a simple question.

How much could you withdraw from a retirement account and have it last for 30 years?

After some number crunching, he got his answer: 4%.

It sounds reasonable enough…

But to get that number, he had to make some assumptions.

Including:

- Modest inflation.

- Average stock market returns of 8% per year.

- At least a 90% chance of your money lasting your lifetime.

It’s a powerful idea.

One that millions of retirees follow today.

There’s just one problem.

One that became all too clear earlier this year:

Why would a large number of Americans suddenly lose their millionaire-status?

Because — surprise, surprise — the stock market went down.

And that’s the great flaw of the 4% Rule.

Just imagine…

You’ve worked your whole life to build a retirement nest egg.

Then one day, it happens: You are a millionaire!

Mission accomplished, right?

Wrong.

Because while for the past 10 years, the stock market has been the place to be:

We all know nothing lasts forever.

And stocks can go down!

Taking a large portion of your nest egg with them.

And that’s exactly what happened to 53,600 soon-to-be retirees around the turn of the year.

In the 4th quarter of 2018, the S&P 500 fell over 14%.

A sizable drop but nothing that hasn’t happened before.

Remember the 2009 Financial Crisis?

We all know that stock market pullbacks happen.

You might even be telling yourself they’re a good thing… that stocks are “on sale.”

But what if you’re counting on those returns to pay your bills?

Suddenly, even the slightest pullback is a BIG problem.

At the start of Q4 2018 187,000 Americans had $1 million or more in their 401K.

By the time the damage was done, that figure had slipped to 133,800.

As it turns out, that 14% pullback was enough to send the number of 401K millionaires down by 28.6%!

The real truth is that the 4% Rule is just about the riskiest ‘retirement plan’ out there.

I’ve seen it over and over.

Stretching all the way back to my days as a stock broker at a regional bank.

It’s why I created the Endless Income Blueprint I’ll be sharing with you today.

The 4% Rule ignores a long list of flaws like…

- How do you retire if you don’t have $1 million or more saved?

- What if you live longer than 30 years past retirement?

- Will there be enough to leave something for your children?

- Where do you go if inflation picks up, which was a major problem in the 1970s?

Then there’s the biggest risk of all…

The market doesn’t even have to go down to have a devastating effect.

Were stocks to simply stay flat for 10 years and you withdraw 4% of a $1 million next egg per year you’d be down to $600,000!

The worst part… you’d have to make that money last for the rest of your life!

Now you can start to see why I call it the “4% Problem” instead of the “4% Rule.”

What I’ve just described happens more often than the financial industry would like to admit.

In fact, the current bull market marked the end of a period just like the one I described…

Everyone knows the stock market goes up over time.

And that’s true – over the long run.

But you don’t get to make decisions over the long-run.

You have to live (and pay bills) in the present.

For example, imagine saying to the electric company you’ll pay your bill once the market rallies back from a selloff.

They’d laugh right in your face.

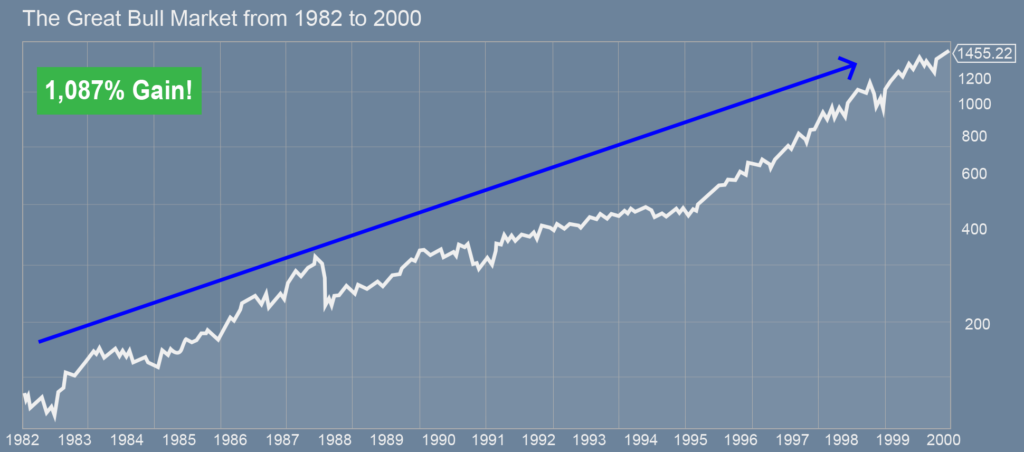

Whenever a Financial Advisor talks about the market going up over time, they always refer to periods like 1982 – 2000:

What they fail to mention is what happened right before the boom years:

Or more recently…

As the old saying goes, “The devil is in the details.”

It’s a decade, or more, when stock market investors see 0% total returns.

A “Lost Decade” would be devastating to Baby Boomers.

Just when they need the market to continue rising the most.

Ask yourself: What if you had just entered retirement in 1968? Or in January 2000?

Not only would your nest egg have suffered….

You would have made the problem worse by withdrawing from your principal at the worst possible time.

Imagine, watching your life’s savings dwindle…

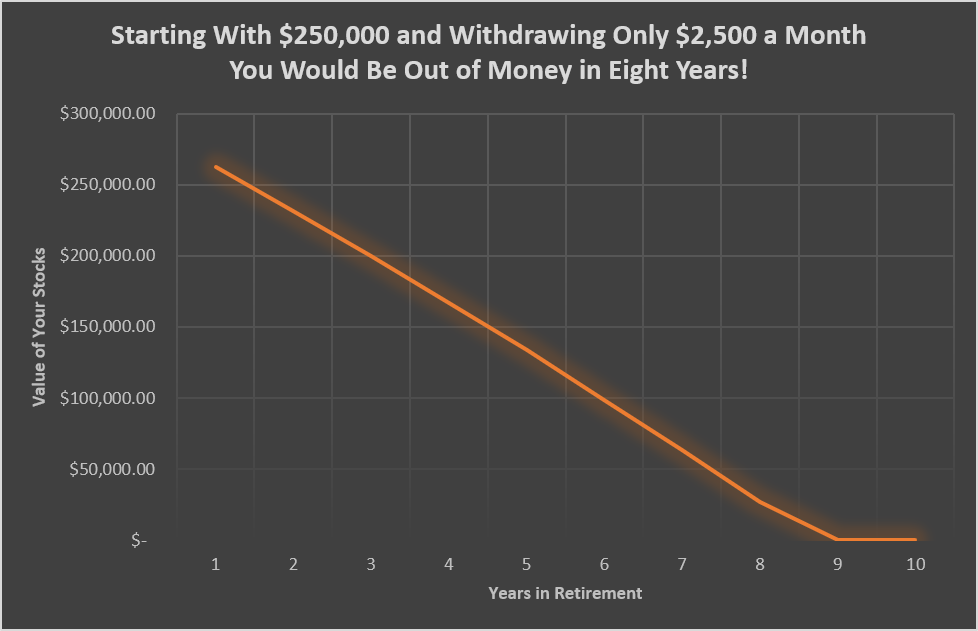

Starting with $250,000 and only withdrawing $30,000 a year (I’d say this is a minimum to live on) you’d be…

Over the ultra-long-term, the stock market is your friend.

But there are periods, even decades, where it’s not.

Fortunately, all is not lost.

I have your solution.

A way to generate lifelong income without ever having to sell off your nest egg.

I call it my Endless Income Blueprint.

A step-by-step guide for navigating your retirement… and building an endless stream of retirement income.

And the timing for you could not be better…

Because if history is any guide, we’re about to experience a period of low returns…

Millions of Baby Boomers are entering…

The Retirement Crisis has already begun.

Starting in 2011, more than 10,000 Baby Boomers started to leave the workforce every day.

By 2013, that figure rose to 11,000.

Since then, this massive retirement wave has only accelerated.

A process that will continue for the next decade.

Not only will this strain Social Security and Medicare.

It’s also occurring at the worst possible time for anyone counting on the stock market for a comfortable retirement.

That’s right…odds are we’re in for another “Lost Decade”.

The reason why is simple.

The stock market has been the place to be for the last decade.

Averaging 14.2% per year.

A $500,000 nest egg invested in the S&P 500 March 2009 would be worth almost $2 million today.

But what typically follows years of above average returns is… that’s right you guessed it… years of below average returns.

Millions of retirees who follow the 4% Rule will be withdrawing from their life’s savings and watching the balance sink lower and lower.

It’s how the market works.

Some time periods are above average.

Others are below average.

That’s the definition of a long-term average return.

Take the 1990s – the previous stock market ‘Boom Period’.

Fueled by tech stocks and a roaring economy, the stock market surged to unprecedented heights:

Even at the peak, there was no reason to think the good times wouldn’t keep on rolling…

But we all know how this story ended.

The “tech-wreck” followed and investors got hit hard.

Had you been fully invested at the market peak, you would have had to wait 15 years to get back to even.

But that’s not what would really have happened.

Had you been doing what the financial industry advises, the 4% Rule, you would NEVER have gotten back to even.

Every year you would have been drawing down your nest egg.

Following the 4% Rule increases your chances that: The day you retire is the richest you’ll ever be.

I call it “Peak Net Worth.”

And the same thing happened to anyone that retired in 1968.

Average returns across these years would have devastated investor savings.

Back then retirees could have survived.

They had pensions and Social Security to fall back on.

Today’s retirees won’t be so lucky.

You can be one of the few that thrives with my…

Think about it this way…

The market just experienced its longest post-War expansion.

How much longer can it last?

I’m not in the business of calling crashes.

Or even Bear Markets.

But I do know history.

Which is why I go with what works.

That’s the beauty of my Endless Income Blueprint.

Once you start following my blueprint, you’ll find it doesn’t matter how long the current bull market lasts.

You’ll be enjoying Retirement A — the kind of retirement with family time and relaxing vacations — no matter what the market does.

You’ll be one of the few who avoids…

You’re told to invest for capital gains.

It’s the foundation of the 4% Rule.

And on its face, it seems like the way to go.

After all, the stock market DOES tend to go up over time.

But as you now know, the devil is in the details…

You can’t count on the market rising to pay your bills.

There are years where it can go nowhere.

Don’t forget it crashes, too.

Which can only mean one thing.

The biggest retirement lie out there…

No matter how much you have saved…

Is that…

“Investing for capital gains is the path to retirement”

Sooner or later, you’ll have to start selling off your assets to fund your lifestyle.

You could even outlive your portfolio.

For example, the average life expectancy is now in the 80’s.

But an average is just that – an average.

What if you live longer?

Heck, even the original study that led to the 4% Rule showed there was a chance retirees would outlive their savings!

Or imagine running into an unforeseen medical bill of $25,000… $50,000…$100,000 or more?

According to Fidelity, an average couple age 65 could need an estimated $285,000 saved just to cover health care expenses in retirement.

So it’s clear now why the day you retire is the richest you could be for the rest of your life… that’s “Peak Net Worth.”

This is true of any retirement plan that requires withdrawing from your nest egg.

Which is why anyone that wants to guarantee Retirement A…

…Needs a Blueprint.

A way to…

- Retire comfortably even if you don’t have $1 million saved.

- Have your nest egg outlive you instead of the other way around.

- Leave something for your children.

- Beat inflation.

And best of all…

- Do it all without relying on stock market gains. I’m going to share this Blueprint with you.

But first…

Hi, my name is Tim Plaehn.

I started out studying mathematics at the Air Force Academy.

And went on to serve as a U.S. Air Force Fighter Pilot.

It was only after my stint as a fighter pilot that I turned to the financial markets.

As a stockbroker and financial planner, it was my job to help my clients retire.

It was at this point in my career I realized that most of the ‘advice’ out there was useless for building a leisurely retirement… Retirement A.

We had all sorts of ways to pick stocks.

Strategies that used…

- P/E Ratios

- Technical Analysis

- Fundamentals

- Market Betas

I knew even then that none of these metrics would help my clients retire.

Because they all target capital gains and the 4% Rule.

Everyone’s goal is to retire comfortably – Retirement A – and you can’t do that by selling off your assets.

I noticed that the wealthiest people I knew all invested differently. They always bought dividend stocks.

It sounded so simple.

They focused on streams of dividend income instead of what the market was doing.

They knew that you can’t always count on the stock market – but you can count on dividends.

I decided that I wanted that for myself.

I wanted the freedom that comes from having my own Endless Income Portfolio.

Since then, I’ve never looked back.

I ‘retired’ long ago.

But I’ve continued to work thanks to a “love of the game” and a desire to share all I’ve learned.

Believe me when I say, there’s nothing better than knowing you have a stream of Endless Income arriving like clockwork.

In other words, becoming..

Every investor does the same thing with their portfolio: They check it.

They get up in the morning, pour a cup of coffee, and log into their brokerage account.

Some carry out this ritual with CNBC on in the background.

Others get their market commentary from one of the countless financial news sites.

But everyone obsesses over the brokerage account balance in front of them.

Spending hours staring at a screen…

And they should be.

Because that money not only represents a lifetime of hard work and savings.

It represents the future.

Were the market to crash some tough decisions would have to be made.

And so every morning, they stare at the screen.

Some for hours at a time. Others several times per day.

When the market falls, they imagine poverty.

When the market rises, they feel euphoric.

This roller coaster rat-race is a reality for millions of retirees and soon-to-be-retirees.

You might stare at the financial news yourself.

And when the market falls you imagine poverty.

When it rises you want to celebrate with a round of golf.

But what if there were another way?

A way for you to turn off the television…

Ignore the market’s talking heads…

And enjoy a stream of endless income?

You’d be able to do what you should be doing in retirement…

It might sound like a fantasy.

But it’s a reality for myself and thousands of others.

Instead of looking to the Dow for how you should feel about your finances, you no longer need to check in every morning.

When you log into your brokerage account, you give the balance a passing glance.

No more pangs of anxiety as you watch one of your holdings go down in value.

Instead, you focus on something far better.

Your income.

Long ago, I learned the value of ignoring the market.

Instead of focusing on this…

We focus on this…

Think about it this way… during your working years you focused on how much money you had coming in every month.

Why should retirement be any different?

Instead of hunting for home-run stocks and capital gains you should always be on the hunt for dividend income.

By owning a diversified list of dividend stocks, you’re free to enjoy your retirement.

So, turn off the TV.

Forget the talking heads in the financial media.

And prepare to become A Dividend Hunter.

Never forget, investing for capital gains is the biggest lie in the financial world today.

It’s how you wind up with Retirement B… returning to work because your savings are gone and you can’t make ends meet.

This is your chance to choose the kind of retirement you desire.

To enjoy all the fruits that Retirement A has to offer.

And the first step is ignoring what the market does.

Success means one thing and one thing only: the dividend income you receive.

As long as that’s growing you’re on track to the right kind of retirement.

I’ve already taken countless investors on the path to Retirement A…

“My portfolio is up $75K since Jan 2016 after instituting your investment philosophy.” -Thomas B.

“Please note that I enjoy your service tremendously, and have and continue to recommend your advisory letter to many of my friends. God bless you and keep up the excellent work.” Louis P.

“I have now been retired for a full year and I just wanted to let you know that I have had great success investing my retirement nest egg using your Dividend Hunter newsletter. My wife and I are living off of the dividend payments and have seen a total portfolio return of 23% over the past year.” -Tom and Gayle H.

For them, investing is fun…and profitable.

And the best part is…

They don’t time the market so they’re free to enjoy life.

They don’t concern ourselves with share price movements. They KNOW know how much money we have coming in every month.

That’s my style of investing.

And it works.

And the best part of all this is you can start investing just like me TODAY.

You can have the full benefit of all my Endless Income investing knowledge right now and at NO COST TO YOU.

I’ll tell you how in a few moments.

But first, I’m going to detail exactly what’s in the Endless Income Blueprint and why it’s so valuable.

To do anything well, you first need to understand it.

And if you want to claim Retirement A you’ll need the Becoming a Dividend Hunter dossier.

It serves as a primer for what it means to be a Dividend Hunter.

After all, change doesn’t happen overnight.

I’ve already shown why you need to become a high-yield investor to enjoy a real retirement.

This dossier is the “how.”

I’ve seen it time and time again. Someone takes charge of their retirement only to stumble right out of the gate.

It doesn’t have to be that way.

What they forget is that you have to walk before you can run.

Which is why I created Component #1.

Inside you’ll discover…

- An in-depth overview of The Dividend Hunter Philosophy so you’ll know how to succeed.

- A review of who can benefit the most from my approach to income investing.

- Why The Dividend Hunter is unlike any other investment advisory publication and what it means for your wealth.

- What you can expect once you’ve made the decision to invest for dividends instead of playing the “Capital Gain Game.”

- The reasons why investing for income is the best way to set yourself up for a lifetime of wealth and security.

And best of all…

- A step-by-step plan for building your own Endless Income Portfolio.

We’re with you every step of the way.

With this report as a primer, you’ll see why going hunting for high-paying dividends is the best path to Retirement A.

Even better, you’ll know how to create your own high-paying portfolio.

![]() Once you’ve read Component #1, this is where you go next…

Once you’ve read Component #1, this is where you go next…

I call it the “Building an Income Portfolio That Lasts a Lifetime”.

It contains all the practical how-to’s of actually setting up a portfolio to receive all the endless income I’ve described here today.

Every piece of this kit is a response to a REAL need that readers have expressed.

Retirement A means having income coming in every single month – and this guide shows you how.

As a bonus, it will show you how to…

- Use the Dividend Hunter’s Payout Calendar to build a monthly income stream.

- Dividend reinvestment strategies.

- Buy and sell rules for long-term success.

- How to put the Dividend Hunter to work for you.

For anyone starting out as a Dividend Hunter, this is a must-have.

One subscriber, Stan P., said it best…

“Thank you for the valuable service you provide… I’ve become convinced that the best investment approach for me is dividend income.”

It details the “nuts and bolts” of an Endless Income Portfolio.

While the next component helps you protect it…

Something big is coming.

As I’ve already discussed, the market moves in waves.

And every so often, capital gains-focused investors can go years without seeing returns.

It’s why one of the biggest fears investors have is a bear market… a market swoon that wipes out their savings.

And if history is any guide, we could be coming up on one of these periods once again.

Which is precisely why this next blueprint component is so valuable.

I call it…

“Sustaining Your Income During the Next Bear Market.”

What you do today very well could determine your financial fate for the rest of your life.

Just imagine, retiring at the start of the most recent “lost decade” – right at the peak of the dotcom bubble in 2000.

Each year you do just as your financial planner advised – selling 4% of your principal to pay living expenses.

And every year, you see your portfolio value shrink.

Down… And down… And down.

This is why I compiled this report.

As we enter our retirement years what we do with our savings becomes all the more critical.

Don’t be one of those investors chases capital gains hoping the stocks you own go up…

That’s how you wind up in Retirement B…

Continuing to work just to make ends meet.

Inside this component you’ll find everything you need to tailor the Dividend Hunter philosophy to achieve the retirement of your dreams – no matter what the market does.

Every day I get an email from someone worried about what the future holds.

How will they retire if the market falls?

These individuals aren’t crazy.

They’re expressing fear about a very real possibility.

They don’t want to leave their retirement to chance …and neither should you.

“I am very glad I subscribed to The Dividend Hunter”

-Johann R.

Dividend Hunters leave nothing to chance.

True “Hunters” focus on how much cash they’re receiving from their investments.

“You have completely changed the way I think about my investments, and I am much more focused on watching my average monthly income go up than I am what the share prices are…” -Jerry M.

Once you become a Dividend Hunter you’ll find there’s nothing holding you back.

In fact, you’ll discover new ways of making money most investors have no idea exist.

Strategies like…

This is my secret weapon.

Lots of “gurus” have secret weapons.

But believe me when I say, this one is in full alignment with the Dividend Hunter philosophy.

I call it…

The “Income Investor’s Secret Weapon”.

You see, Wall Street has lots of ways to make money off Main Street.

My secret weapon takes the fight to Wall Street…

And puts the power in your hands to make outsized profits.

Imagine… turning a dividend stock that yields 5%…6%… even 8% and then doubling that income?

Whenever I mention this secret weapon, and it’s potential to make anyone 10%, 12%, as much as 16% in a single year, peoples’ ears perk up.

That’s because this ‘Secret Weapon’ is the best way to live life to the fullest

And make sure Retirement A…

…is a reality for you and your loved ones this strategy is indispensable.

This strategy is how you go from guaranteeing endless income to becoming wealthy.

“I just want to say what a great system you have introduced me to…”

-Mark C.

“…I made 66% in 45 days’’ -Peg B.

With The Income Investor’s Secret Weapon you’ll be able to turn Wall Street on it’s head.

And start making real income in retirement.

One should always know where they stand.

That’s particularly true when it comes to investing.

Every day I get an email from a subscriber asking me what they should do given their situation.

More often than not, they fall into one of three categories of investor.

What you do at each stage is crucial to your long term success.

Which is why I created…

“Your 3 Phases of Being An Investor and How to Profit” report.

The end goal of this report is to show you what to do at each stage.

That way you’re on the path to enjoying the retirement of your dreams.

All these reports are worth more than $900.

But you get them FREE today.

In fact, I’m about to tell you how I’m going to sweeten the pot.

We’ve talked a lot about having a ‘stress-free’ retirement today.

For most Americans, that means having the confidence you’ll never run out of money.

And part of being stress-free is having someone in your corner helping you at all times.

An expert who can guide you through this transition.

That’s why I’m inviting you to enjoy these three FREE bonuses and much more inside my most popular flagship investment newsletter, The Dividend Hunter.

The Dividend Hunter is my private members-only community where I reveal how to both profit from top-paying dividend companies and see consistent “paychecks” monthly.

You gain access to my personal Dividend Hunter Portfolio.

It’s comprised of stocks I’ve purchased for my own account —

It’s comprised of stocks I’ve purchased for my own account —

And today, I have a very special offer for you.

A “Thank You” for listening to this presentation.

I’m sure by now you’ll agree that investing for income is the only way to guarantee the kind of retirement we all desire.

Which is exactly why I put together my Endless Income Blueprint.

You have the desire to take your financial future into your own hands to have everything necessary to start earning endless investment income.

To do that, you’ll need each component of the Blueprint:

- Blueprint Component #1 – Becoming a Dividend Hunter. Describes the philosophy behind my style of investing and the Dividend Hunter Worksheet that allows you to fully understand your finances. Value: $49.

- Blueprint Component #2 – Building an Income Portfolio that Lasts a Lifetime that dives into the nuts of bolts of building a wealth-generating portfolio that lasts. Value: $99.

- Blueprint Component #3 – Sustaining Your Income During the Next Bear Market contains everything you need to thrive no matter what the future holds. Value: $199.

- Blueprint Component #4 – The Income Investors Secret Weapon is perhaps my most coveted profit-generating secret. Value: $499

- Blueprint Component #5 – The 3 Investor Phases and How to Profit in Them teaches you what to do and when throughout your investing life. Value: $99.

The value of this Dividend Hunter Endless Income Blueprint Kit exceeds $900!

How can you put a price on knowledge and taking control of your financial fate?

And it can be yours FREE with this special offer.

As we’ve learned, anyone can become a Dividend Hunter with the right tools.

But it takes time, discipline, and dedication to truly maximize your gains.

That’s why I started my investment service.

To allow anyone to benefit from the Dividend Hunter philosophy in just a few minutes a day.

The Dividend Hunter’s Endless Income Blueprint is yours

to keep with your Risk-Free Subscription.

Once inside you’ll find everything you need to start earnings thousands of dollars per month – a real income that lasts a lifetime.

Get started right now by clicking the button below. You’ll be taken to a secure page to put in your information.

You’ll join thousands of others already benefiting:

Steve L. wrote me saying:

“I have invested just under $100k and my return percentage is higher than my financial agent can manage. Go figure.”

-Steve L.

And this message from Vic B. in Colorado…

I just wanted to take a moment to thank you for your wonderful newsletter and dividend tips. I have subscribed to a lot of stock newsletters in the past and found them to be very hard to understand.

I have tried several newsletters and yours is the only one I have stayed with.

-Vic B.

I am glad to have found The Dividend Hunter and all your weekly updates. The dividend calendar is excellent and I have been using it regularly.

I eagerly await all your updates and thank you for improving my income stream with all your great ideas.

– Jack G.

The Dividend Hunter will be your go-to resource for building Endless Income.

Thousands have already joined.

If you’re serious about creating a long-lasting income, The Dividend Hunter is worth every penny.

The going rate for The Dividend Hunter is $99 a year.

And I know it’s worth far more.

Believe me this is not some “money grab” situation like a lot of other financial publications engage in.

It’s my attempt to open a whole new world of investing success to you.

That’s because I know that when you begin experiencing the kind of success I’ve described here today, you’ll be back for advanced investment training.

Ways of making money that few know of and allow practically anyone to kick Retirement A into overdrive.

Plus, the wealth of knowledge in the Endless Income Blueprint is worth $945.

But all of it can be yours for just $49.

You read that right.

Today, you can get a one-year membership to The Dividend Hunter for a mere $49 investment.

More than 90% off!

$49 in the grand scheme of things isn’t much. You’ll pay more for a nice dinner out — and that’s without the wine.

And that’s to say nothing of the thousands you’ll start earnings per month like clockwork!

I’ve been told $49 is far too low for all the monthly issues, the updates, and the sheer amount of income you could make.

Here’s what some of my current members had to say:

I cannot remember just how I became acquainted with your Dividend Hunter newsletter, but I am truly thankful. The dividend payouts are like clockwork. Set and forget… have already made back my subscription fees plus. Consider me hooked!

— Alan F

“Thanks to your advice, we are now getting money that we were missing out on before. Our first month’s dividend checks will surpass $1,250!

-Pedro T

What a privilege to have access to your sage advice-I’m shaking my head in disbelief at how my dividend portfolio is performing. Thanks again.

— John O., New York

To join, all you have to do is click the button below.

For the amount of value you’re getting, I’d be tempted to offer zero refunds. I can’t afford to waste time with investors who aren’t serious.

However, I want to make it a no-brainer decision for you, so I’m offering you a full year money back guarantee.

At any point, if you don’t find The Dividend Hunter to be worth every penny…shoot me an email and you’ll get a full refund.

In fact, you can even keep the Endless Income Blueprint Components as a free gift.

Retirement A may be harder to achieve these days.

But that doesn’t mean it can’t be yours…

That you can’t live the life of your dreams after a lifetime of hard work.

The first thing you need to do is ignore what the Wall Street advisors have to say.

They want you to swing for the fences and invest for stock market capital gains.

Next you need to turn off the TV.

And focus on what’s important – generating real income.

Just like you always have.

Becoming a Dividend Hunter is the easiest way to make it all happen.

You’ll have an Endless Income coach right by your side every step of the way.

I created my service for you and anyone else that wants to guarantee the retirement they deserve.

All for just $49.

Leaving your financial retirement to chance is the sure path to Retirement B…

I’ve seen it time and time again.

Every day you delay is one more day further from Retirement A.

You could be generating tens of thousands dollars in endless income right now.

I urge you to…